- Lumida Ledger

- Posts

- Markets in Q1 2024: Traffic Jams & Rollercoasters

Markets in Q1 2024: Traffic Jams & Rollercoasters

Justin Guilder & Ram Ahluwalia

January 07, 2024

Welcome back to the Lumida Ledger. Here’s a preview of what we cover this week:

Macro: Fed in a bind, Left tail risk, Goldman on Housing

Markets: Q1 Rollercoaster, Biotech breakout?

AI: AI’s adolescence in 2024

Digital Assets: BTC ETF - Buy the Dip, Sell the News or On to New Highs?

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

In Defense of Decentralization

This week we published an Op-Ed in the American Banker: In Defense of Decentralization with Anthony Scaramucci (Skybridge Capital) and Omid Malekan (Adjunct Professor, Columbia Business School)

Please Retweet and help me get the word out.

It's time to go on offense on crypto policy.

This op-ed lays out the intellectual defense for decentralization.

The op-ed answers the question of why decentralized blockchains are superior to centralized chains - which are merely glorified databases.

We discuss the incentive and game-theoretic properties of a decentralized chain and how they could have:

(i) prevented the Libor rate rigging scandal, and

(ii) helped overcome the lack of transparency in the 2008 subprime securitization market.

Moreover, decentralization opens up capital and innovation across the long tail.

It's time to go on offense and win the battle of ideas

Read the full Op-Ed here or email us for a copy.

This tweet also has an excerpt.

What’s on your Mind

Lumida is off to a great start!

Last weekend, and over a flurry of twitter posts, we made the case that Tech is poised to correct.

Tech started the year at a 99%-ile valuation. And, more importantly, everyone is long.

When there’s no one left to buy, markets drop.

And that’s what happened.

Listen to this video to understand more of Ram’s Non-Consensus Investing philosophy.

Ram and Justin also discuss:

Why Lumida went sour on Apple in the summer ‘23 and why we expect it will lag Mag 7

Google

The new AI form factor

The danger of growth stock to value stock transitions

Lumida Issued a “Market Call” on Twitter on the First Day of Trading

We acted on the research we had built over the recent weeks - including the observation that tech stocks are at a 99%-ile valuation, and sentiment was at a local peak.

This is what we wrote - and we’re pleased to report the implementation was successful.

Market Call:

We have been building our thesis on Tech in the last few weeks.

Tue Jan 2 11am: “We believe Mag 7 lags in January and tech (including semiconductors) is due for correction.”

On Apple: Remember last week how QQQ was approaching all time highs - but without Apple?

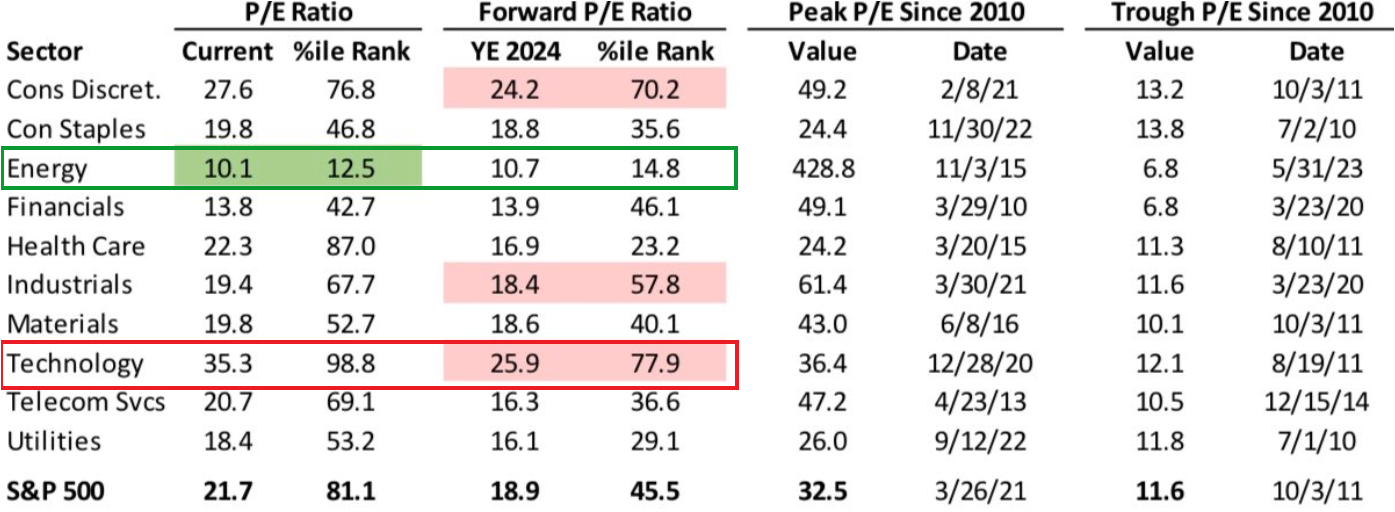

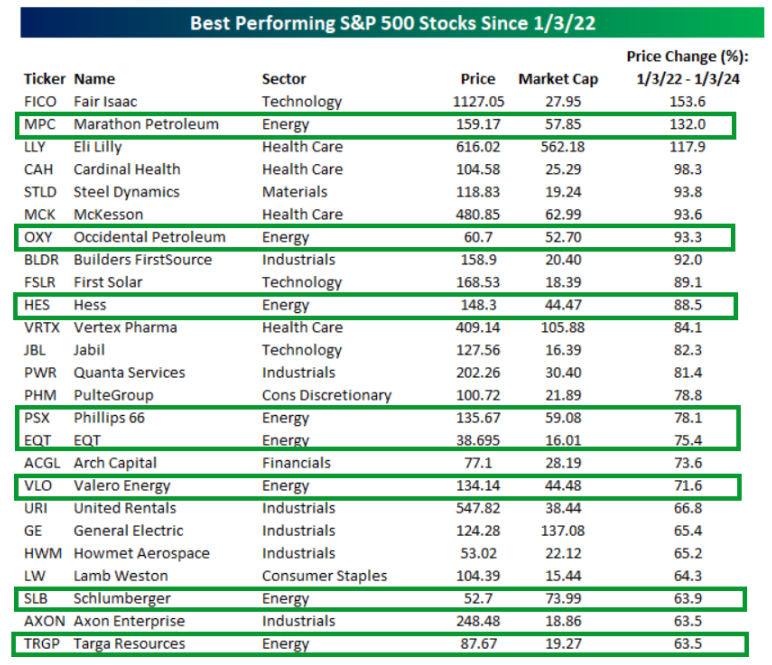

Study this table - where do you see value friends?

