- Lumida Ledger

- Posts

- Time for a Correction? A “split” equity market

Time for a Correction? A “split” equity market

Ram Ahluwalia & Justin Guilder

February 11, 2024

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Markets: The Quality Momentum Rally, Equity Futures are Max Long, Mr. Market is Getting Sloppy

Macro: China, Economy Beats Expectations

Company Earnings: Key themes and headlines

Digital Assets: Crypto VC Funding

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

This week Ram was in Dubai meeting clients & prospects and learning about the tax regime and local culture.

There’s a lot happening in Dubai.

Tune in to our latest What’s on your mind to find out.

Ram also shared his experience trying out NAD+ - a longevity driver.

Longevity is one of Lumida’s key investment themes - we believe spending on Longevity is a secular trend.

Markets

There’s a lot to get into this week.

Markets are on a record winning streak not seen since the early 1970s.

We wrote this about two weeks ago in our newsletter. We believe this explains much of what we are seeing today.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Recall, we looked at a few studies at the beginning of the year to understand what happens after markets have a multi-month winning streak.

The basic takeaway - expect more upside and buy all dips. Overbought markets stay overbought.

We’ve had a few dips. They were marked by spikes in fear from the Empire Manufacturing index and the FOMC meeting last week.

We have a new insight into what is driving markets.

There is a funny paradox in markets. On the one hand, breadth is decreasing. Meaning if you throw a dart at a random stock, it is declining. On the other hand, indices are at ATH.

What’s happening?

In short, since the beginning of 2024, we are experiencing a quality momentum rally.

Quality refers to Profitable Growth companies. This can include Buffett type businesses, hyperscalers, Caterpillar, FICO…

Investors are bidding up the highest quality businesses across sectors. It’s really quite something - and no one is talking about it.

We love to find quality businesses and for nearly every sector we partition names into ‘Leaders’ and ‘Quality’ vs. the rest.

And the inescapable conclusion is we are in the Best vs. the Rest rally.

Here’s what has rallied since the FOMC meeting:

- AI theme & semis: Nvidia, Meta, On, and many others

- Financial services (APO, Verisk, Visa)

- Healthcare (Novo, LLY)

- Biotech (RCKT and others)

- Insurance (Aon, McK, etc.)

- Nuclear (but not energy)

- Tech / SAAS (Mongo, Nu, Shop)

- Consumer Discretionary

- SAAS (DDOG, PANW, etc)

The themes are broad

All of these stocks also have exposure to the momentum factor. Meaning, they have relative strength.

The mindset of Mr. Market is something like: 'I'm scared of higher rates, so I want to rotate out of cyclicals (energy, small banks, unprofitable tech, etc.). BUT, I have a mandate to own equities. I can't lag my benchmark. So, I'm going to hide in Quality stocks. And, specifically, those quality stocks in uptrends'.

That is the Zeitgeist.

It’s not a Growth vs. Value play either. Berkshire Hathaway is the epitome of Quality. That’s also up. Caterpillar and United Rentals are nicely up as well.

This is a Quality and Momentum rally.

It turns out semiconductors and software companies have a lot of Quality - and they are rallying nicely. We have significant exposures to these themes, so we are benefitting from that.

What’s not working are cyclicals - including Uranium miner Cameco which is taking a breather.

Profitable growth is working.

These are great businesses by and large.

We own many of them (Nvidia, PANW, Apollo, APEI, ASML, Cloudflare, Novo Nordisk, and many more). All of these names we have written about on X or in our newsletter.

Pick a random sector and you’ll see the best winners are Quality.

This is not a junk stock rally by and large.

Thus far, 2024 has been a Smart Money rally, not a retail rally.

What’s not working?

Volatile stocks, junk, and negative momentum.

Volatile stocks like regional banks, energy metals and mining are, on average, down since FOMC.

SoFi, Beyond Meat, cruise lines, mortgage lenders, shaky REITs, Bitcoin miners, etc since the FOMC. These ideas have been punished.

Weak semiconductors and weak software firms have also been punished.

We can’t find a short in those sectors to hedge because they are already beaten up!

Mr. Market is crowding into the very best names in the sector. That’s causing Quality stocks are getting re-rated higher by Mr. Market.

In 2024, Mr. Market has a refined diet and wants only the very best now.

Statistically, your optimal strategy as an investor is to own these factors over a long period of time.

Part of the reason we detected this is we like the Quality, Value, Momentum trifecta. And we do believe owning high quality businesses at fair prices is the best way to compound wealth over the long run.

Now, how far can Momentum run?

Take a look at MTUM. This is an ETF representing momentum stocks.

Let’s zoom in a bit more. That green dot is the wake of the mini-correction post New Years.

The ETF is not quite parabolic and it could keep going.

Will ‘the rest’ catch up?

Notably, we saw a slew of earnings reports with major pops.

Meta: 20% pop (we own it)

Cloudflare (NET): 20% pop (we own it)

SPIR: 20%+ small cap pop (we own it)

SLQT: 20%+ pop (we own it)

You can look up the tickers for META, NET, and SLQT and you will see Ram’s buy calls.

SPIR is a new position as of two weeks ago.

What started to happen Friday is low-quality retail stocks started participating.

Bitcoin miners like CLSK took off.

So, much like the last two weeks of December, we are seeing retail investors get excited and get back in the market.

Mr. Market was highly disciplined YTD. Now we believe we’ll see a rally broaden to low-quality names.

That will keep the indices going higher. Retail investors are often late to the party though, so we’ll want to be on guard the next couple of days and weeks.

We are not really buying many securities at current levels. We’re fully invested. There are a handful of tactics here and there that come up that we’ll take advantage of. It’s not a buyer’s market anymore.

How to hedge in this setup?

Find negative momentum, low quality, expensive stocks.

Stocks like Tesla before they crashed and burned.

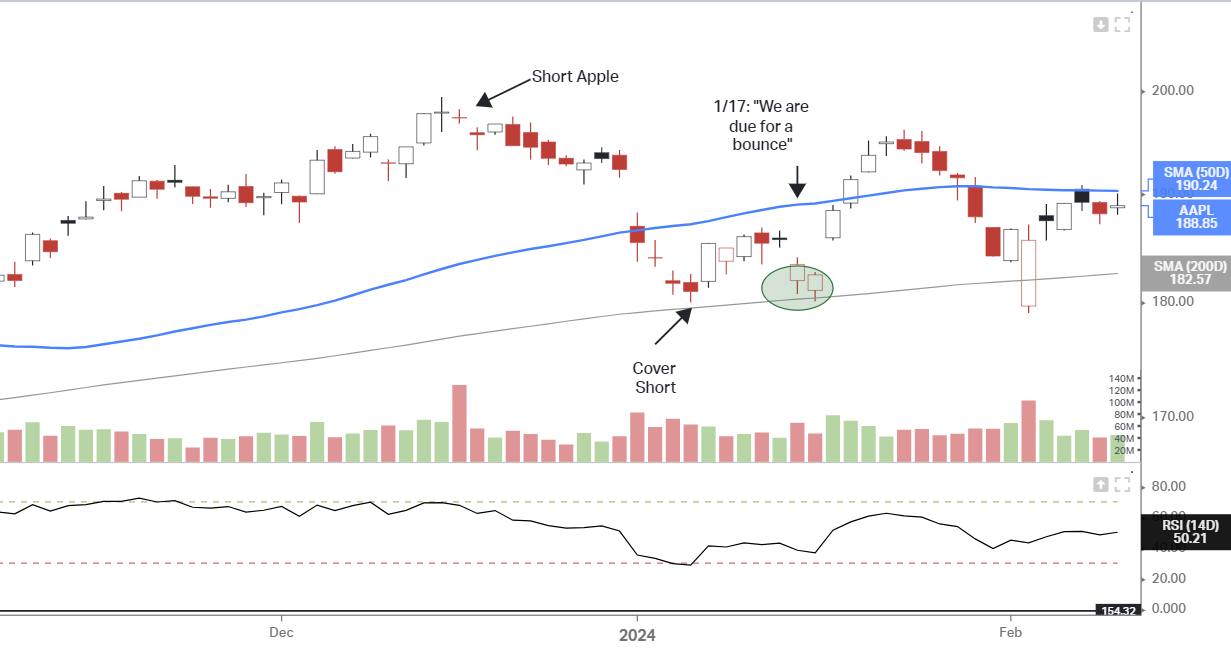

We added shorts on Apple and Oracle to reduce our net exposure. This helps us avoid incurring capital gains from selling wonderful businesses that we want to own for a long-time.

