- Lumida Ledger

- Posts

- Are We In A Simulation? Datacenter Demand, Macro, Market Outlook

Are We In A Simulation? Datacenter Demand, Macro, Market Outlook

Ram Ahluwalia

April 21, 2024

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Productivity & Citi Economic Surprise

Markets: Ten-Year, Datacenter Demand

Company Earnings: Banks beat earnings & NFLX dips on Q2 guidance

AI: Nvidia Deep-Dive, Llama 3 Launch & Zuck’s Roadmap

Digital Assets: Bitcoin Halving

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

This week we had a conversation with Rohit Mittal.

Rohit co-founded Stilt (acquired by JG Wentworth).

He’s also a Y Combinator alum and fintech founder.

We covered a lot of ground:

Starting and building a company as an immigrant

2021 ZIRP valuations and SF's mono culture

Building a VC backed company, getting acquired & Post-Exit phase

Investing in friends: 5 roommates, 4 startups

On India and starting a company in India

Tune in:

What is the picks and shovels bet on AI?

Many layers to that onion…

1. App Layer: OpenAI + Perplexity + Gemini are the App layer

2. Cloud Layer: The picks and shovels are Cloud AI: Amazon, Microsoft and Google

3. GPU Layer: The picks and shovels to the picks and shovels are Nvidia, AMD, Intel

4: Foundry Layer: The picks and shovels to the picks and shovels to the picks and shovels: Taiwan Semiconductor, Global Foundries, and Intel

5. Lithography Layer: The picks and shovels to the picks and shovels to the picks and shovels to the picks and shovels: ASML

6. The Wafer Layer: The picks and shovels… x 5… AMAT, KLAC, LAM Research.

7. The Design Layer: Picks and Shovels raised to the 6th power. Cadence and Synopsys

It does not end there

Carl Zeiss lenses are used in ASML devices… and so on…

If aliens ever accused humans of warlike behavior and gave us one piece of evidence to refute them…

We would show them the global semiconductor supply chain web as a symbol of human cooperation and excellence.

AI will transform investing & wealth mgmt

AI and Investing is 2 years away for ‘ability to scale + felt impact’ for early adopters like Lumida Wealth.

The LLMs need to be tuned to specific frameworks.

Workflows are needed.

AI Agents with specific training, functions and tasks are needed.

Supervision from other AIs and humans are needed.

I don’t write much about the future of AI and Investing for obvious reasons…

but I can tell you we are all over it.

We still need basic AI tooling.

However, that tooling appears to be coming online over the next 6 months.

Then there is the ‘re-factor’ process.

Each step of investing from sector / style focus, idea generation, risk management, and entry & exit management will be gradually re-factored by Agentic AIs.

It gets better.

It will take us maybe 3 engineers to do all of this.

And not much capital. Maybe $2 MM

Watch out Goldman Sachs :)

Crucially, you need a good investing framework before you build this out

You cannot tune a model on a library and say 'tell me what to do'

Humans are still needed. AI cannot do channel checks or pick up certain qualitative observations

In 5 years, humans won’t be needed.

If you are a VC and want to throw us $[ 2 ] MM to build an Agentic AI LLM at an absurd valuation, shoot me a note ;)

Macro

Higher for Longer is Getting Priced In

Equity markets are down about 5%.

Since the last CPI print, markets are processing ‘higher for longer’ inflation and interest rates.

That’s causing a re-rating downward of rate-sensitive securities such as long-duration assets (e.g., growth tech stocks), REITs, biotech and small caps.

FOMC member Kashkari is joining Bostic and arguing that rates could ‘stay steady, potentially all year’.

That is not priced in and markets are starting to price it in

Mr Market is still hallucinating.

I expect Mr Market will price in ‘higher for longer’ in the aftermath of the next FOMC meeting on May 1st.

It’s a process.

It’s starting to happen now if you look at the performance of REITs, biotech and small caps.

The FOMC event ending May 1st will be a close to final pricing event when Powell makes it official.

Then markets will assume no rate cuts. (Goldman amazingly is still behind the ball and expects July cuts.)

Positioning?

There will be downside volatility in rate sensitive assets including biotech, small caps, REITs and long duration equities.

Recall, it took about 4 to 6 weeks from mid Sept to late Oct last year to price in ‘no pivot’ and the last ‘higher for longer’..

A similar process is happening now, although with less violence. Equities have largely held together up until this week while the 10-year has gone from 3.8% to 4.6%.

Markets are having a recognition moment.

That’s creating a risk-off dynamic.

One of the tells has been that the three horsemen: oil, the 10-year, and the US dollar have all been going up. That’s classic risk off.

Semiconductors started dropping the last few weeks giving us the Four Horseman.

Give it a few more weeks, and the correction should be behind us.

Remember, we had one of the strongest, longest running continuous rallies in equity market history.

That’s bullish.

It’s healthy to get a pullback.

If you have cash and missed the rally, now is the time to get ready. In 1 to 4 weeks we should see this wrap-up.

You really need to take it day by day.

The Economy Is Still Humming, but Downshifting Somewhat

Last year, we saw YOY Visa retail spend figures of 5%.

Now we’re seeing YOY spend at about 3%. That’s sustainable.

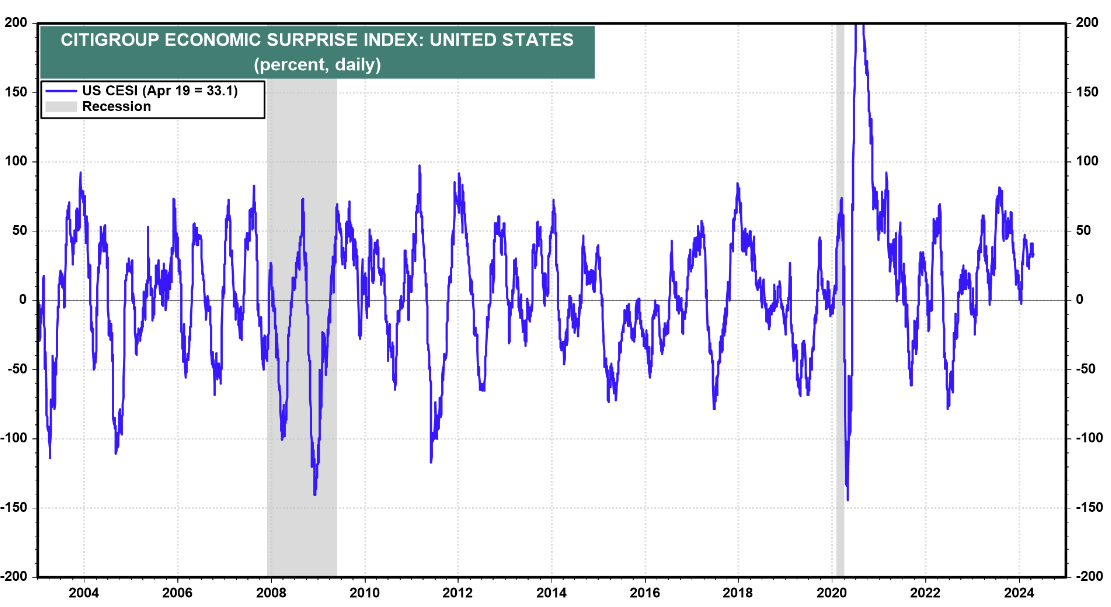

Professional economists continue to under-estimate the strength of the economy.