Remember, energy is a hedge on technology - they are negatively correlated (unlike bonds now). And energy is a hedge against rising geopolitical risk.

We are overweight energy, and underweight tech as of this Tuesday.

To my knowledge, Lumida is the only wealth manager that under-weighted risk the 1st week of August, went back to normal weight in October (buying semiconductors), then under-weighted Mr. Market in early January.

It takes a lot of skill, discipline, and obsession to pull this off.

We hope to do it again and humbly prostrate ourselves before the Market Gods for continued good fortune. :)

Look at Apple’s lackluster stock performance. Apple was lagging the Mag 7 in December - that was a subtle tell in hindsight that markets were weakening.

How do you have ATHs without the most valuable company in the world?

JP Morgan released their 2024 Outlook just shy of New Years Eve.

Their Outlook reminds me of the ‘magazine cover’ indicator.

JP Morgan was bearish all of ‘23 and missed an incredible year.

Now, those pillows are meant to represent a “soft landing”.

They top-ticked the market. Legacy wealth management firms are driven by committee and consensus. They are conservative - which paradoxically makes them riskier.

Remember when everyone said Apple was better than a money market fund? They perceive less risk - when we hear that we perceive complacency…

Legacy wealth firms are the same way. Advisors are emotional. No one ever got fired for recommending Apple.

Lumida’s Non-Consensus Investing Philosophy

Remember how the Goldilocks narrative was advancing in December?

You can’t get better than Goldilocks.

There is no ‘soft landing for longer’.

[ Unless you are Irving Fisher before the ‘29 crash: ‘stocks have achieved a permanently higher plateau… or Dotcom Era ‘This time is different ]

Now look at this headline: ‘Reverse Goldilocks’ from MarketWatch

We don’t have a crystal ball.

Rather than predict the future like these ‘equity market strategists’ who are wrong again and again…

We do the opposite.

We seek to measure what is right in front of my nose (e.g., Consensus)

That is hard enough!

When Consensus is solidified, that is when Mr. Market jumps to the next vine.

And if my Consensus read is correct, then I am there waiting on the vine for

Mr. Market to catch it rather than the other way around.

Rather than read the future, I am reading the present.

Which task is easier?

Non-Consensus is Content Neutral.

It is of the form ‘Not X’ where ‘X’ is Consensus.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

What Drove the Lumida Market Call on Tue

To quote Obi Wan, 'There is a disturbance in the force.'

Here's a walkthrough of what we were looking at and what's driving our Market Call.

First the Market Compass, which we share every week here in the newsletter.

1. The US Dollar is turning up. We highlighted in our last week's newsletter that USD is due for a bounce. Up by 1.13% WOW.

When the USD increases in values, US equities decrease in value.

2. The 10 year bond yield closes out the week at 4.05%, up 20 bps WOW.

We expect rates settle between 4 to 5%.

When the Ten-Year increases, that hurts valuations for long duration stocks.

The 10-year has tightened to 3.8% last month and is now heading back up to the 4%+ range.

3. Semiconductors are down.

Semiconductors are an expression of AI narrative.

That's headed down by ~5% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average.

We expect semiconductors will decline further. Nvidia will out-perform ASML and Broadcom - both of which are over-extended and we sold or hedged.

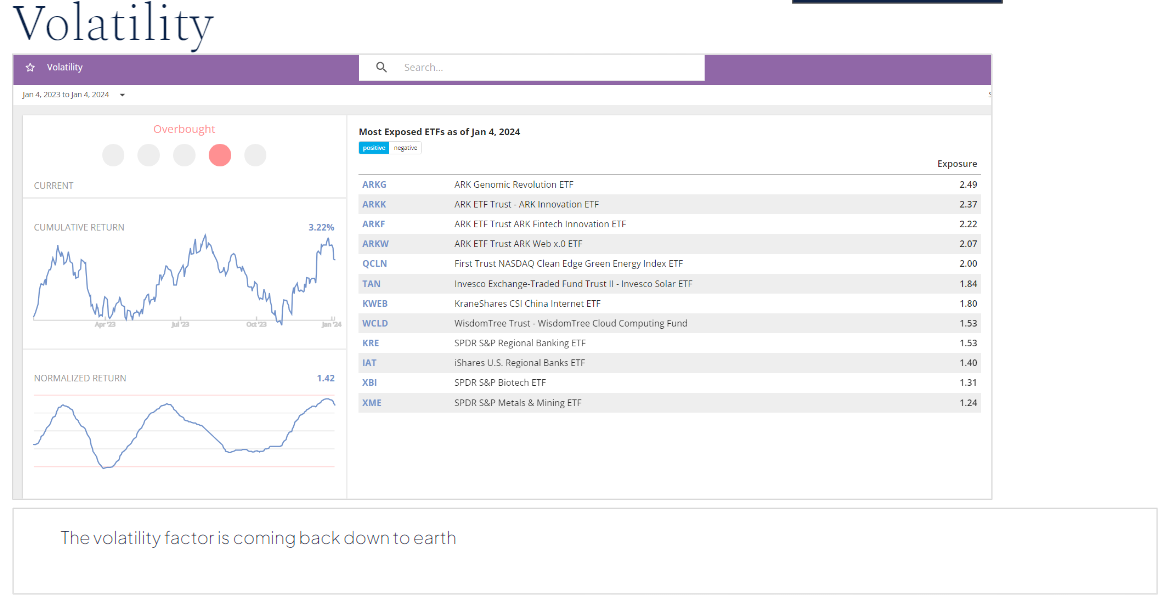

4. The Volatility Factor and Momentum factors are starting to mean revert.

This is a picture of the Volatility Factor - a quant equity factor that explains the cross-section of returns for many MoMo stocks.