Apple’s stock dropped after earnings last week on guidance that their revenue is shrinking 5% in the next quarterly update.

We view Apple as a growth stock transitioning to a value stock - that means PE compression. So, when Apple gets near its highs we believe it serves as a nice hedge.

You can see our prior commentary on Apple here. How does the entry on that last bar look to you? Should Apple break, which is possible, we would expect those gains are given back.

And if it takes off - that means long positions are taking off at presumably a faster rate.

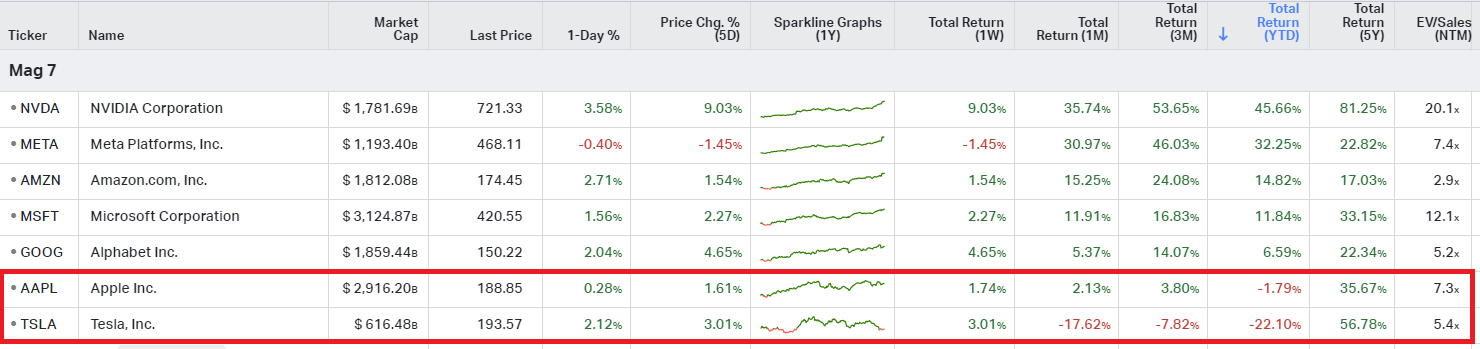

Indeed, Apple has lagged its Mag 7 peers.Take a look…

If we make money on a relative basis we are fine.

Since we started critiquing Apple’s lack of revenue and earnings growth over the summer there have been ~6 analyst downgrades.

It takes time for the public to shake their perceptions. Those events usually occur during earnings… More to come on the wonderful but shrinking business we call Apple.

Notice how these retail stocks are getting slammed.

This is from Thursday…but it’s the story for most of the year.

Low quality stocks haven’t received a bid until this Friday. (Mr. Market wants to make us put more work and nuance into our newsletter!)

Quite a few of these are also retail favorites are they not?

Mr. Market has done a good job sorting out weak semiconductor stocks.

The low quality semis tanked after January and never looked back, even as Nvidia went up 40%.

Take a look at NVTS or DIOD for example.

Mr. Market is cleanly separating leaders from laggards.

It's quite impressive to see - there are not many easy to find 'low hanging fruit' mispricings.

Thus far, this is not a sloppy rally.

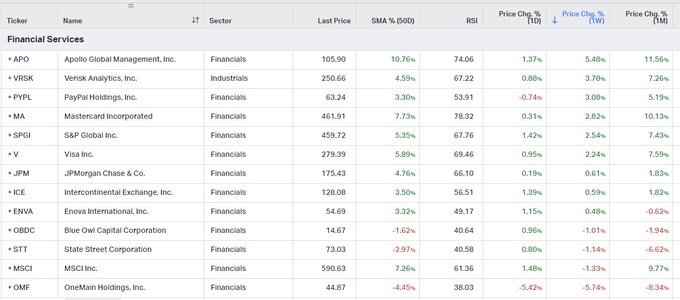

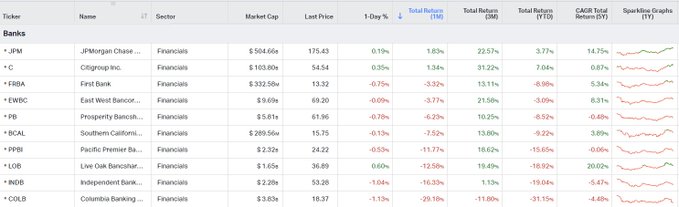

Here is our quality financial services screen.

Notice how 'quality' financial services firms have rallied as low quality regional banks get smashed.

Lenders are also getting hurt - such as One Main Financial.

(PayPal is in the Quality list, it just needs positive momentum to get going. We would buy PYPL on dips.)

How about Small Caps?

Quality Small caps are rallying too!

When people say Small Caps aren’t keeping up, show them this list.

Take a look at this screen. I had to crop out the names because these are our favorite small caps after extensive research.

We are growing paranoid when we publish a list and we see those names lift-off (like our Semiconductor list).

The mark of a true investor or accumulator is we welcome low prices

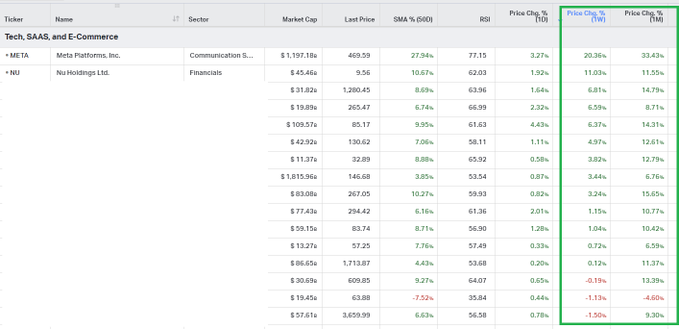

What about Tech?

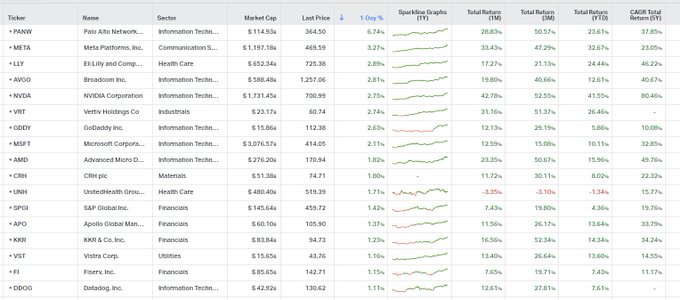

Take a look at our Quality Tech screen

What are the top names? Meta and Nu.

We talked about both of these names on Howard Lindzon’s Trends with Friends podcast two weekends ago. This was before Meta’s monster earnings bounce of 20%+.

Here’s a link for the receipts.

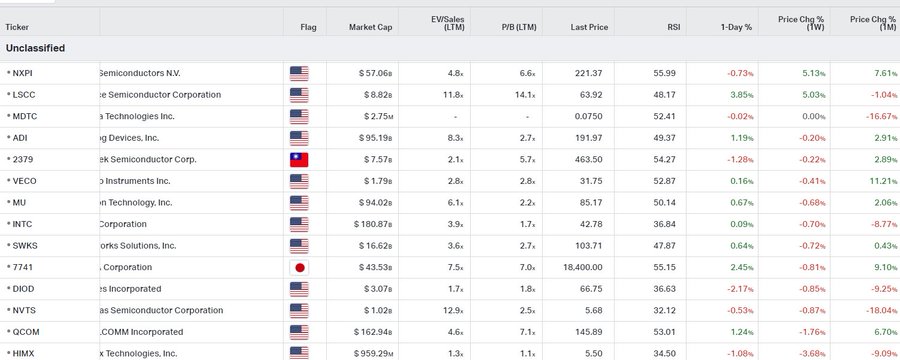

This is a screen for semiconductors that are lower quality.

They are all lagging Quality semiconductors substantially.