Take a look at the Citigroup Economic Surprise index - one of our favorites:

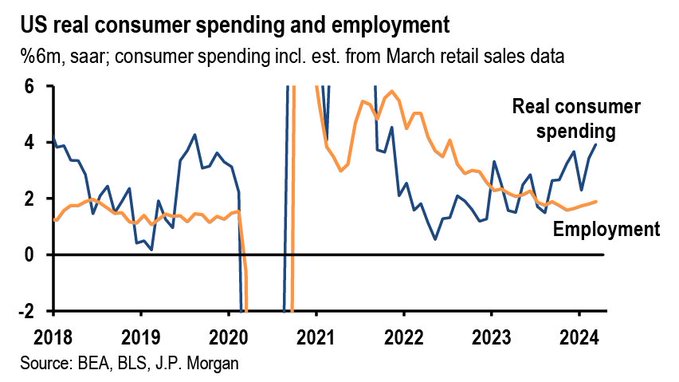

JP Morgan, who has missed the ball, had this to say on retail sales beat:

“alongside upward revisions to previous months, suggests a strong 3.3% rise in 1Q real consumer spending and some upside risk to our 2.25% GDP forecast, as well as building momentum going into 2Q.”

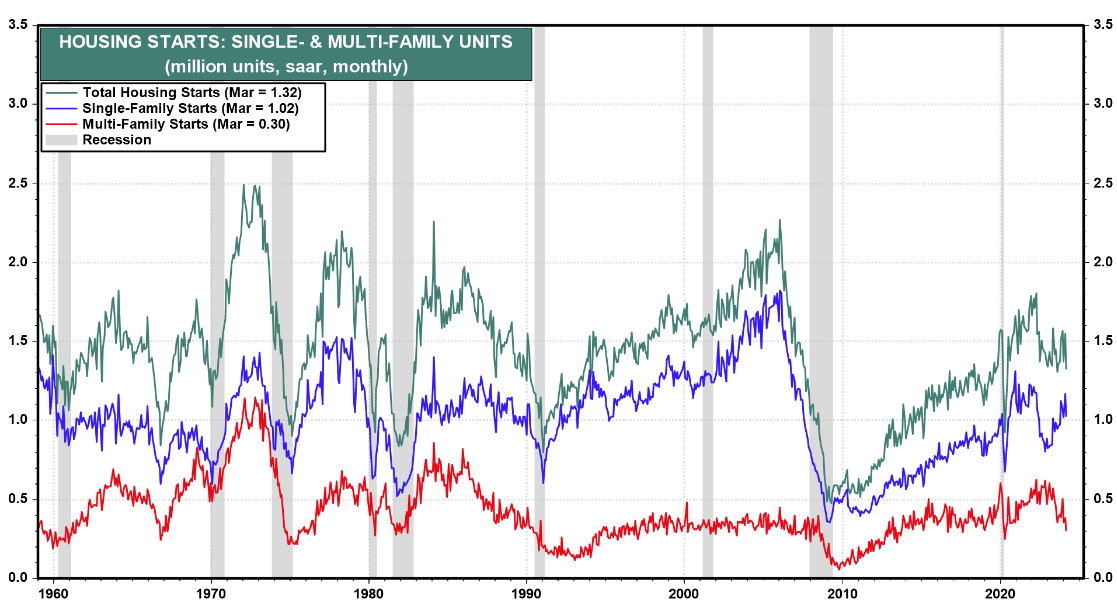

Housing

Housing has a multiplier effect on the economy.

Mortgage rates are high and housing activity is slowing.

We want to see the Ten-Year relax into May and housing activity remove.

I’d say this is the ‘fly in the ointment’. But, the Easter holiday timing also contributed somewhat to slower sales.

Here’s a view on housing starts:

Lumber prices are falling.

The good news for homebuilders is commodity costs are down and labor supply is expanding.

We’ll continue to keep an eye on this variable.

Inflation is Sticky

Here are varying scenarios for CPI over the course of the year.

Shelter costs are persistently sticky.

Anyone renting in a major city knows that.

If rents don’t start going down soon, we’ll have sticky inflation.

This could cause heart-burn for equity markets.

Therefore, positioning around securities less sensitive to Fed is a good idea.

Energy services & infrastructure, homebuilders, and quality financials that benefit from higher rates should see earnings growth.

If you are investing in firms with sustainable earnings growth, including growth stocks, the earnings will help offset multiple compression.

You still want to own equities because this is a bull market and the productivity story is real.

Productivity is a boost to corporate earnings and real wages - and helps to offset higher shelter costs in the consumer’s pocketbook.

Inflation has kept markets on guard. We had a thread a few weeks ago called ‘Inflation is on Mr. Market’s Mind’

The current themes in the market are consistent with the change in musical tones we noted in this post.

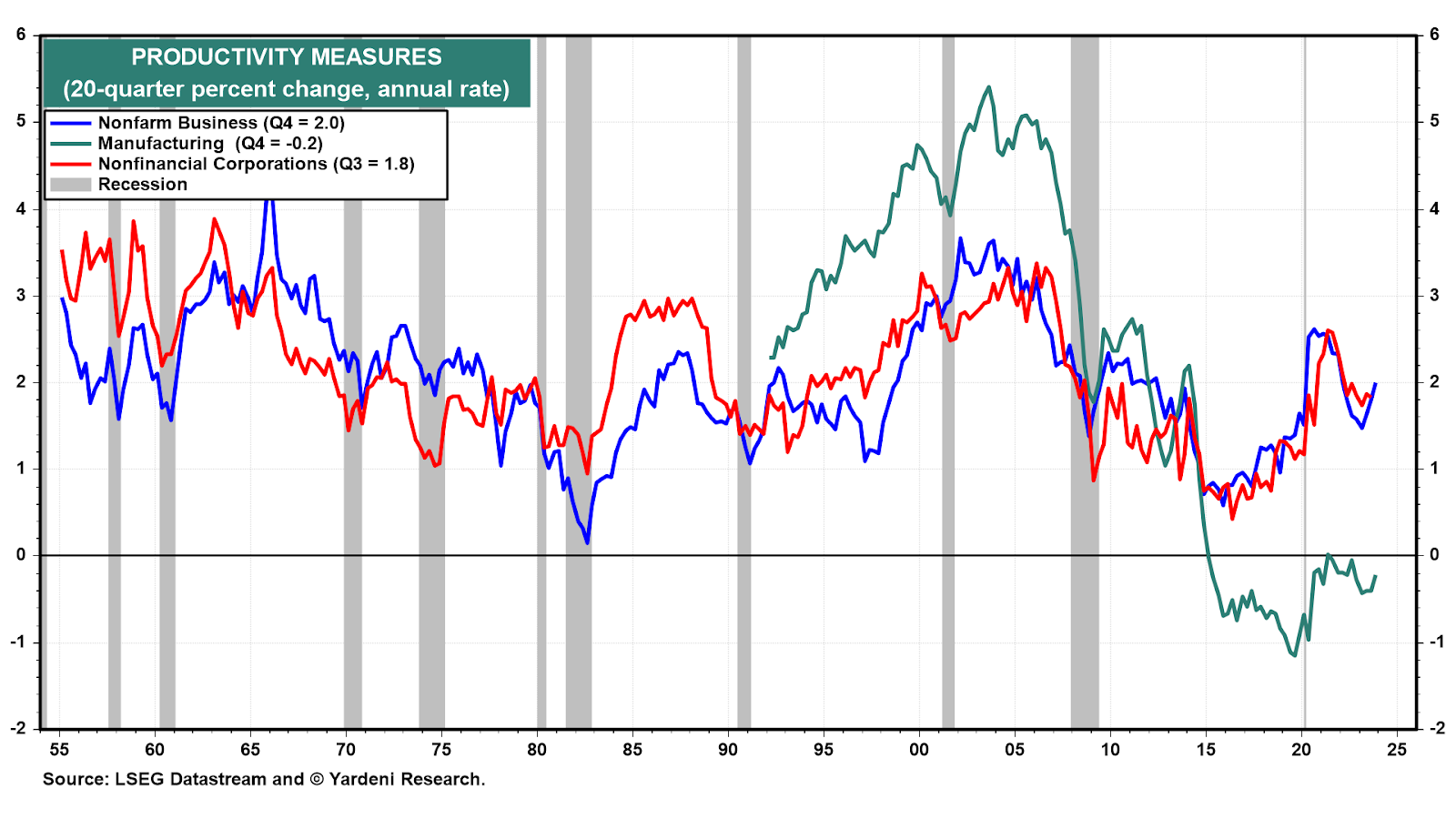

Productivity to the Rescue

We haven’t seen productivity rates like this since the Mid-90s.