What do you think is going to happen to stocks indexed to this factor?

We want to reiterate here that legacy wealth managers don’t think in terms of factors.

Our CIO is a recovering statistical arbitrage ‘quant guy’ and fuses that background with a fundamentals and sentiment approach to investing.

We believe this modern investing approach gives Lumida a competitive edge.

5. The 'marginal liquidity' stocks (e.g., MARA), which is a battleground crypto miner, is down after going parabolic.

6. Hedge fund shorts are pressing the advantage from Friday and following thru today.

7. Apple, a key leader in Mag 7, is down

8. Tesla is down big. Lost 4% on Friday alone.

Apple and Tesla are stocks we either don’t recommend owning or recommend shorting from time to time when as a hedge against our other names when markets are over-extended.

9. Stocks like Palantir, The Trade Desk, and Snow Flake achieved stratospheric valuations and have been trading down.

We pointed out Palantir was over-valued on 11/18 in this tweet

Palantir is down double digits since then.

These stocks are like ‘canary in the coal mine indicators' for animal spirits.

They are marginal liquidity markets.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

What’s Working

What's working today? Healthcare stock Elevance.

That was the healthcare stock we wrote about last week.

Hedging

I added a short to $SOFI on Friday just before New Years.

The stock dropped 20% - half of that after a downgrade on Thursday.

SoFi is a great management team, but it's just too clean of a macro hedge for us to pass up at stratospheric over-extended valuations.

People haven’t figured out that SoFi is a cheap macro hedge. It’s a balance sheet full of unsecured, first to default personal loans and has liquidity risk.

In a Risk Off environment that type of stock gets whacked

The 10-Year & Dynamic Hedging:

When markets go down 3 days in a row, often there is a relief rally.

We combine fundamentals, macro, sentiment, and technicals to perform a synthesis.

On the macro front - the most important chart for markets at this very moment is the 10-year.

It went from 3.8% to 3.99% for the last two days and broke out to 4.1%.

Our call is simple: the beatings will continue in equities until morale (stops) improving.

We noted on twitter, if rates exceed 4%, then that means more downside for QQQ.

We want to remain net long - but we will have a variety of small positions to help us hedge.

For example, we are hedging with shorts on Clorox and on First Solar. We keep those positions small. We prefer many small hedges over massive large hedges.

And we seek to avoid crowded consensus short because you can get a short covering rally.

There’s a lot to balance - we use (very expensive) analytics to help us approach this complex portfolio construction problem.

Again, we want to stress, this is what modern wealth management looks like. It doesn’t look like spending time on the golf course - it’s about stewarding wealth in a disciplined manner.

Here is a snippet from Ram’s personal account in case you are curious. Many of these names we have talked about before, right?

These positions were established within the last two weeks as we wrote about them on Twitter and in our newsletter.

Notice the diversity of bets across sectors and the avoidance of consensus shorts.

We covered our shorts Thursday morning?

Why? Rule of Thumb.

When markets are down 3 days in a row, expect a bounce.

That played out. Markets bounced Thu and Friday

The hedge served its role precisely.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Market Compass:

Let’s cycle through our three-prong market compass as we look to the week ahead.

1. The 10 year bond yield closes out the week at 4.05%, up 20 bps over the week.

When the Ten-Year increases, that hurts valuations for long duration stocks.

The 10-year has tightened to 3.8% last month. It’s now heading back up to the 4%+ range we believe.

2. The US Dollar is turning up. We highlighted in our last week's newsletter that USD is due for a bounce. We want to wait for the bounce, not predict it.

On Tuesday morning, we saw the USD surging - that’s exactly when we made our Market Call on Twitter.

That market call is a culmination of a thesis we have been building in this newsletter over the last several weeks.

When the USD increases in values, US equities decrease in value.

3. Semiconductors are down.

Semiconductors are an expression of AI narrative.

That's headed down by ~5% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average

How about Oil?

Yes, Oil is up to.

All of this data points to one conclusion: we are back to a risk-off environment.

What’s Our Longer-Term Outlook

We are still in a bull market.

We quote John Templeton : “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die of euphoria”

We are between skepticism and early optimism.

We are still in Phase 2 of the market rally.

Risk aversion is like a mimetic flu. People were excited, and now they are coming down to earth.

That’s what the volatility, momentum, and sentiment factors show - and the USD and so forth (our avionics) are telling us to consider.

Stay long.