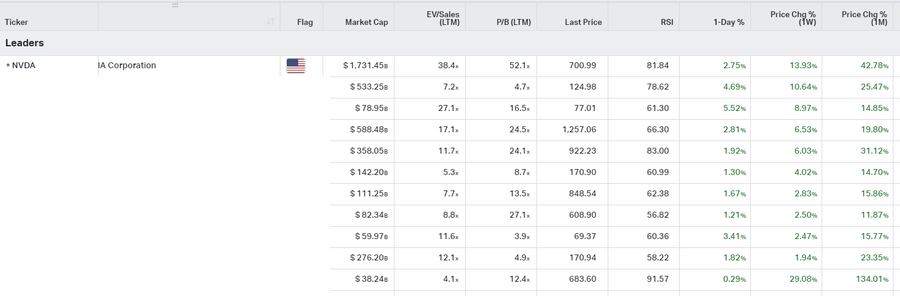

Now compare that to quality semiconductors (also shown below but masked)

Table: Bad semiconductors (QCOM we’re not sure about)

Table: Good semiconductors. Green everywhere. These are the names we are buying.

Note the Too Big to Fail banks are on top.

Quality banks are on top.

This is a Momentum Quality rally.

Next time someone says it's just 7 stocks, show them this list.

These are Quality factor firms.

Of the top 5 names, we like and have discussed: PANW, META, NVDA, AVGO.

Cybersecurity and Semis - a good combination.

PANW was a stocking stuffer stock.

Are we in bubble territory?

No, we are not.

Mr. Market has sobered up and is rational.

Are we OB? Yes. But… there is a rationale to it.

These are great businesses that are rallying.

This is a stock pickers market unquestionably.

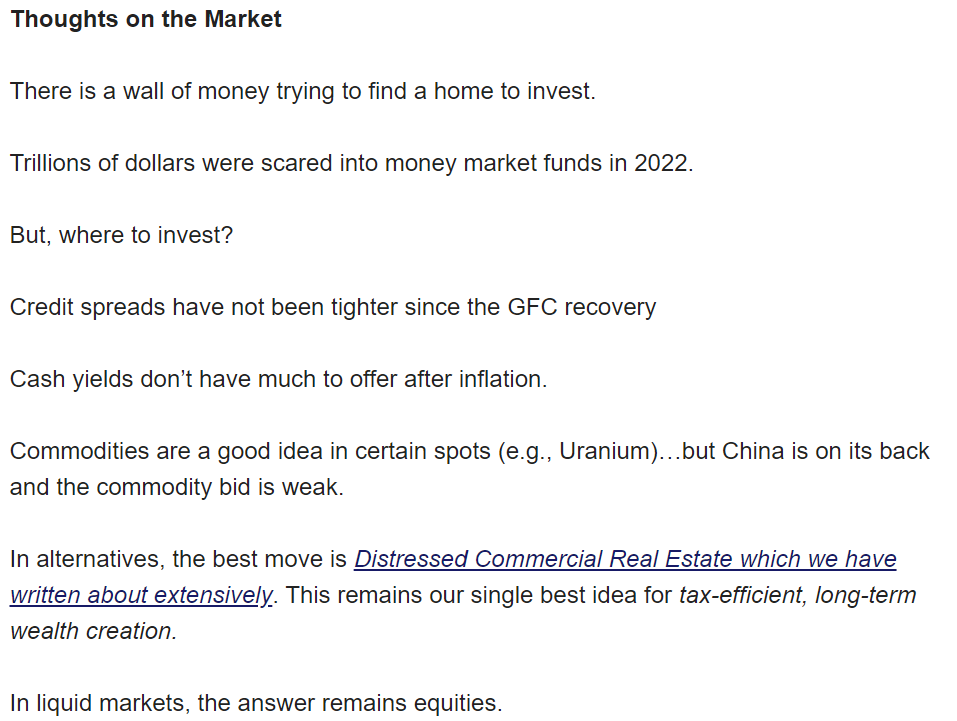

The Case for a Market Correction

We ended last year with a flurry of technical studies noting we are setup for a bull market in 2024.

And we believe that’s the case.

But, we are now seeing abundant evidence that we are due for a correction.

Let’s go thru our list.

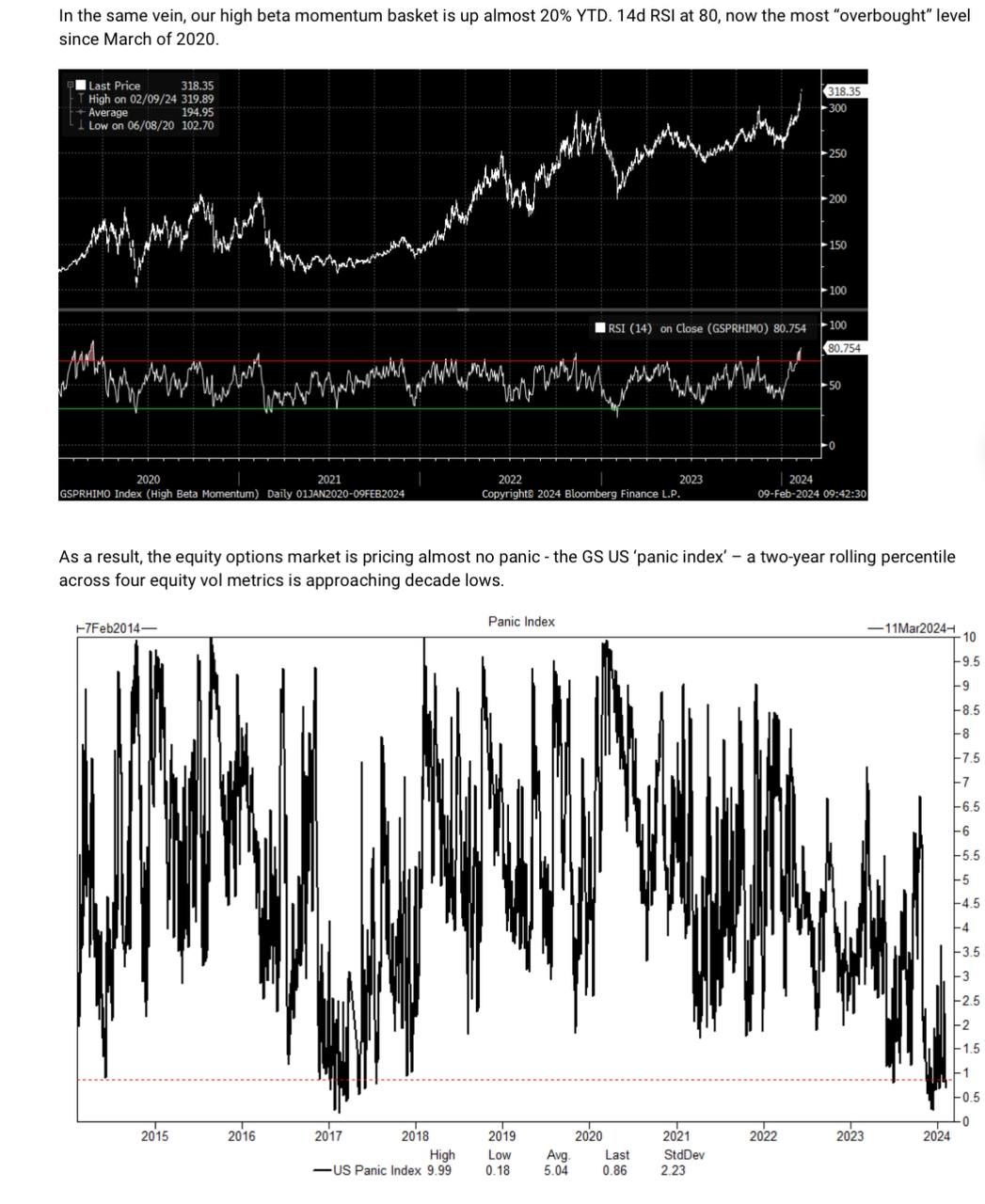

1) High beta momentum stocks are up 20% YTD. They have not been this overbought since March of 2020. That parabola will correct.

2) Signs of complacency. The Goldman Sachs ‘panic index’ is approaching decade lows. Recall, last summer, the volatility index was also quite low. (This is good in the sense that the cost of insurance is cheap.)

That’s also true for the VIX index which measures Fear in the stock market.

This study shows how the VIX spikes over various timeframes.

Buying VIX calls with a 3 to 4 month window is a cheap way to hedge, or perhaps puts on the Nasdaq 100.