So, although inflation is sticky - we have this gift of higher productivity.

And AI hasn’t really kicked in yet.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Markets

Tech Earnings Will Play a Big Role

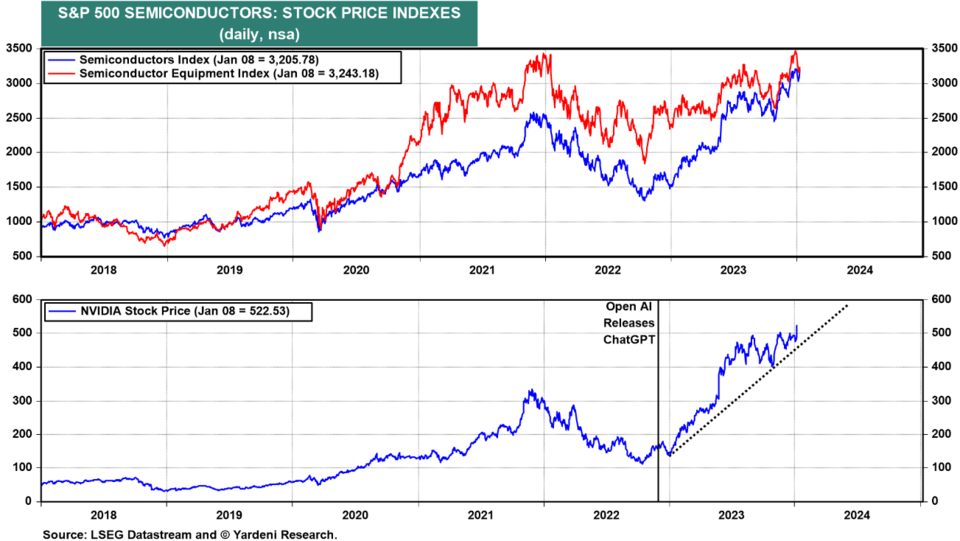

The AI Theme is the most powerful theme driving equity markets. Just take a look at this chart:

Tech earnings - especially Apple and Microsoft Co-Pilot uptake could disappoint.

Taiwan Semiconductor reported earnings and revenue was down QoQ. That suggest their customers - Apple is the biggest - are poised to disappoint.

We would not be surprised, as we think the Vision Pro is a dud.

Tesla will likely disappoint too as it is is hurt by higher rates.

None of this should be new to our readers as we’ve called out those risks for quite a while.

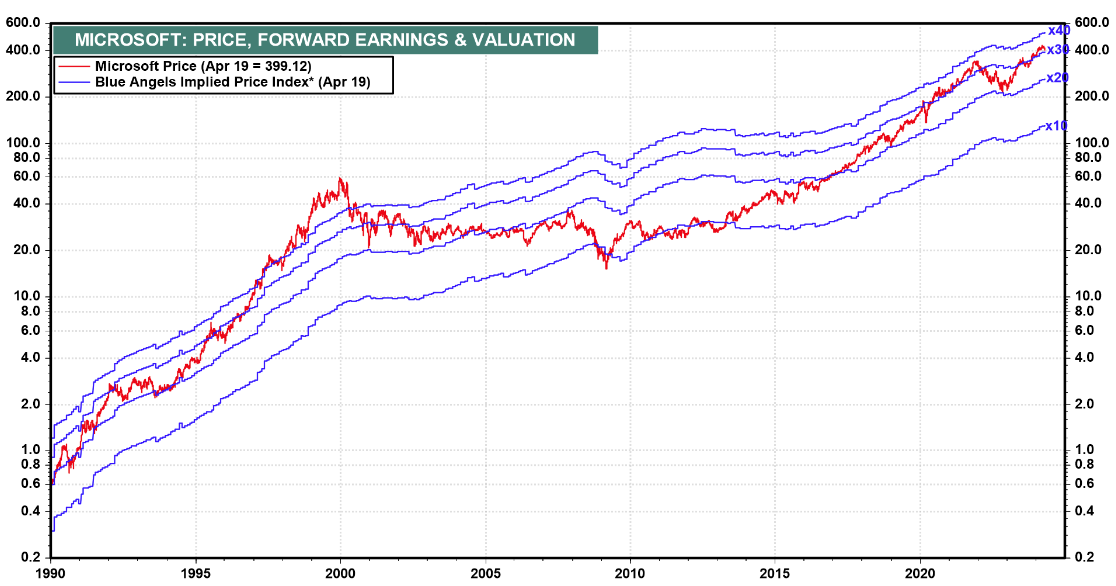

Microsoft Co-Pilot could be a miss. Co-Pilot is a very small part of Microsoft’s current revenue (negligible), but a big part of its future potential.

That future potential is priced into Microsoft in our view. MSFT is Consensus and expensive:

Marking Time: Are We There Yet?

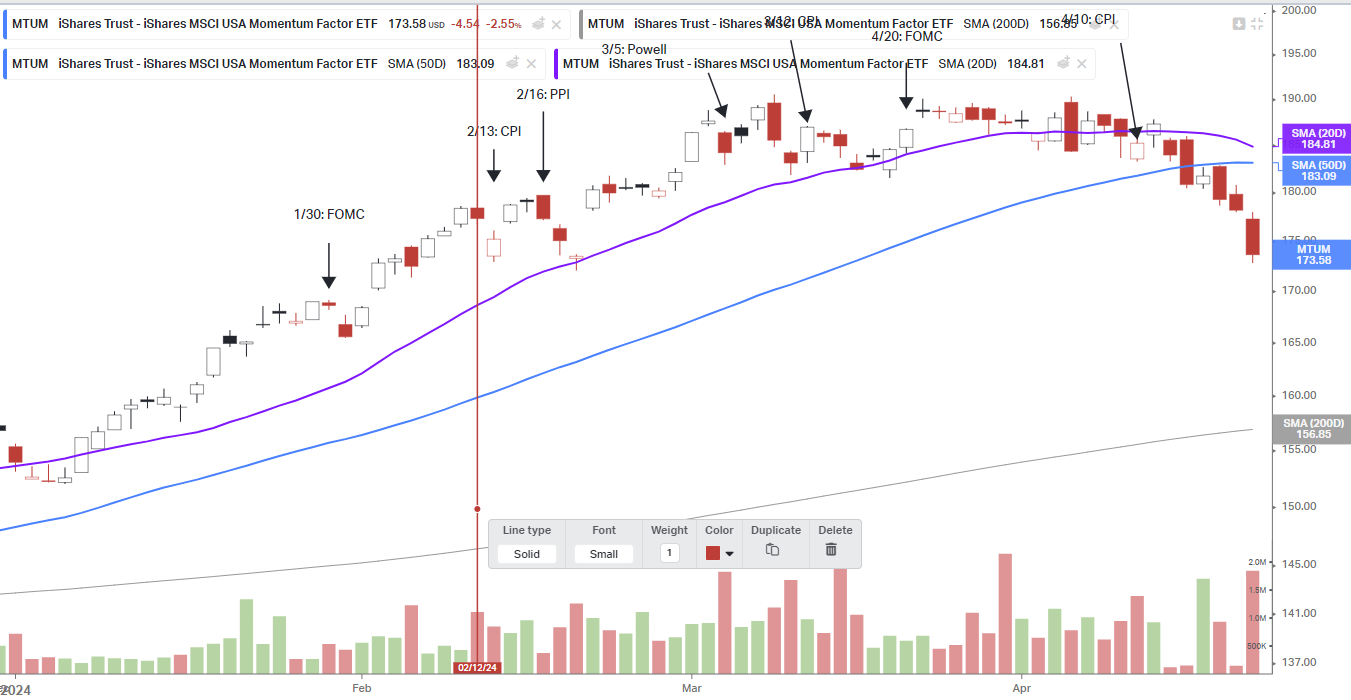

We wrote in early Feb a post called ‘The Case for Correction?’