Macro

Left Tail Risk

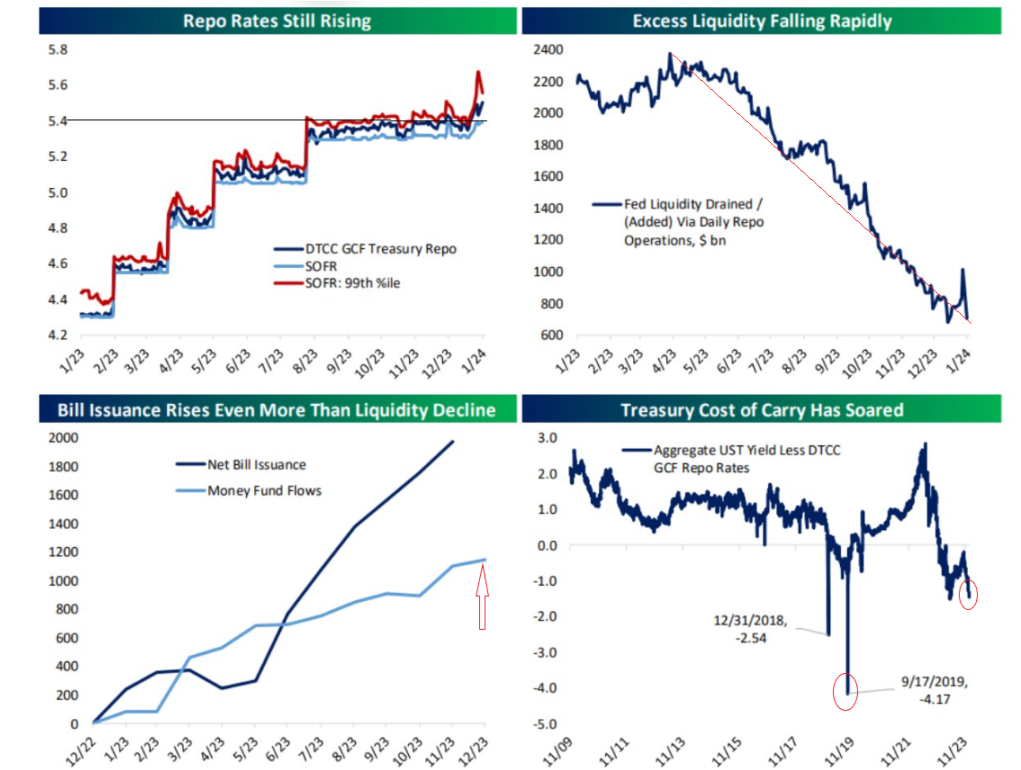

Imagine the financial market as a busy highway.

"Left tail risk" refers to the chance of a sudden traffic jam happening, where "liquidity risk" is like not having enough open lanes for cars to move smoothly.

"Credit risk," on the other hand, is like worrying about the cars themselves breaking down.

In the current scenario, the concern is not about the cars (credit events, like people not paying back loans), but about potential traffic jams (liquidity events, such as when it's hard to buy or sell government bonds quickly).

We are not worried about a ‘credit event’.

There is however a risk of a Treasury liquidity event.

The cost of financing a Treasury position is now 145 bps higher than its yield in aggregate. So, it's like paying more in tolls than the amount you get paid for taking the trip.

That makes further purchases of Treasuries less attractive given they now cost money to own for marginal buyers.

That creates upward pressure for rates.

It argues for rates going higher for longer.

If the Treasury market or repo were to break down, I would expect the Fed to intervene and create a liquidity facility.

The Fed will intervene if there is a breakdown in market infrastructure and execution.

Treasuries and repo markets are the base asset for capital markets. Both are like the main roads on the financial highway.

Not a forecast, we are simply highlighting that this is the left tail risk people should focus on - not rising consumer credit delinquencies.

No recession in sight

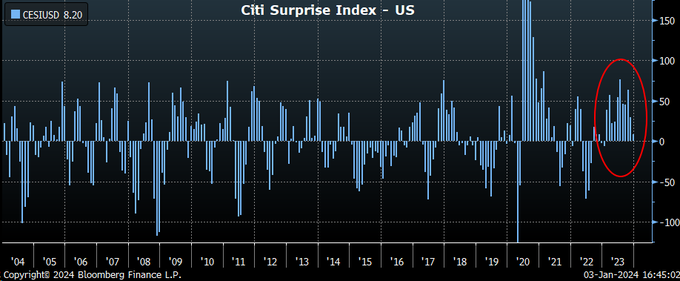

The Citi Surprise Index now has a record 11 months of positive surprises.

Yet economists continue to predict a slowdown/recession/landing.

This series is mean reverting and cyclical - just like human emotion.

Zoom in on that last bar - mean reversion at work.

Goldman on Housing

Despite the high rates in October, home prices went up by more than 8%.

The momentum is expected to carry into 2025, leading to an upward revision of home price appreciation forecasts to +3.7% from +2.8%.

That means consumer balance sheets, and their psychology, are strengthening.

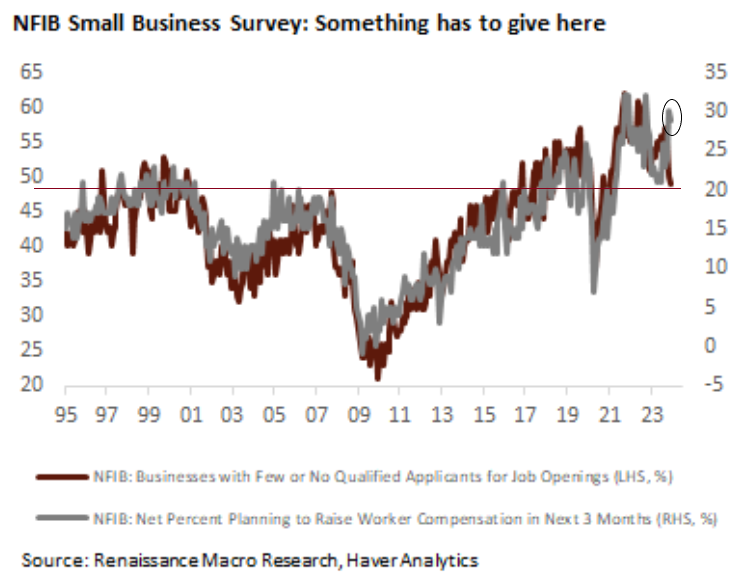

NFIB Small Business Survey - Something has to give here

It’s getting easier to find workers. Labor market is softening.