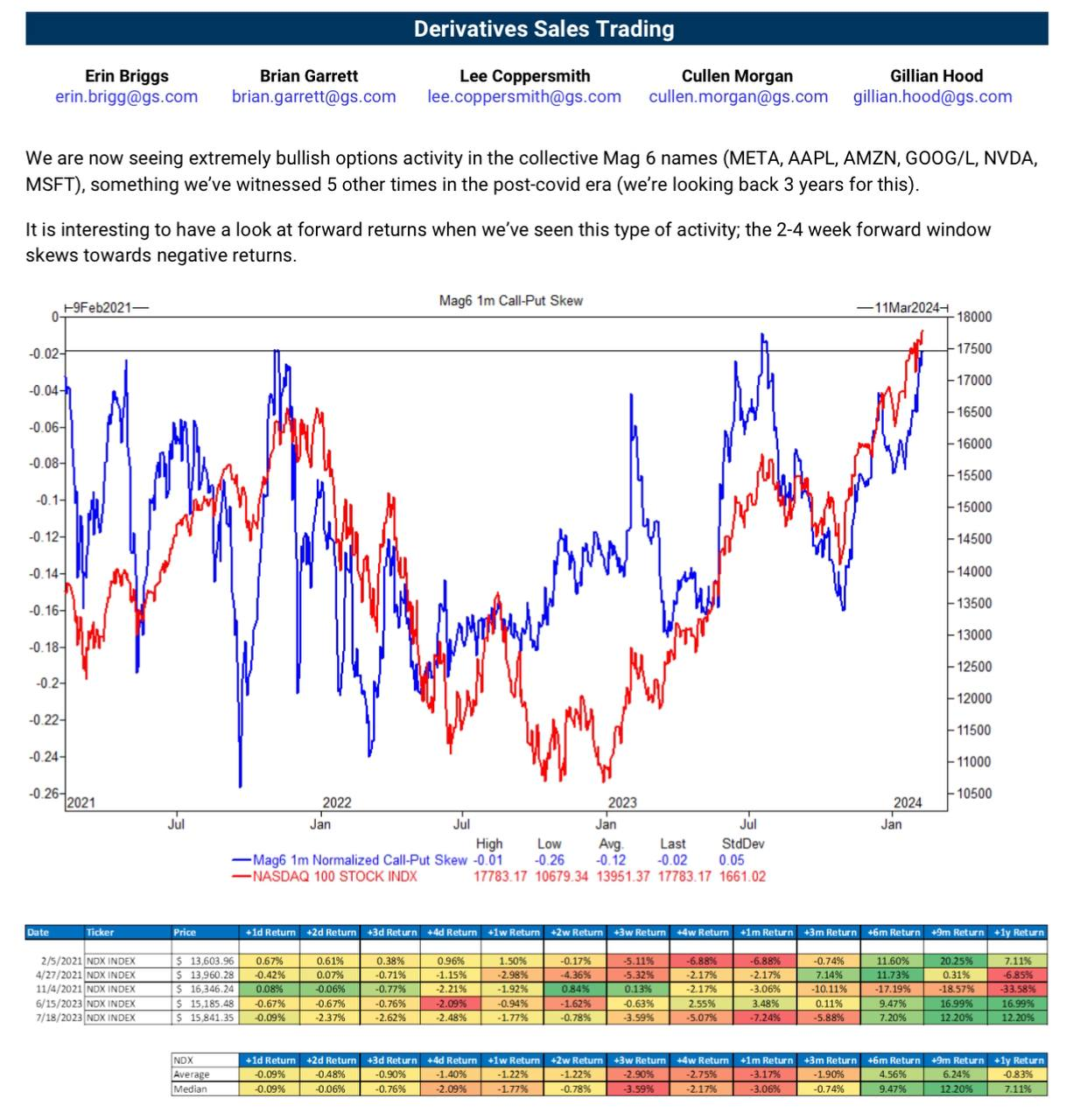

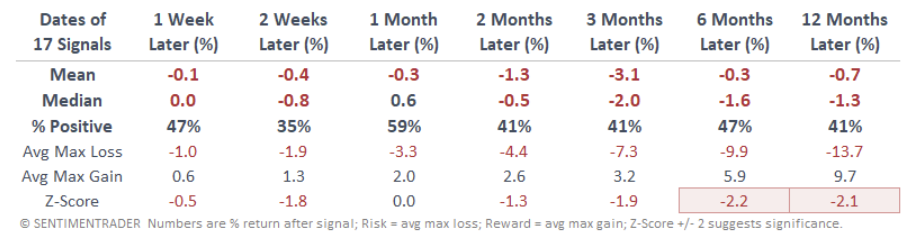

3) There is extremely bullish options activity in Mag 6 (META, APPL, AMZN, GOOG, NVDA, MSFT). Investors are buying calls hand over fist.

Look at the chart below - what happens when the blue line (call demand) gets to this level, the red line (the Nasdaq) corrects. Those calls wind up going worthless.

The 2 to 4 week forward window of forward returns skews negative.

The forward returns are negative when you look out 2 to 4 weeks. The selling starts in over the next 3 days.

Source: Goldman Sachs

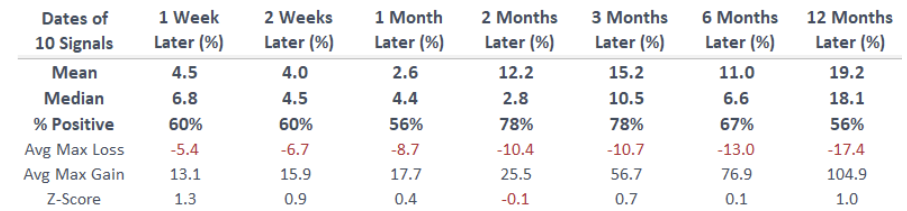

4) 52-week lows has been rising while 52-week highs are not rising on the Nasdaq.

We have a “split market”

Usually, when the Nasdaq hits an all-time high you see a 3:1 ratio of New Highs to New Lows. Here’s the forward performance the last time this happened:

Here we see weakness in the 1 to 8 week timeframe.

Note, there was a false positive in 1999 during the DotCom melt-up. Ultimately, those gains were given back a full-year later.

Said another way, if there’s no correction here, then the alternative scenario is a Melt Up.

We ran a poll on X to see whether people believe we are due for a Melt Up or Correction.

Mr. Market will find a way to make both ends of the spectrum feel like they are right at the worst possible time.

5) There are Ominous sounding warnings like the Hindenburg and Titanic Syndrome that are kicking off.

These technical warnings are increasing at pace not seen since December 2021 - that was within 1 month of the market top.

These technical studies indicated negative performance over a 6 month window.

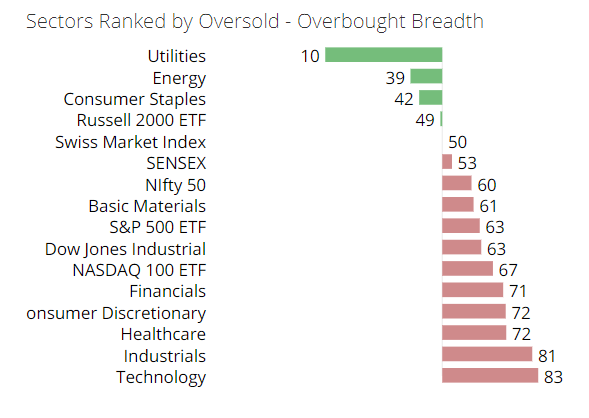

6) Deteriorating Participation & Breadth.

The percentage of stocks within the index holding above their 10-day, 50-day, and 200-day moving averages has been decreasing even as indices hit all time highs.

Once again, the returns look weak looking out 6 months.

7) Morgan Stanley’s Mike Wilson is no longer in the US Equity Strategist role. Recall he was quite bearish during the 2023 rally. Last summer when Mike issued a “We Were Wrong” report, US equities took a nose dive in a 3 month correction.

Similarly, JP Morgan traders are no longer listening to their head strategist Marko Kolanovic:

For the record, we think both those strategists were wrong. But now that people are completely tuning them out - it’s time to tune in!

Speaking of, JP Morgan has also completely flubbed the last two years

Be greedy when people are fearful, and fearful when people are greedy.