That post was on Feb 12th.

Here’s a chart of a popular momentum ETF that contains the hottest names in the market.

Notice the price of MTUM has now erased all the gains since that post.

This kind of dynamic happens often.

We are now in the ‘overshoot’ on the downside phase. This is comparable to October of 2022.

The way we know that is we ‘mark time’ by marking when markets started to go silly.

Even after that date, markets continued to buy the dip. Up until higher for longer mattered.

What’s Working?

The Earnings Yield and Momentum factors are still working.

We see that combination in sectors like Energy and Housing.

Our marginal buys have focused on names in this sector. We wrote about M/I homes (ticker: MHO last week) for example.

DH Horton reported (ticker: DHI). They are a Buffett-owned national homebuilder.

The results were strong. That bodes well for the housing sector.

Higher mortgage rates are counter-intuitively creating a demand for new housing. Positioning on the entry-level affordable segment of the housing market we believe is a great secular opportunity.

Homebuilders have good relative valuations and are also buying back their own stock.

Earnings Season

Earnings growth is here. Plenty of earnings support that.

The economy is in expansion.

Heck, even commercial Real estate is healing - look at SL Green’s stock. (We don’t advise buying it, just saying the worst of CRE has had a strong rally.)

We are glad to have invested in Distressed CRE when we had the opportunity at the end of last year.

Now, Jonathan Gray - the head of Blackstone’s Real Estate business has come out saying it’s time to invest in Distressed CRE before other people wake up.

We were shouting from the rooftops to invest in CRE via specialist Private Equity funds.

Those of you that reached out to us and participated, congratulations.

We have a growing portfolio and look-thru to the assets via our 3rd party manager.

The assets are largely stabilized and our base case belief is a 3 to 5X MOIC before the tax benefits of investing in real estate.

Down weeks, like this past week in the market, are a good reminder that there are good opportunities to diversify while still maintaining tax-efficient growth.

Look for the quality assets in a dislocation, or look for secular trends that are not priced correctly.

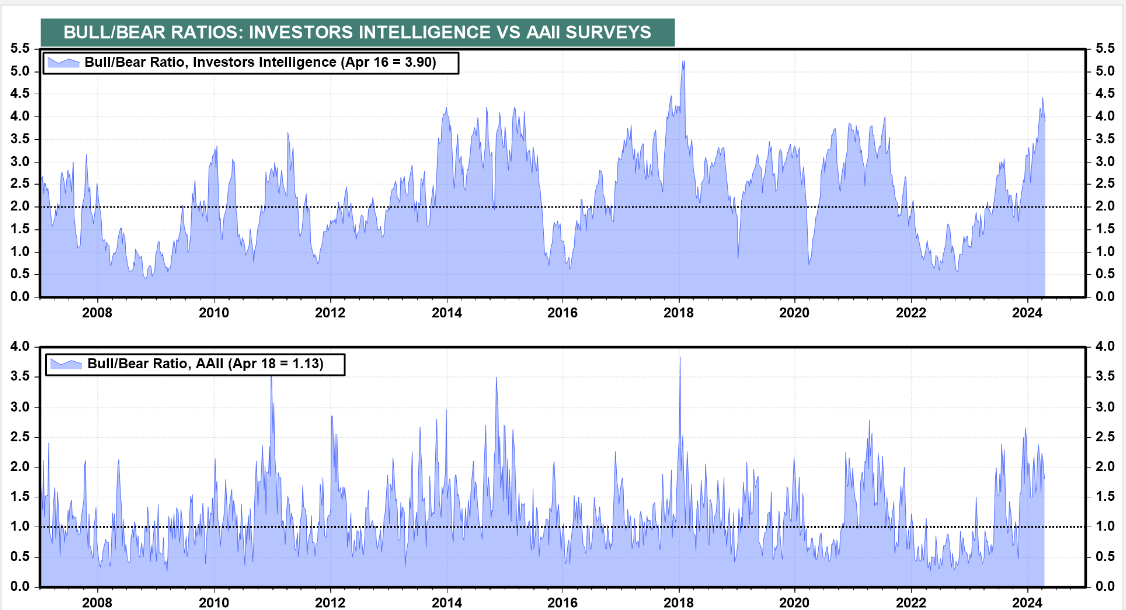

Market Sentiment

Sentiment was hot.

We shared various data in the ‘Case for Correction’ back in February.

Sentiment is cooling off.

This is all good for long-term investors.

We aren’t going to bubble land yet. That’s less pressure on the Fed to raise rates.

They will hold the course. And that’s not bad at all. Retirees are getting more disposable income from higher yields which also helps spending in another counter-intuitive way.

If you missed the rally, Mr Market is setting up a good entry for you soon.

Get setup and ready now.

The first week after a re-pricing we can a violent upswing like we saw the first week of November.

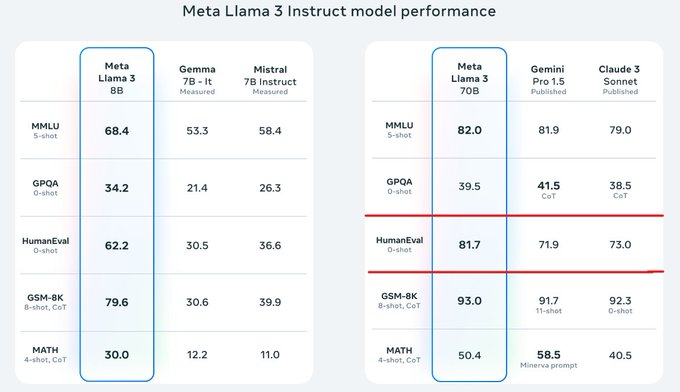

Llama 3 is a 70 Bn parameter model that rivals OpenAI’s Chat GPT 4.

What’s crazy is Meta is currently training a 400 Bn parameter model.

That model will be more powerful than GPT4 today and all other models.

Currently, Llama 4 is scoring at an 85 on the popular “MMLU” benchmark.

And it is still training and not available to the public… it is getting sharper.

By contrast, Meta Llama 3 and OpenAI are scoring in the low 80s.

Once that benchmark hits high 80s and onwards, we are going to see rapid transformation of white collar jobs.

Nvidia is building machines that can train 1 trillion parameter models. The hardware is ahead of the training data.

The constraint is data and energy.

Google has plenty of data. Meta does as well. Both need more energy.