The percentage of firms saying that there are “few or no qualified applicants” for job openings sank to a new low.

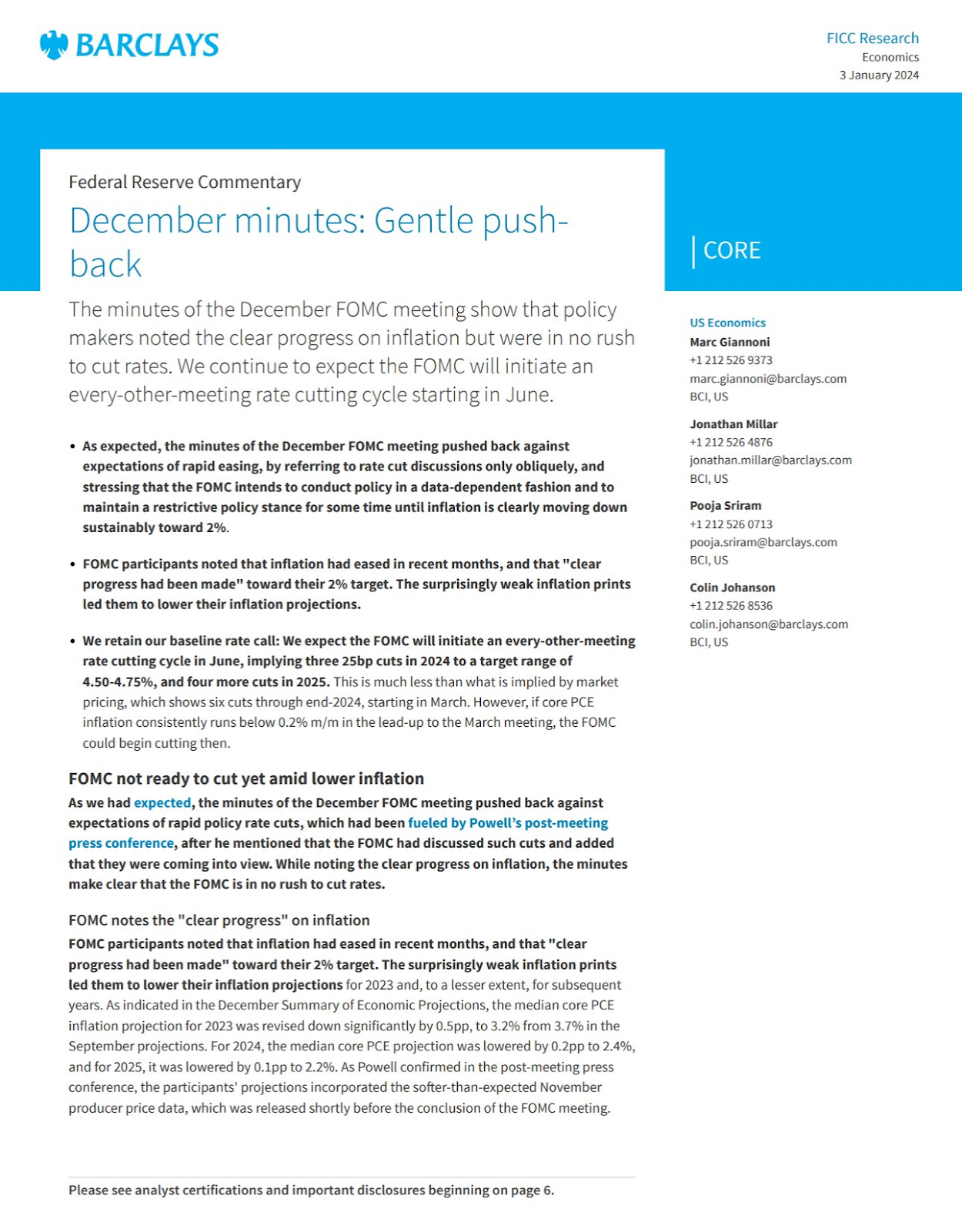

Fed Watch: Rate Cut Expectations in Q1 Are Declining

Remember the Dec FOMC meeting melt-up?

Here’s Barclays reacting to the Fed minutes: ‘Minutes of the Dec FOMC meeting pushed back against expectations of rapid easing, by referring to rate cut discussions only obliquely’

All that is getting unwound now.

The market read it wrong.

Scroll down and you will see how I tracked this variant perception starting from a deep non-consensus position.

We listened to the same call that day and said ‘The Fed is not pivoting’ - a non-consensus view.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Markets

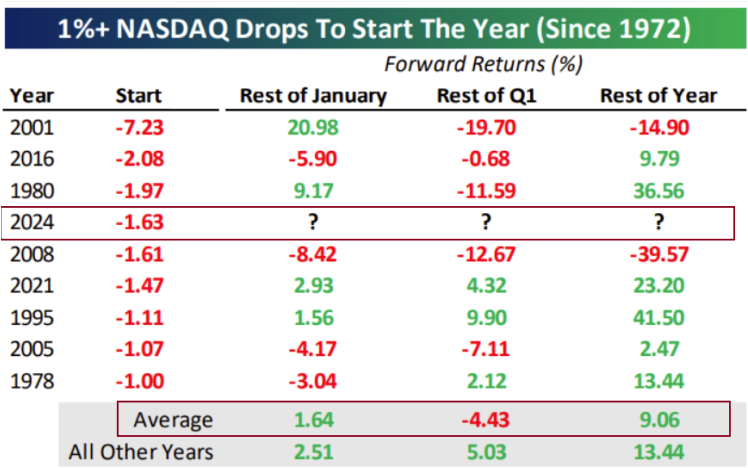

Expect a Weak Q1 Ahead

When the NASDAQ dropped by more than 1% at the start of the year (since 1972), the average return in Jan was 1.64%.