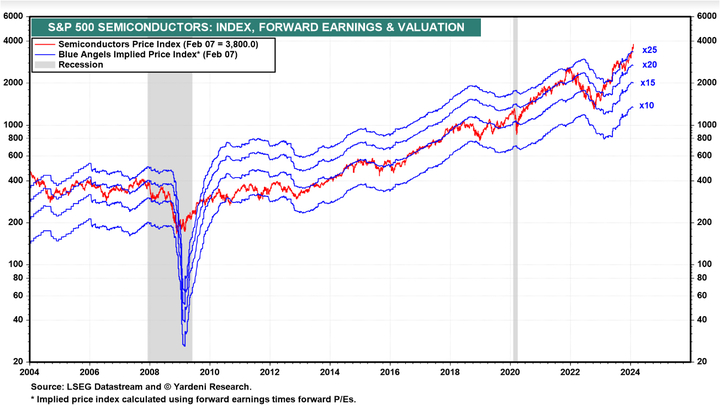

8) Semiconductor valuations are now fully priced

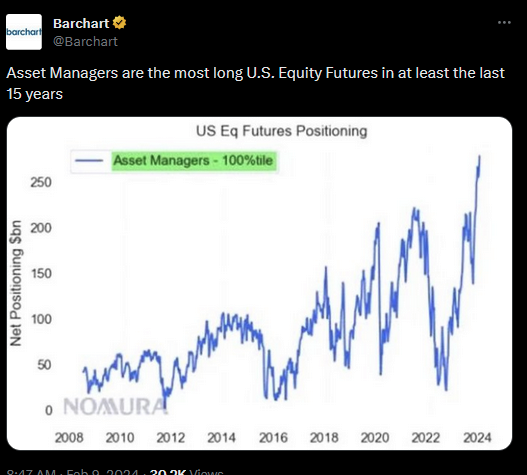

9) Asset managers have record long equity futures exposure. 15 year highs. Can they get more long? No. They can get less long. That’s called selling.

At the very least, these studies suggest the outlook over the next two weeks is highly unfavorable. So re-positioning promptly is a good idea.

On Friday, we shorted Apple and Oracle.

Nvidia is up 50%+ in the last 5 weeks. We’ll be selling that position which has worked so well for us. Nvidia is now Consensus.

We should note, Lumida has been long our investment themes: semiconductors, software is eating the world, nuclear renaissance and others. Mr. Market has rewarded our themes very well.

Mr. Market offered stocks on sale in October. Now, 5 months later, Mr. Market wants to buy the same stocks back from us at ridiculously inflated prices. We are happy to oblige..

On all our client accounts we are beating the S&P and QQQ YTD. So, we’re not perma bears or bulls. We just look at the evidence and adjust accordingly.

We also have positions in our portfolio that should benefit in case we are wrong. This is a crucial part of investing with humility. For example, we will look to deploy Nvidia proceeds in a semiconductor or other tech ideas that looks relatively cheap.

We have analytics organized by investment theme ready so we can easily identify where to focus next.

Markets Started to Get Sloppy

Most of the market action this year was highly disciplined.

Good stocks went up. Bad stocks - like Tesla and the EV bubble - went down. Bad semiconductors also went down.

Unprofitable tech went down.

This last Friday we saw major moves in retail momentum favorites like CLSK, Palantir, SoFi, Carvana, ARKK, HOOD, and AMC.

Positioning

On the margin, you want to own more of assets in the green and reduce exposure assets that are overbought.

Healthcare names like Eli Lilly are also overbought. Tech names - including those we own and have recommended - Nvidia, Palo Alto Network, Meta - are overbought.

Macro

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

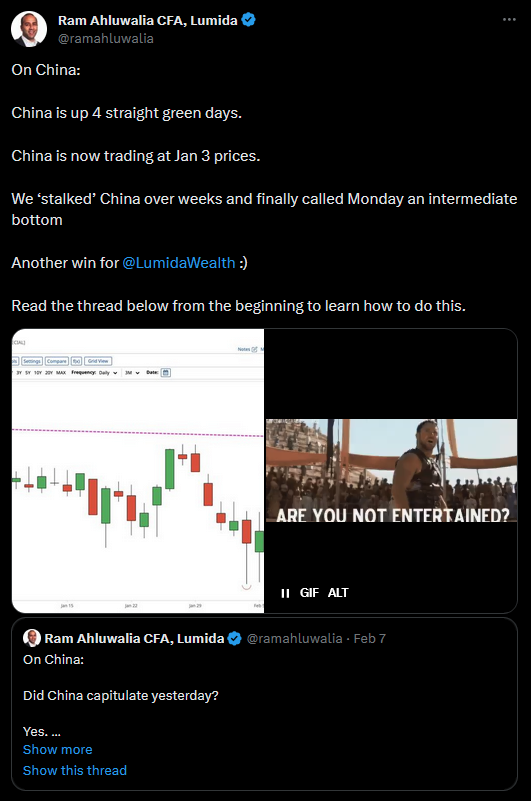

On China:

China is up 4 straight green days.

China is now trading at Jan 3 prices.

We 'stalked' China over weeks and finally called Monday an intermediate bottom

China is up 4 days in a row since our call.

Read the thread below to see how we covered China day-by-day in a ‘Capitulation Watch’.

Then we issued our Capitulation Call..

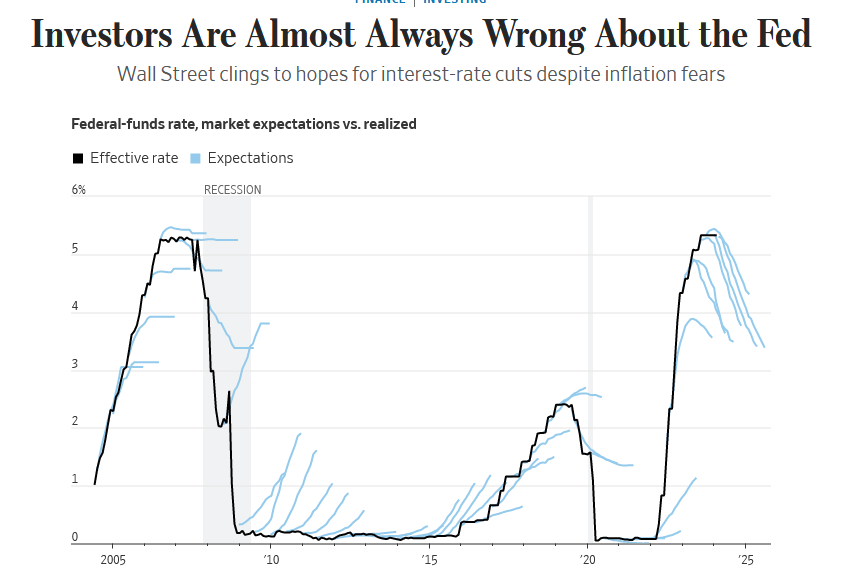

The Fed and Interest Rates:

We noted that the Fed will not cut rates in March.

This is a nice chart showing how Mr. Market is awful at predicting FOMC behavior.

Mr. Market is an emotional ball of wax and narrative.

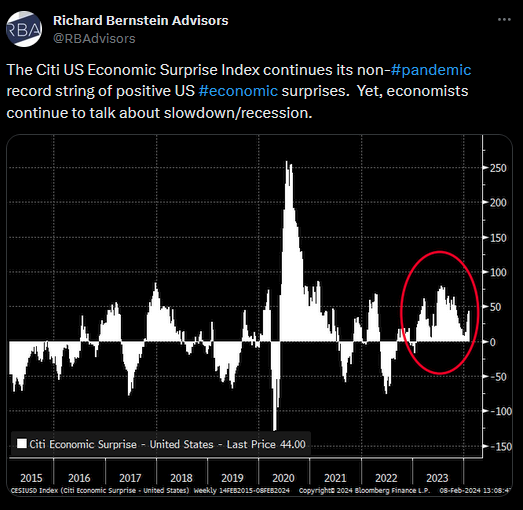

Economic Strength

The Citi US Economic Surprise Index continues its record string of positive US economic surprises.

Yet economists continue to talk about slowdown & recession.

We believe we will experience a correction within the context of a bull market.

Source: RBA Advisors

Markets

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Market Compass

Let’s cycle through our three-prong market compass as we look to the week ahead.