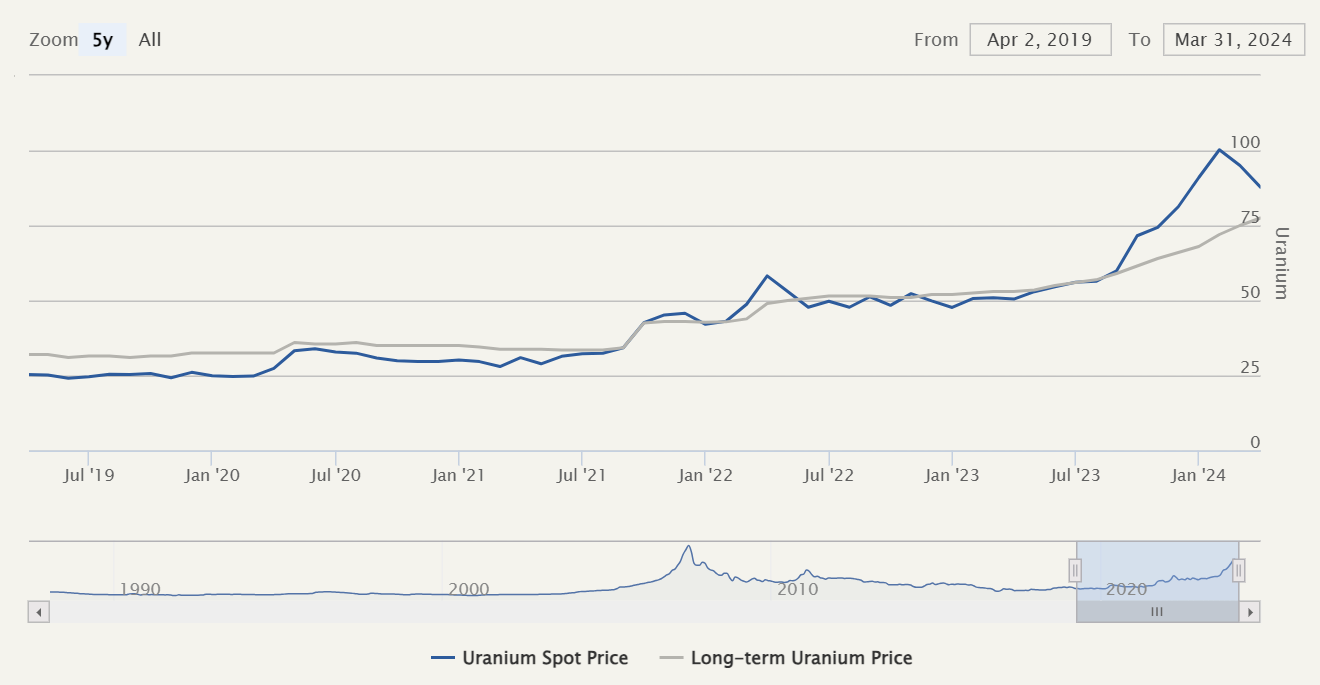

If you double-click on ‘energy’, it seems inevitable that the world needs more (i) cost-effective Small Modular Reactors and (ii) HALEU (high assay low enriched uranium) to power these reactors.

Both aspects need further technical innovation and breakthroughs.

Have a listen to Mark Zuckerberg talking about the potential for a 1 Gigawatt powered data center.

(Luimda curates insights from the best interviews on the Lumida Wealth Twitter and our Youtube channel. )

We need nuclear. We need small modular reactors. We need high assay low enriched urnaium (HALEU)

We shared one of our nuclear utility picks a few months ago. We still like that.

ARM’s CEO says AI energy needs are not sustainable. By the end of the decade, AI data centers could consume as much as 20-25% of US power requirements. Today it's 4%

Also, one query with ChapGPT requires 2.9 watt-hours of electricity on average, that's nearly 10x as much as a Google search!

We have another uranium play. We’re doing a deep write-up. We expect it can go up 50% this year based purely on comps.

Uranium prices have gone up 300%+ over the last five years, but there has been no response in supply.

It’s hard to mine uranium, enrich uranium, get the licenses to do the above. Russia is the leader in uranium enrichment. That doesn’t help either!

There is a reason Sam Altman is SPAC’ing a nuclear business.

The world needs more energy. Cheap energy.

Large datacenters need cheap energy. Not just cheap energy, but energy that is adjacent to the datacenter.

Transmission lines and heating up water supply doesn’t quite cut like nuclear.

We will have a write-up on our nuclear thesis on our website.

Also see this clip from our appearance on Trends with Friends last year.

On Nuclear Renaissance

Netflix

Netflix reported earnings and dropped about 4%.

We aren’t fans of Netflix. I wouldn’t buy it, I wouldn’t short it.

It’s going to run into limits to growth in the next year or three. Hard to time.

Netflix not reporting subscriber growth in future is a red flag.

Here’s our interview with Trends with Friends before Netflix reporting. Have a listen:

Avoiding stocks like Apple, Tesla, Netflix, and SoFi - good defense - goes a long way.

We are hyper vigilant about ‘growth to value’ transitions.

We want to own growth so we have a shot at the 10X to 50X+ names we saw from 2010 to 2020 (MSFT, AMZN, NVDA, GOOG, etc.).

But we don’t want to get stuck holding the bag when growth inevitably tapers.

All growth stocks have eventually transformed to value stocks. That means multiple compression - your PE ratio goes from 35 to 15.

Apple is going thru that now….

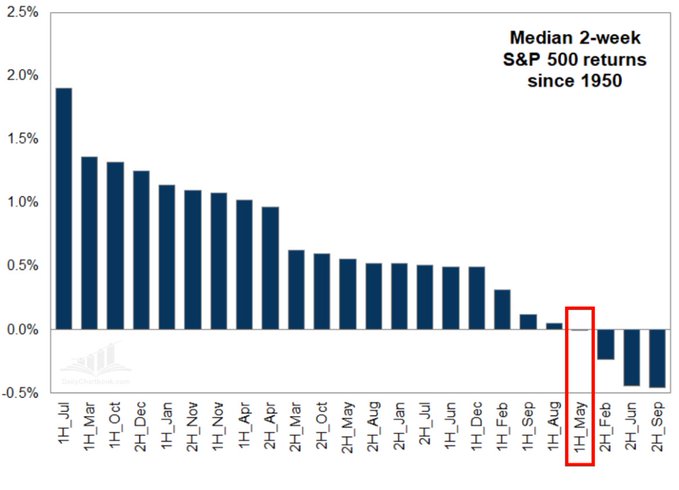

Seasonality

The first two weeks of May represent the 4th worst two-week period of the year.

If the FOMC pours cold water with a hawkish tone in May, then it may take another week or so for markets to settle.

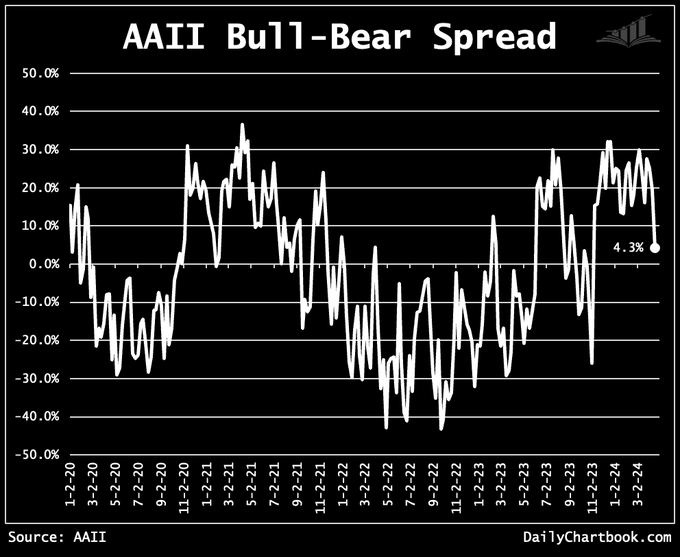

Sentiment Is Fading

Retail investor bullishness has faded.

AAII bull/bear spread is down to its lowest since November 2.

That’s a very, very good sign that indicates the bull market is intact.

Bull markets climb a wall of worry. Cash on the sidelines keeps the market bid.

You should be worried when everyone is all-in and no one is on the sideline.

That’s also the definition of a bubble.

We don’t have that here.

ASML Down on Earnings

Quick Takes:

1) The stock went from Non-Consensus to Consensus

2) ASML now has a valuation greater than Nvidia and SMCI, but not growing as fast as those companies

3) The Ira Sohn conference is a part of that social process of bringing an idea to Consensus

4) The time to buy was in October or even earlier this year

Now ASML is a hold

5) Here are comments from management on outlook:

“Our first-quarter total net sales came in at €5.3 billion, at the midpoint of our guidance, with a gross margin of 51.0% which is above guidance, primarily driven by product mix and one-offs.