For the rest of Q1, the average return was -4.43%.

By the end of these years, the NASDAQ tends to recover, with an average return of 9.06%.

While a negative start to the year may indicate a rough Q1, it does not necessarily dictate the market's performance for the entire year.

We expect market returns to bounce back later in 2024.

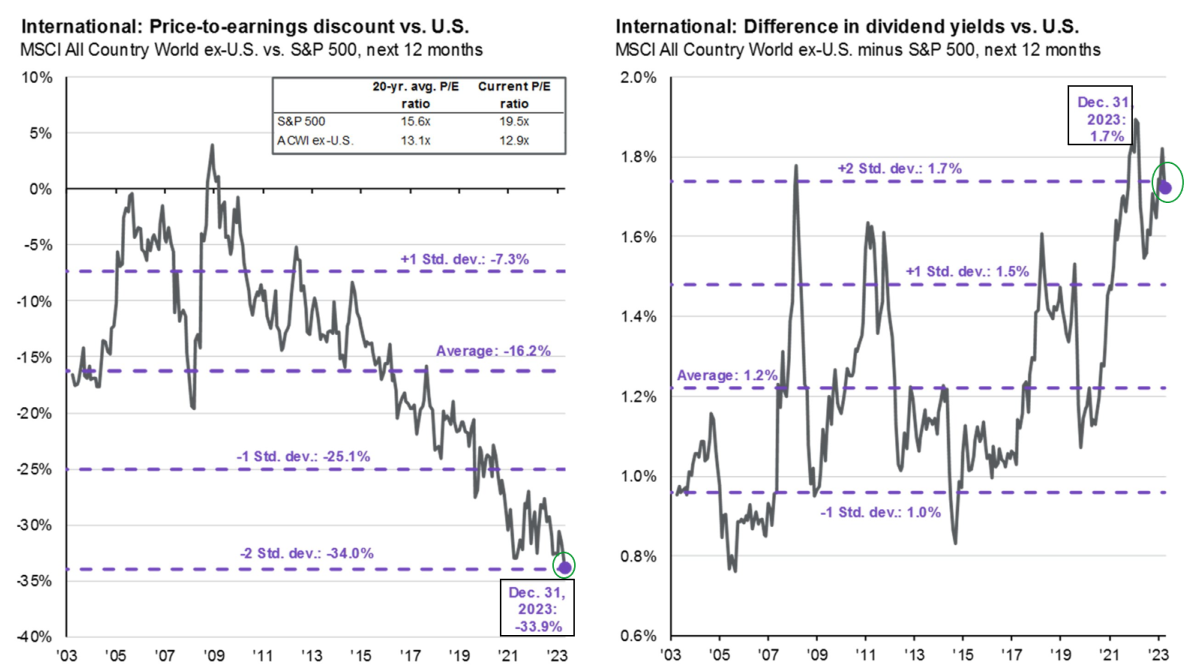

Fresh lows in the ex-US stocks P/E ratio vs US

S&P 500 P/E ratio is higher than the 20-year average at 19.5x (Avg P/E: 15.6x).

Non-U.S. markets are getting cheaper relative to the U.S. market.

As of December 31, 2023, international stocks show a substantial -33.9% discount to the U.S.

Also, the International stocks are providing a higher dividend yield of 1.7% vs US (As of Dec 31, 2023).

We suggest the significant P/E discount and higher dividend yield for international stocks could offer opportunity for conservative investors.

US Dollar strengthening likely means those markets benefit in the weeks and months ahead.

Biotechnology ETF (IBB) on the breakout

IBB on the breakout list after showing impressive momentum.

Equally impressive are the extreme ETF outflows which are historically a bullish sentiment set-up.

We believe biotech stocks can do a 30 to 50% gain this year.

The sector is on the verge of breaking out.

We think a pull-back is in order. We have our buylist ready and will be buying the dip.

This is a high conviction thesis from Lumida. Make sure you get your biotech exposures ready to go. Our prior newsletters discuss why we like biotech.

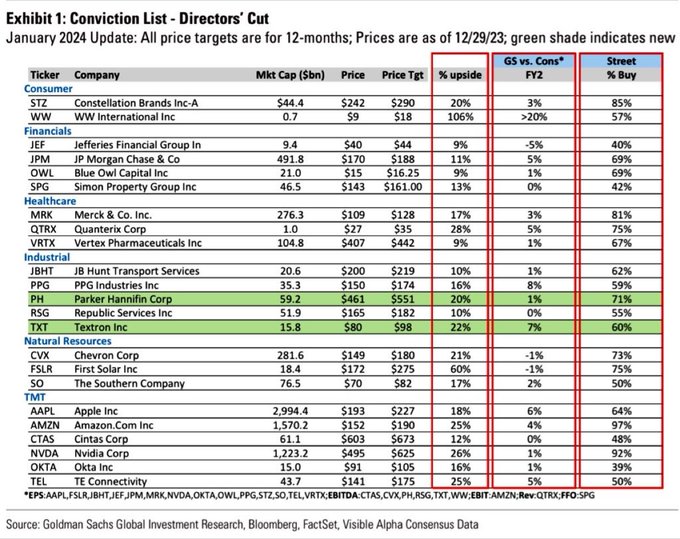

Lumida Reaction to Goldman Sachs “High Conviction” list.

1) Constellation Software (STZ): We own it in our model portfolio at Lumida Wealth.

2) JP Morgan: The time to buy was during the ‘banking crisis’.

It’s up double digits now.

JPM is expensive now, although if you are going to hold for 5+ years it is a good idea for stable dividend income.

Small well-capitalized banks with excess liquidity are a better move now.