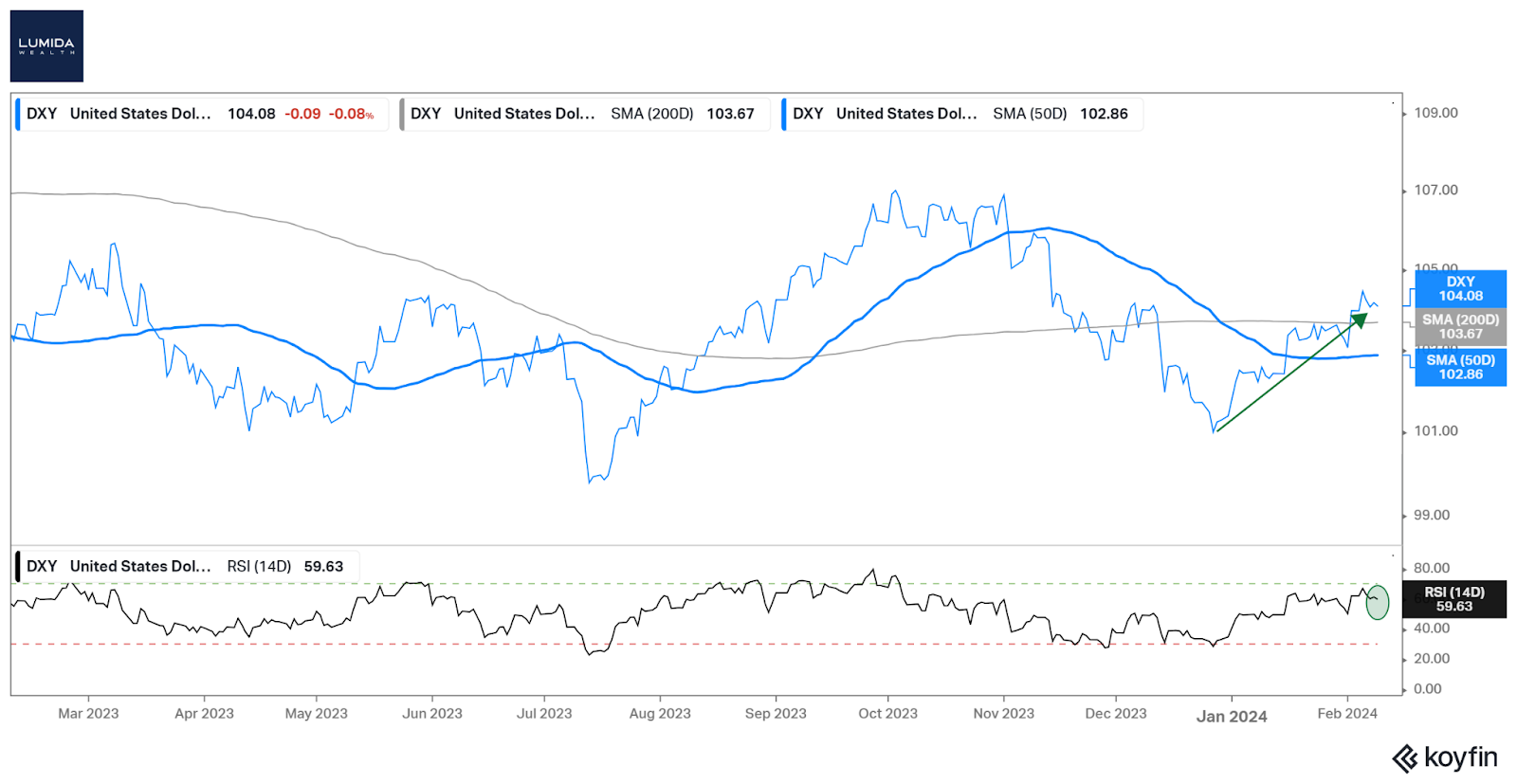

1. The 10 year bond yield increased over the week at 4.17%, up 15 bps WoW.

When this increases, that hurts valuations for long duration stocks.

2. The US Dollar is turning up, currently at 104.08 (Up by 2.66% YTD)

When the USD increases in values, US equities decrease in value.

That’s two strikes for risk off.

3. Semiconductors are up.

The SMH ETF moved up by ~8.6% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average.

NVDA is up ~50% YTD.

This looks like excess enthusiasm.

Take a look at the ETF - MTUM. It contains quality momentum technology firms:

That’s going parabolic also.

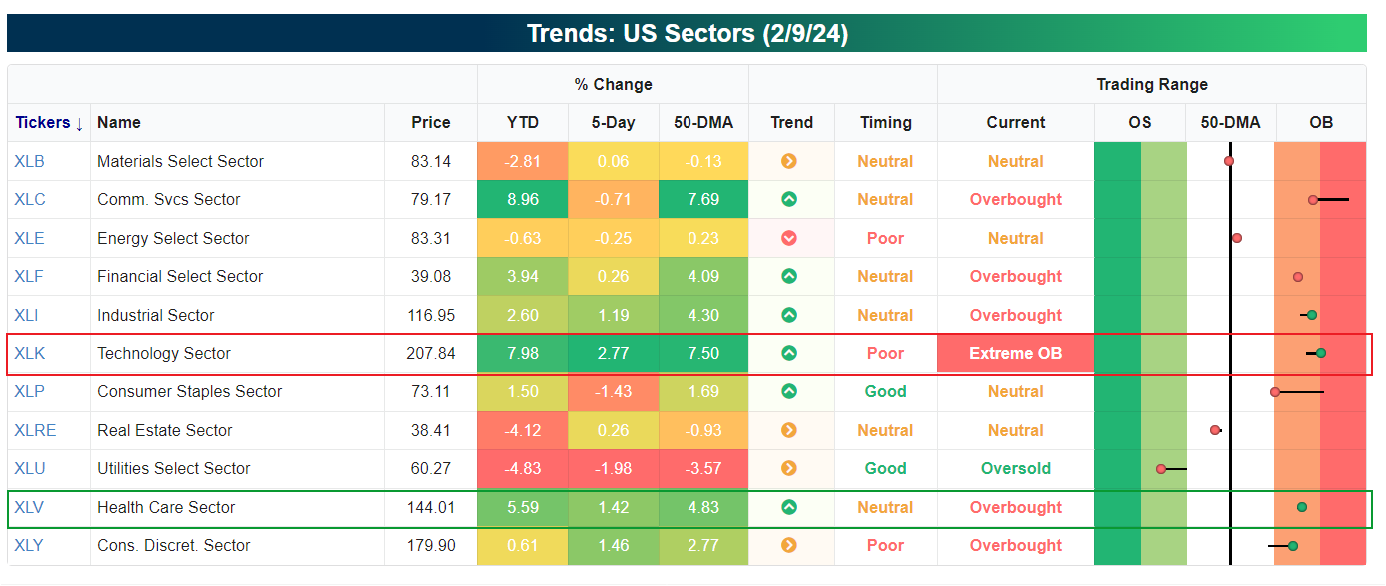

4. US Sector Trends

Technology and Healthcare are up 2.77% and 1.42% respectively, since last week.

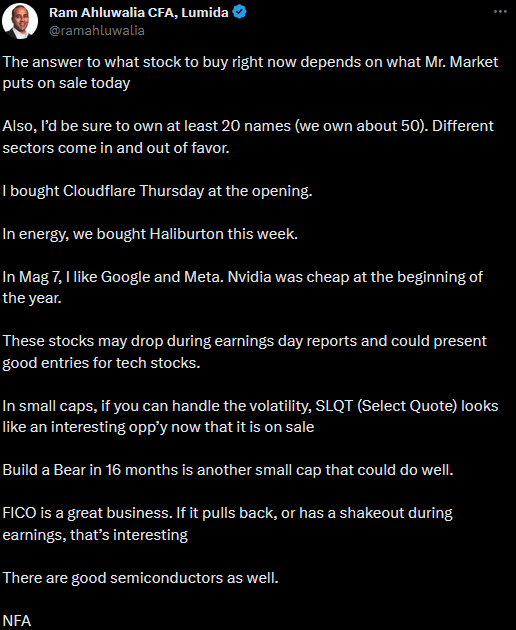

Lumida Calls:

We wrote this on the weekend of 1/22:

'In small caps, if you can handle the volatility, SLQT (Select Quote) looks like an interesting opportunity now that it is on sale'

SLQT:

1/22: $1.07

2/9: $1.41 on strong earnings

That’s a 31% gain since we wrote that call on X in 3 weeks - we'll take it.

It's not just a Mag 7 market folks.

Small caps should outperform tech in the months ahead.

We wrote about small caps in the @LumidaWealth newsletter... There is a lot to do in this category.