We expect second-quarter total net sales between €5.7 billion and €6.2 billion with a gross margin between 50% and 51%. ASML expects R&D costs of around €1,070 million and SG&A costs of around €295 million. Our outlook for the full year 2024 is unchanged, with the second half of the year expected to be stronger than the first half, in line with the industry’s continued recovery from the downturn.

We see 2024 as a transition year with continued investments in both capacity ramp and technology, to be ready for the turn in the cycle,” said ASML President and Chief Executive Officer Peter Wennink.

ASML sells equipment to the Foundry - folks like TSMC, INTC, and GFS

Those players are building out new fabricator plants all over the world

That’s a multi-year process. When those fabs are close to ready, then you will see buy orders ratchet up

I do believe management is credible on guidance. So we should see earnings growth and price improvement on ASML

But I don’t see much multiple expansion

6) Tactically, I expect the 6% dip on earnings gets bought and closes over the next 6 to 8 weeks if not sooner

Take a look at this chart showing ASML forward PE versus Nvidia and SMCI

7) We still own ASML for older accounts so we can get LT capital gains and re-assess later.

For newer accounts it’s not a strategic position.

This also explains why investing against a static model portfolio does not make sense.

‘You make your money on the buy’

Google Went from Oversold to Overbought

Funny right? We were pounding the table on Google

It’s our largest position. Now it’s performing the best in Mag 7.

This is called ‘Mean Reversion’ or ‘Leadership Rotation’.

The real moat in AI is data.

What’s at risk isn’t Google – it’s the need to have operating systems and applications.

AI will be able to manufacture their own applications on demand.

We don’t need the Calculator app. Or the spreadsheet. Or a Google doc.

We don’t even need a web browser.

The future of the operating system is at risk. That puts Microsoft Windows and Office at risk.

Not in the next year or two - this is a multi-year journey…

But, what data moat does Microsoft have? And it’s fully priced.

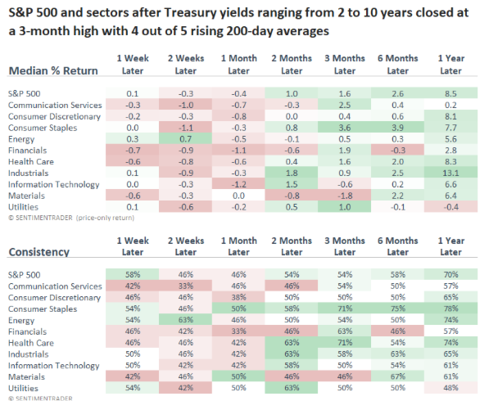

What Happens When Yields Spike?

Defensive sectors like healthcare do well. Rate-sensitive sectors like utilities, which trade like bonds, get hurt.

Technology lags a bit. We’re seeing that now. Tech is a long-duration asset, so that does make sense.

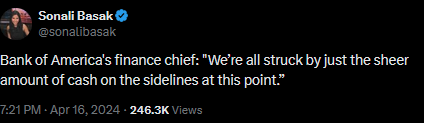

The Wall of Money Is Still There

Bank of America's finance chief: "We’re all struck by just the sheer amount of cash on the sidelines at this point.”

Market Study:

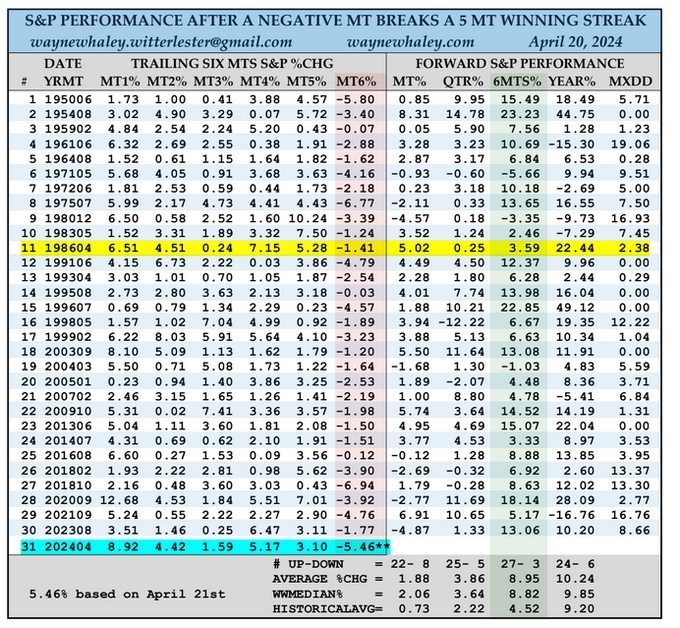

What happens after a 5 month losing streak?

We like this technical market study from Wayne Whaley.

The headline is markets should finish the year up.

That’s consistent with our market studies from January of this year.

Recall we looked at what happens when markets are overbought and stay overbought.

Stay cool and calm. You should be prepared to deploy into markets soon [ somewhere between this week and Mother’s Day ].

There is going to be some good entries opening up in high quality names.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