4) Blue Owl: An interesting idea in the asset management space.

I prefer their competitor Apollo.

I can see the logic though.

5) Merck: A strong pharma company.

It’s a B+ idea - but a better move is BioTech.

Pharma needs to snatch up biotech as their IP pipeline evaporates in the back half of the decade.

M&A is starting.

Biotech was trading around net cash assets.

And the GLP1 theme and breakthrough is creating a powerful fundamental AND narrative machine around biotech.

Search for ‘biotech’ in my prior posts for more - we wrote about this when it was Non-Consensus.

In biotech we have 20 names give or take - one example we like: RCKT.

We also own Novo Nordisk and other names in healthcare more generally.

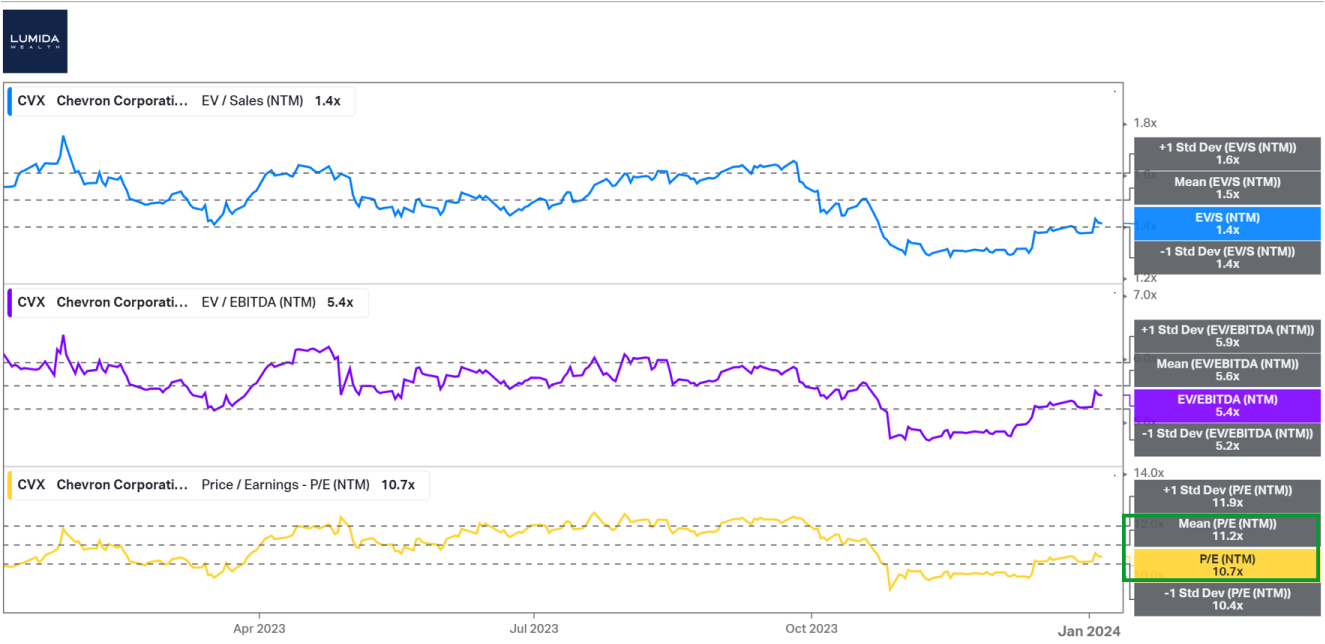

6) Chevron:

This is a dull energy pick.

Buffett’s OXY is better due to higher ROE.

There are so many better ideas: energy services, nuclear renaissance theme, Tidewater, Petrobras and others…

They’ve all done well and are reasonably priced.

7) First Solar: Bad idea. Full stop. Maybe even a tactical short at current levels.

8) Apple: Are you kidding me. No.

Apple has a higher forward PE than Nvidia.

Apple will lag Mag 7.

GS is the lead tech M&A banker.

Of course they like Apple - a highly acquisitive company.

9) Nvidia: Yes.

But there are better risk adjusted returns with smaller names in the semiconductor space.

10) Okta: No.

Fundamentals are starting to weaken.

There are many other ways to approach technology (Zoom, TEAM, etc).

No views on the other names.

Note: Big banks can’t cover small caps.

That’s your edge.

Semiconductors demand holding up and showing signs of strength.

We love semiconductors - it’s a thematic picks and shovels bet on AI without paying nosebleed valuation.

South Korea Chip Output Jumps:

• Production: +42%

• Shipments: +80%

• Inventories: +36%

Semiconductors like ASML and Broadcom are correcting now. They still have room to correct.

We’ll be buying them and others in the Lumida model portfolio.

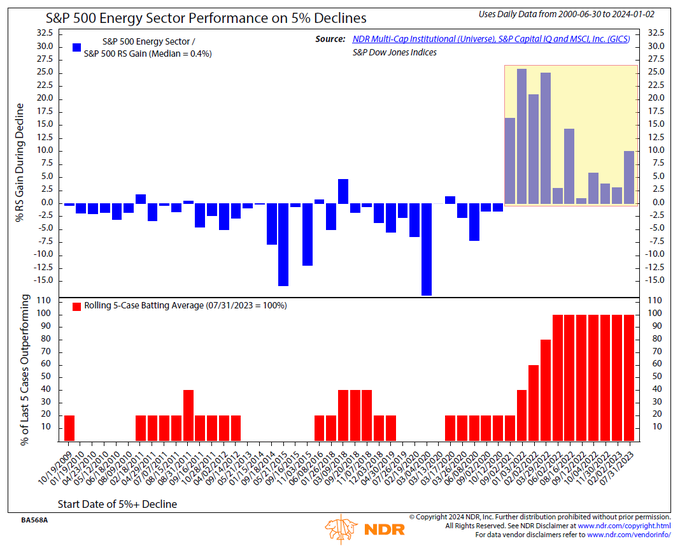

Energy Sector Performance

Energy looks to have carried its defensive attribute that started in 2021 into the new year.