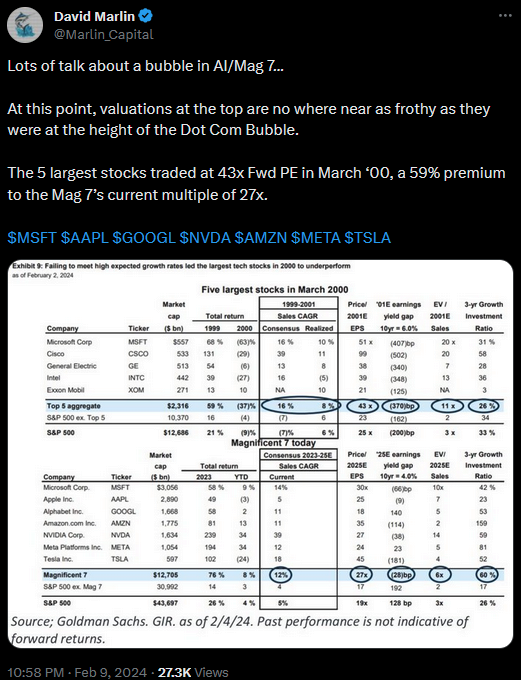

This is Not the DotCom Bubble

In the DotCom era, the 5 largest stocks had a 43 forward PE ratio in March ‘2000 - the peak.

That’s a 59% premium to the Mag 7 multiple of 27x.

Greenlight’s David Einhorn says Markets are Broken

Bloomberg: "David Einhorn says Markets 'Fundamentally Broken' by Passive Quant Investing'

He's correct.

For example, Lumida Wealth we have published 13F trackers based on our analytics.

We get to ride on the research of sharp hedge funds for free.

We can see Einhorn's positions in the context of dozens of others and generate 'meta' views around positioning.

We can see specialized HFs building up positions, or bad funds like ARKK dumping positions.

That gives us an advantaged starting point when we do our research.

We have tools that measure retail sentiment.

So, we have a sense of when the crowd is getting into a feverish binge.

The tools aren't perfect, but they do deliver measurable value added.

We use a variety of quantitative tools that help us identify opportunities, sectors, and factors that are interesting.

Lumida’s Quantamental Approach

Our approach is not pure Quant, but it is highly informed by Quant.

We are 'hybrid'.

The approach is 'Quantamental' - I combine quantitative systematic techniques with bottoms-up fundamentals and top-down themes.

If you take a strong chess player and pair them with a decent computer, they can beat any Grandmaster.

We can run faster than Goldman Sachs, JP Morgan, or Morgan Stanley because we have analytics and a framework for idea generation and hedging.

That's quantamental.

The human element still matters. Humans generate the top-down themes.

Machines can't 'see' themes like 'Aging Demographics'.

Humans also identify idiosyncratic value (e.g., stock picking within a sector due to qualitative business assessment).

Quant tools help there also though by allowing us to reject ideas quickly.

And we have the quantitative tools that help us identify where to focus and how to blend ideas into a portfolio.

It's a unique homegrown approach that I believe represents what Modern Investing should look like.

There are several 'edges' in this approach.

We can see how HFs are positioning. We can see what retail investors are doing.

We can measure whether momentum is working or not.

Fun Fact: In a former life, I used to build and run statistical arbitrage strategies and co-hosted the NYC Quantitative Reading Group some 10 years ago - a small group of quant investors from Two Sigma, Morgan Stanley, and other leading funds I can't name.

You can go to http://quant.stackexchange.com and look up my posts there if you want to DD :)

Our approach is to combine:

- the fundamental underwriting you get from a CFA (that's the 'idiosyncratic value')

- the top-down thematic approach that VCs and PE funds use (machines can't see the world at this level - you need a human to say 'AI theme' or 'Semiconductor capex receiver thesis', ‘nuclear reinassaince’, ‘Aging demographics’, etc.)

- The quant factor models which enable us to construct portfolios and position size

- Quant overlays for technical entries / exits

The key overlay is Non-Consensus.

That's a good summary of our approach which I believe is highly original.

Asset Managers are the most long U.S. Equity Futures in at least the last 15 years

On Cathie Wood and ARKK

Headline: ‘Morningstar Calls Cathie Wood ARKK Wealth Destroyer’

I have strong opinions on ARKK.

We regularly go thru ARKK’s holdings to find good hedges and short ideas.

Why?

ARKK’s investment skill, as evidenced by performance, is objectively awful

ARKK is an asset gatherer, not an asset manager.

Ironically, ARKK does have good big picture themes.

I agree with many of them.

But, their expression is off target.

Examples:

1. They buy Tesla.

I shorted Tesla, and bought On instead.

Made money on both.

2. They buy SoFi. We shorted SoFi, and bought nCino - a true ‘tech platform’

Made money on both.

3. They buy bitcoin.

I bought discount to NAV funds at a big discount to get a better entry.

Made money on that too.

4. They bet on Beyond Meat.

We shorted BYND and bet on Hershey’s.

Ditto.

5. They bet on biotech via Gingko.

We bought pharma Novo Nordisk (and other biotechs).

And all of the above you can evidence by looking up the tickers on X posts.

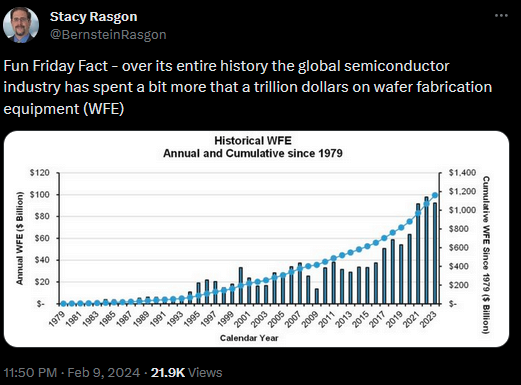

On Semiconductors:

The global semiconductor industry has spent a bit more that a trillion dollars on wafer fabrication equipment (WFE)

That’s bullish for names we own such as ASML that provide the lithography equipment to foundries and other component suppliers.

On Google:

When Google dropped 8% on earnings did you buy?

Or, did you let your amygdala take over?

The vast majority of people reading this saw the opportunity and invented logical sounding reasons to do nothing.

David Hume: ‘Reason is slave to the passions.’

Meaning, we have a feeling first then invent justifications to match to the feeling.

Most people get a deer in headlights response and cannot act when they need to.

Instead, they will FOMO at ATH thinking that’s ‘safer’

Self-deception is your own worst enemy and why professional investing adds value.

Take a look at Google since then and scroll down for our buy call.

Up every single day since then.

Ditto for our China call.