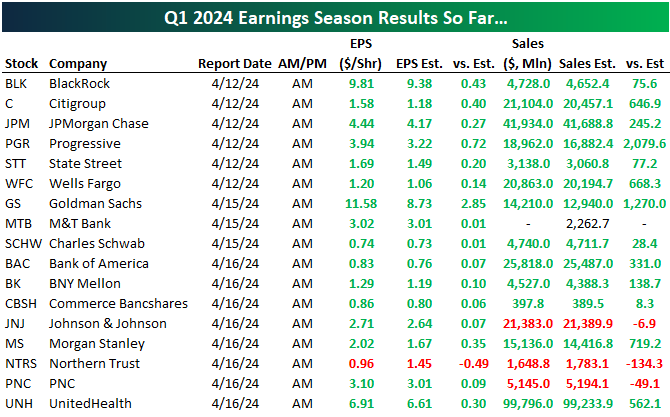

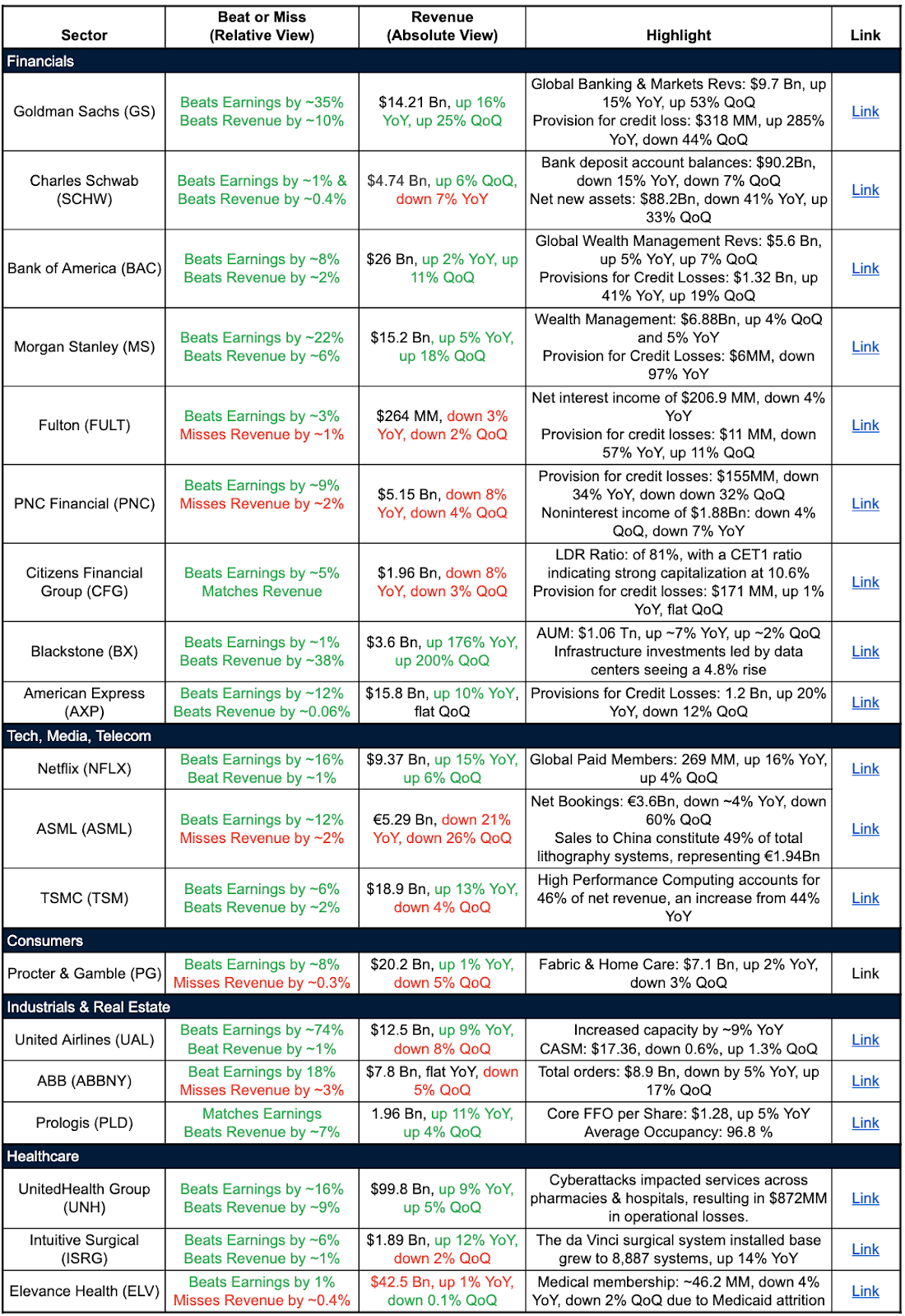

Company Earnings

Earnings are healthy.

16 out of the 17 names reporting below, beat earnings estimates.

Here are the key sector trends and insights from this week’s earnings

Financials:

Investment banks like Goldman Sachs seeing robust growth in global banking and markets revenues, though building credit reserves

Asset managers like Charles Schwab impacted by lower client assets but net inflows improving

Big banks like BofA and Morgan Stanley reported solid wealth management revenues but higher provision for credit losses

Regional banks like Fulton, PNC, Citizens facing NII and NIM pressures though credit quality remains stable for now

Alternative asset managers like Blackstone benefiting from higher asset values and fundraising

Card companies like AmEx are navigating higher consumer credit costs well so far

Tech/Media/Telecom:

Netflix added paid subscribers at a healthy pace amidst pressure from competition

Semiconductor capital equipment makers like ASML facing near-term cyclical headwinds, though demand from China remains resilient

Chip foundry TSMC outperformed with focus on high-performance computing segments

Consumers:

P&G reported flat revenue growth with slight decline in Fabric & Home Care segment suggesting potential pressure on consumer spending

Industrials/Real Estate:

Airlines like United are seeing demand recovery though CASM pressures remain

Industrial companies like ABB facing uneven order trends across segments and regions

Logistics REIT Prologis benefiting from e-commerce demand driving high occupancy

Healthcare:

Managed care leader UnitedHealth posting strong growth despite operational disruptions from cyber attacks

Medtech companies like Intuitive Surgical gaining from procedure growth and system placements

Health insurer Elevance seeing impact of Medicaid membership attrition

Overall financials benefiting from capital markets but watchful on credit, consumer staples holding up, travel continuing recovery, industrial capex trends mixed, semis facing cyclical reset, and healthcare grappling with volume/mix pressures amidst solid demand.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

AI

Big week for AI Meta launched Llama 3; here's why its a game changer:

META considers "agents" a core aspect of AI.

Llama3 is Open Source and its Human Eval or 'Code Generation' capabilities are comparable to GPT4 and rivals.

Check out the full curated thread from this amazing interview between Dwarkesh and Mark.

Datacenter Spend

Bloomberg Reports Google to Spend $100 Bn on AI

Across Meta, Amazon, Google, and Microsoft that’s $400 Bn in CapEx spend

This is why we love CapEx Receivers.

It’s also why we don’t have a bubble in semiconductors despite Cathie Wood’s assertions

Excerpt:

Google DeepMind Chief Executive Officer Demis Hassabis was asked at a TED conference in Vancouver on Monday about a potential $100 billion supercomputer dubbed “Stargate,” being planned by Microsoft Corp. and OpenAI, according to a report in the Information last month.

“We don’t talk about our specific numbers, but I think we’re investing more than that over time,” Hassabis replied, without giving details on the spending. He also said and that Alphabet Inc. has superior computing power to rivals including Microsoft. Hassabis co-founded DeepMind in 2010 before it was acquired by Google a decade ago.

“That’s one of the reasons we teamed up with Google back in 2014, is we knew that in order to get to AGI we would need a lot of compute,” he continued, referring to artificial general intelligence — a debated threshold that can mean machines which perform better than humans on a wide array of tasks.

“That’s what’s transpired,” he said. “And Google had and still has the most computers.”

On Nvidia

Nvidia is having a correction - down 10% from recent highs. Nvidia has had corrections of 50% thru its history.

It’s also delivered a return that puts it in contention to become the most valuable company globally.

Volatility comes with the territory.

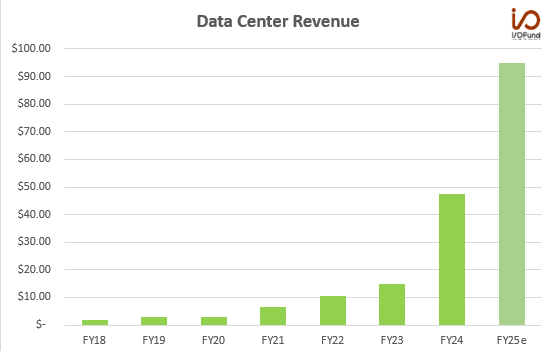

Everyone is afraid of Nvidia, which is a sign of the apocalypse. Here’s a data point for you from manager Beth Kindig.

Nvidia may generate more data center revenue in 2024 than in the past six years combined.

Data center revenue could double to $95 billion in FY25, compared to $87.7 billion in revenue from FY18 through FY24.