The sector has outperformed in the past 11 S&P 500 declines of 5% or greater.

We like energy because it's a great hedge against tech stock decline and geopolitical risk. If oil prices stock, energy stocks should benefit.

Notice how many energy names are here. Normally, you pay for a hedge. Hedges have 'negative carry'.

Energy stocks have a positive carry because over time they appreciate.

If equities sell-off, energy will as well, but in the day-to-day volatility they can serve as the buffer that bonds once did.

AI

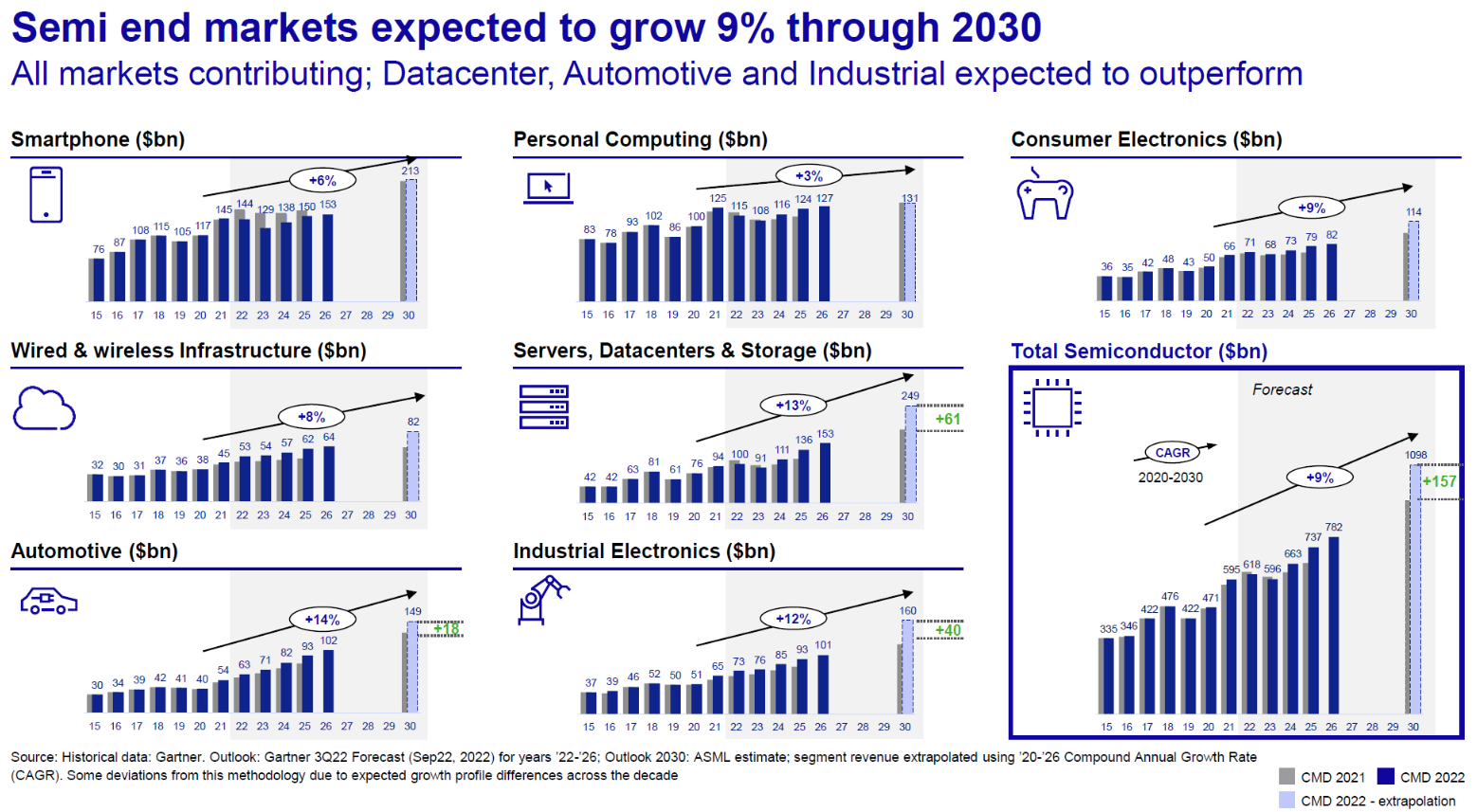

Semiconductor outlook: AI’s Adolescence

Semiconductors stocks made a new high in 2023.

The AI market is expected to reach $100 billion in revenue by 2024.

AI's rapid growth could lead it to surpass the size of the Smartphone and PC markets, possibly as early as 2024.

We like semiconductors - although many names are overbought here.

Nvidia should outperform technically vs other however at the current moment.

Lumida believes that the AI training and inference segments will become the largest semiconductor sub-market in the world in the next few years.

The PC and Smartphone market are each worth around $120-140 billion.

Even with a possible correction, the AI market is in its early stages and here to stay.

Digital Assets

BTC ETF - Buy the Dip, Sell the News or On to New Highs?

This week we had an incredible conversation with Alex Thorn (Galaxy HQ), Pranav (Van Eck) & Quinn Thompson (Maple Finance) on the recent developments surrounding the Bitcoin ETF.

It’s a must watch for those who want to know how to trade the markets, the importance of pre-positioning, what will actual flows look like? And how long after ETF approval?

Don’t forget to subscribe to our channel, every subscriber helps build our tribe so we can grow and deliver more great content.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Quote of the Week

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” – Philip Fisher.

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/orbe affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.