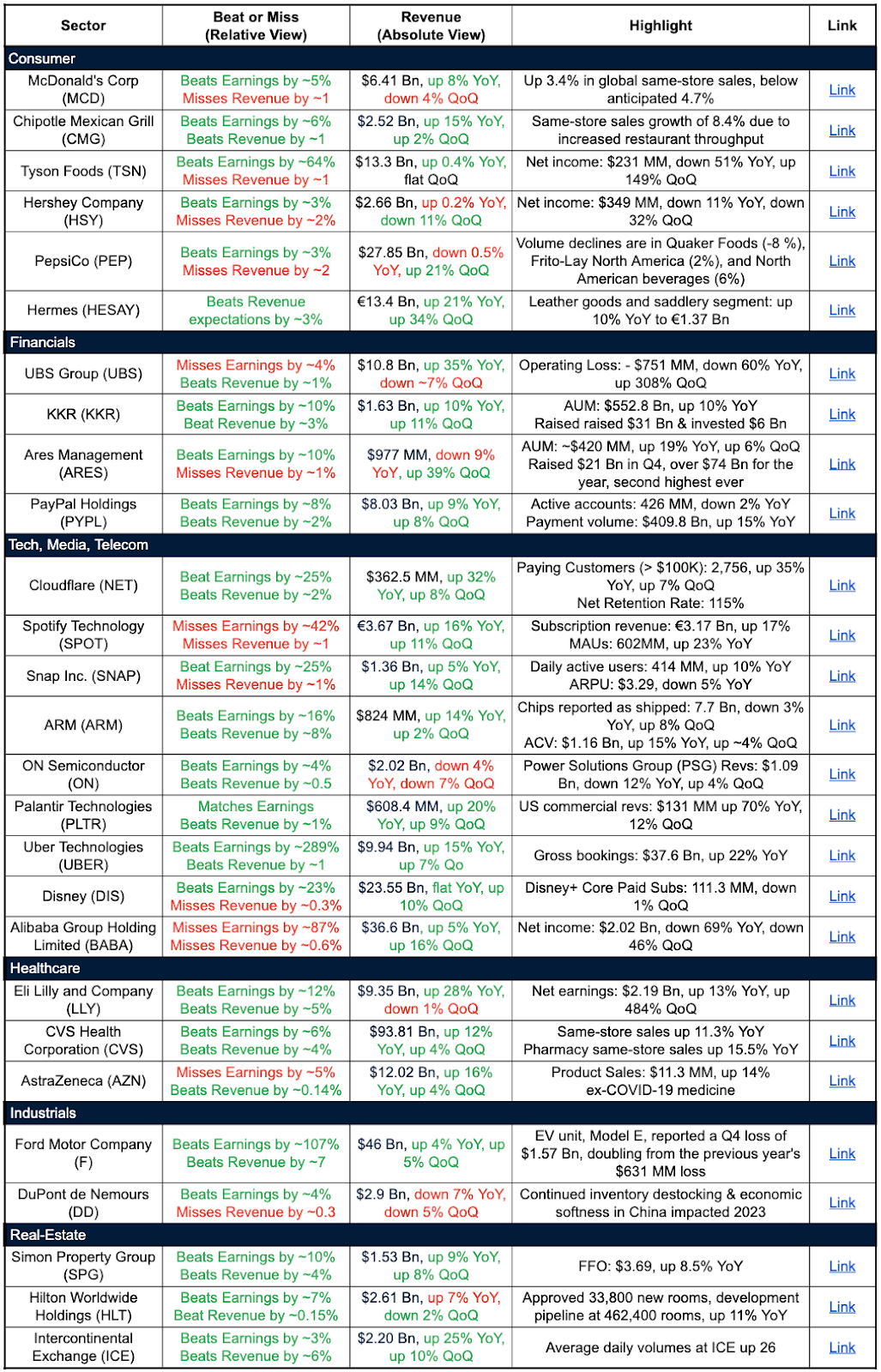

Company Earnings

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Broader Trends observations this earnings season:

Sellers to China are feeling the pinch

We saw this with Apple, Nike, and Starbucks

Consumer:

Companies reported: McDonalds (MCD), Chipotle (CMG), Hershey’s (HSY), Pepsi, Hermes (HESAY)

Mass consumer companies (McD, PepsiCo) faced slowing demand growth with many missing revenue expectations

More Premium & luxury brands (Chipotle, Hermes) saw strong growth

Industrials:

Companies reported: F, DD

Automakers are seeing solid demand but are challenged by EV investments

Broader sector facing inventory corrections, China weakness

Tech, Media, Telecom

Companies reported: NET, SPOT, SNAP, UBER, AAPL, AMZN, MSFT, META, NFLX

Trend:

Solid user and subscriber growth at digital media platforms like Spotify and Snap, but some challenges monetizing users

Cloud services still seeing strong growth

Digital advertising growth is still healthy

Financials:

Companies reported: UBS, KKR, ARES, PYPL

Increased capital raising and deal activity fueling strength in AUM, at firms like KKR and Ares Management.

The digital payments sector is seeing continued user and payment volume increases (PayPal).

Travel & Freight:

Companies Reported: UAL, AAL, UPS, ODFL

Trend:

Reported strong earnings, however, revenue was down QoQ, (suggests a slight decrease in demand for air travel)

American Airlines, achieved its best-ever Q4 and full-year completion factor, with the lowest number of cancellations

Decline in freight volumes, challenges in logistics and supply chain

Chip manufacturing

Companies Reported: INTC, ASML, LAM, AMD, QCOM

Trend:

All companies beat estimates on earnings and revenues

Revenue is up QoQ across all three companies, with only LAM being down YoY

Real Estate:

Companies Reported: SPG, HLT

Strong performance and growth in assets like malls (Simon Property), hotels (Hilton)

AI

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

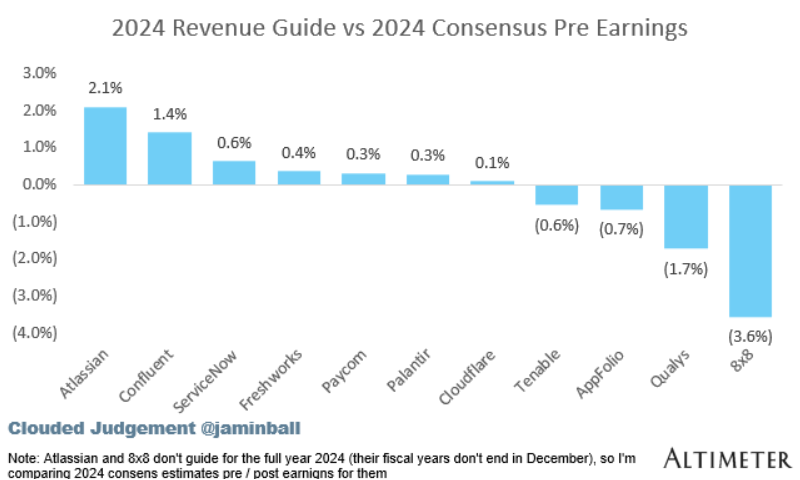

SaaS- Altimeter Highlights

Despite significant stock price movements (e.g Palantir and Confluent both up 30%, Cloudflare up 20% after hours), there hasn't been a substantial change in forward estimates for 2024.

Companies like Confluent (+1.4%), Palantir (+0.3%), and Cloudflare (+0.1%) have only slightly adjusted their revenue guidance.

This suggests that while valuations are rising, short covering and AI sentiment are driving the market higher.

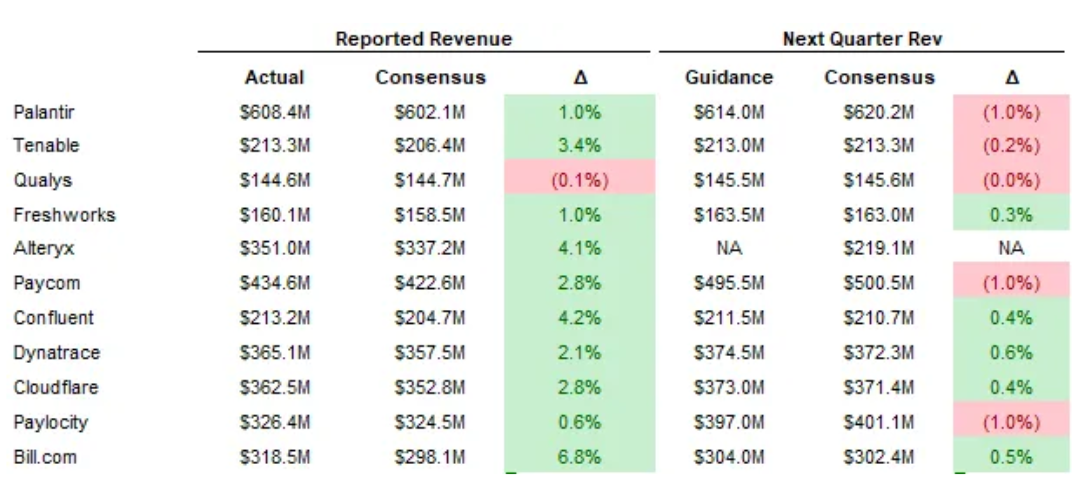

Quarterly Reports Summary

Digital Assets

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

CLSK had a 30% short squeeze on their earnings report.

When CLSK and other names start to roll-over, that’s when a correction in Bitcoin miners should start.

Coinbase reports this Thursday. Coinbase should benefit from higher ETF adoption. But, ETFs do eat into Coinbase’s revenue from enabling Bitcoin and Ethereum trading.

The custody fees are ~10 bps as compared to 1.5% from Bitcoin and Ethereum trade facilitation.

Over time, unless US consumers want to trade altcoins that do not have ETFs, this should pressure Coinbase.

We recommend looking at on-chain data to get a sense of how Coinbase should perform on earnings.

We would fade positive over-reactions (meaning a large pump) like we saw in CLSK.

Note: We do have certain altcoin positions we like. And we can enable crypto investing as a service thru a non-custodial mechanism. Reach out if you’d like to learn more.

Quote of the Week

“In a rising market, everyone makes money and a value philosophy is unnecessary. But because there is no certain way to predict what the market will do, one must follow a value philosophy at all times.” – Seth Klarman

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.