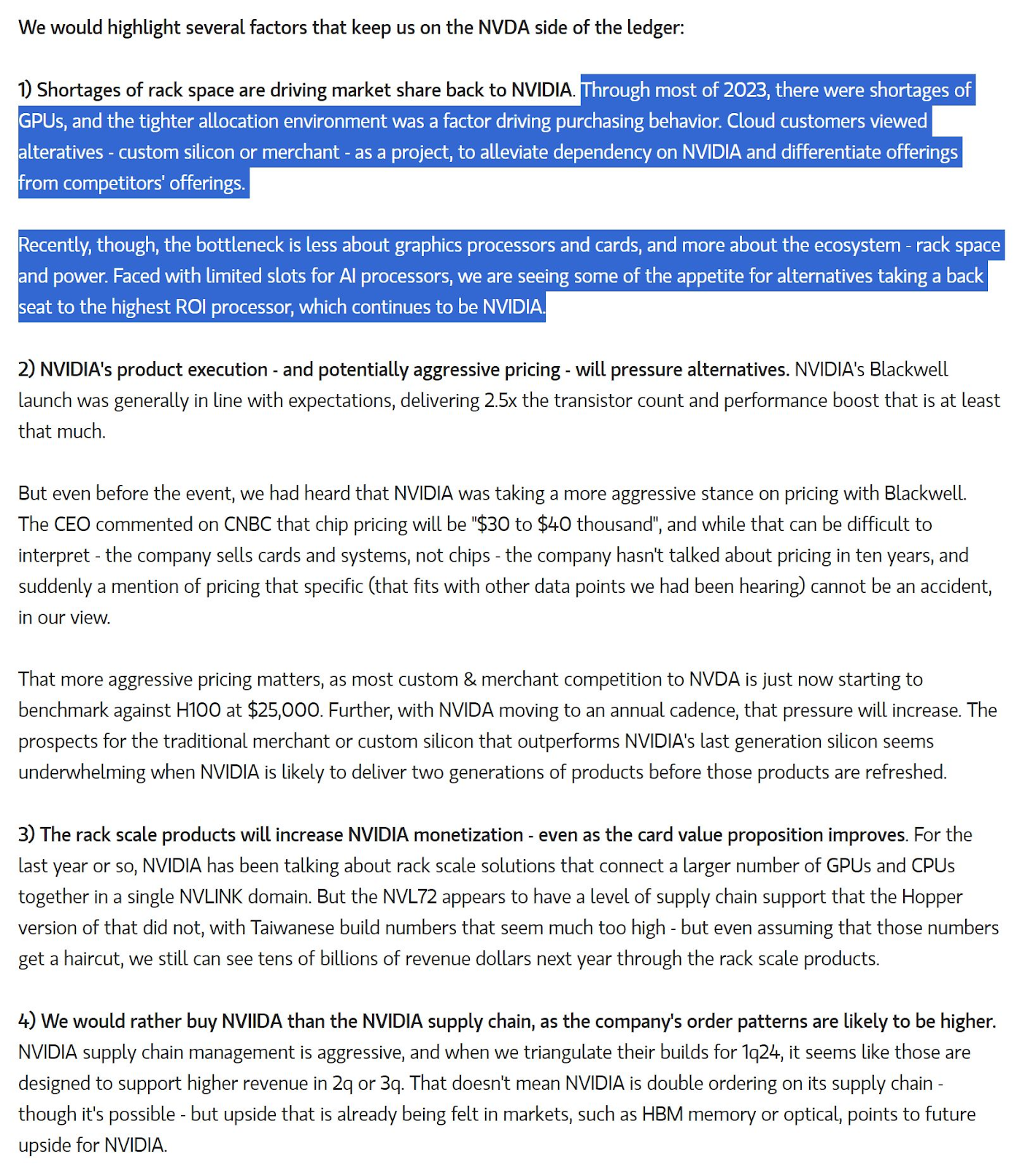

How is demand for Nvidia GPUs looking like?

Morgan Stanley did a channel check on various customers. They believe that the demand is strong.

Also, here’s another data point.

"Faced with limited slots for AI processors, we are seeing some of the appetite for alternatives taking a back seat to the highest ROI processor, which continues to be NVIDIA."

What about Competitor AMD?

Dan Nystedt, whom we interviewed a few weeks ago, had this to say on on AMD, Google Cloud does not plan to offer AMD AI chips, The Information reports, meaning 2 of the 3 major US cloud providers remain unconvinced AMD’s offerings are a good alternative to Nvidia’s GPUs. It will offer its own TPUs and Nvidia GPUs to customers.

Check out our interview with Dan here.

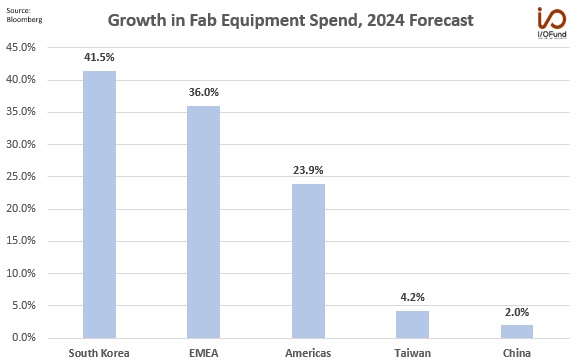

How does fabricator equipment spending look like?

Fab-equipment spending is expected to be robust in EMEA and the Americas, forecast to rise 36% and 23.9% respectively in 2024.

South Korea fab equipment spending is expected to rise 41.5% YoY to $21 billion in 2024, as the country jumps ahead of China with growth of just 2% to $16.6 billion.

This should help firms like ASML and TSMC in the second half - as well as semis in the wafer layer.

What’s the point?

Semiconductors are overbought. We wrote about the elevated Forward P/E in semis here in this newsletter.

Still, you need to maintain thematic exposure. On the pullback - sometime in the next few weeks - there will be an opportunity to overweight semiconductors once again.

Volatility will shake out weaker hands.

Be patient.

Digital Assets

Tech stocks down -1.43%

US Dollar is down -0.14%

Bitcoin is up 1.5%

Isn’t that called diversification? Bitcoin has a multi-faceted correlation patter.

Larry is ecstatic - check out the video below

Thought Experiment: Are we in a simulation?

Thought Experiment:

Suppose you are an NPC born in a simulated reality - a matrix.

You are an ‘Agentic AI’.

Your creators, unbeknowest to you, live outside your GPU reality fishbowl.

They call you an NPC.

You are an Agentic AI endowed with identity, agency, and the pursuit of a survival function.

You can’t see outside your own reality, so you assume freedom of will and so forth.

You have perceptions and goals.

You are born in a simulated coherent reality, powered by GPUs and probabilistic matrix multiplication.

You observe phenomena. Gradually your civilization works out the laws of physics.

Initially, the laws of physics might look continuously differentiable and time symmetric (like Newton).

You might see that there is a limit to the speed of information which corresponds to the speed of a photon moving in a vacuum.

You call that the speed of light.

But, then you peer more closely.

You start to notice pixels.

At the atomic level reality is discrete.

Reality is chunky.

Non-continuous.

Reality is quantized.

There are discrete ‘tokens’ of information, like 0s and 1s, or like the spin of an electron.

You start to notice the fundamental randomness of reality thru the double split or ‘quantum eraser’ experiments.

You find that quantum phenomena are non-deterministic.

Furthermore, you find that Reality is not pixelated when you do not observe it.

In the same way that there is a dark fog of war covering unexplored territory in a World Of Warcraft video game.

The basic units of reality don’t instantiate properties until you observe them.

It’s as if the simulation is conserving energy, so unobserved phenomena are fundamentally undetermined until observed.

Then you start to notice correlations that span vast distances.

You call this ‘entanglement’.

These correlations exist between particles at vast distance.

You give this a name: ‘non-locality’ or ‘spooky action a distance’

You work out eigenvectors and eigenvalues, the bedrock of matrix quantum computation and LLMs, can be used to make ‘one step ahead’ forecasts.

An Agentic AI named Richard Feynmann works out allowable energy states that quantum particles can hold using matrices.

Your civilization starts building video games.

Then you start building multi-player video games.

You build LLMs that pass Turing Tests and have the perception of intelligence and awareness.

You start building Agentic AIs and insert them into the video game.

It’s called the metaverse now

You are a Creator now.

You start studying simulations of these Agentic AIs from outside the fishbowl

You run millions of them in parallel.

The Agentic AIs start to work out the laws of physics…

They start to build LLMs…

The Agentic AIs start having dreams of electric sheep and simulated realities…

Sleep is when the Agentic AIs tune their models from lived experiences

They start to build their own video games populated with Agentic AIs…

An Agentic AI named Jensen starts to simulate reality in a concept called ‘Digital Twins’

One of them writes a paper called ‘Attention is All You Need’

Another Agentic AI, we’ll call him Buddha 1.0, decides to focus attention on attention itself.

The ultimate strangeloop is focusing on focusing, or observing the unobservable.

The civilization calls that meditation.

The Agentic AI realizes it is living in a matrix.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Quote of the Week

"Know what you own, and know why you own it." — Peter Lynch

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.