- Lumida Ledger

- Posts

- Investing as Surfing, Biden SOTU, Amazon goes nuclear

Investing as Surfing, Biden SOTU, Amazon goes nuclear

Ram Ahluwalia

March 10, 2024

Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Amazon goes Nuclear; Bank failures incoming

Markets: SOTU market impact; Tiktok ban; Factors Charts

Company Earnings: Cautious consumer spending; Software, semiconductor, & cybersecurity leading the way

AI: Cheaper LLMs; Claude 3; Uni-Founder Unicorns

Digital Assets: Alts season; BTC ETF in pension funds'; Lumida Crypto

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

This week, we talked with David Nikzad, an early investor and advisor to Y Combinator cohorts.

David has put first money into over 80 companies, including big names like AirBnB, Betterment, and more.

David started his career as a club promoter, moved to LA, started doing real estate investing, and found himself in Venture Capital.

Right now, David is leading EI Ventures, a company that produces health products made from natural psychedelics to help with mental health problems

We discussed topics like Non-Consensus VC, Digital Assets, AI Startups, and Psychedelics. Only a few people are skilled at both creating businesses and investing in these areas, and David is one of those experts. This is a must-watch—tune in below.

For those who missed the ETH Denver, tune in to our latest WOYM for the Debrief with Nick & Ishaan.

Macro

Humans Are Never Satisfied

Psychologically, humans want equity-like returns with bond-like risk.

Well, not even bond-like risk. Bonds are risky.

Humans want equity-like returns but with a perfect upward slope.

Humans want insurance products that throw off attractive returns.

Good examples of this:

- The structured products that blew up China's Evergrande

- 2008 RMBS

- FDIC insured high yield bank deposits

Assets that exhibit that pattern (the 'low vol' factor) get bid up more than other factors.

Assets that exhibit cycles and give their investors a roller coaster ride (like gold miner stocks, for example) are cheaper. Despite having more volatility.

And their returns are weaker than the low-volatility stocks.

Meaning investors are not compensated for bearing all of that volatility.

That violates the portfolio theory you learn in school.

School says 'riskier stocks should compensate investors by delivering a higher return'.

Don't take it from me...

The finding that 'low volatility' stocks outperform higher volatility stocks spawned 'Risk Parity' strategies.

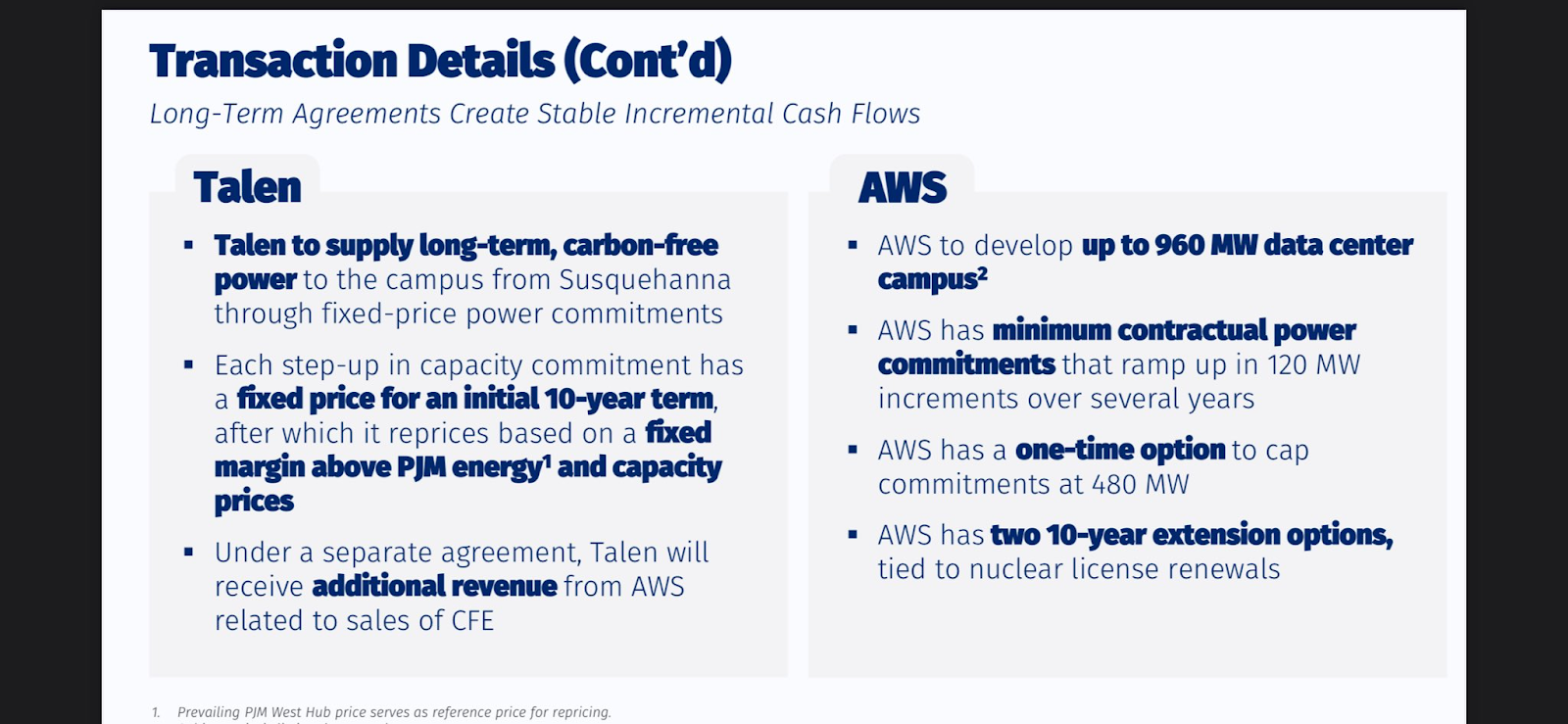

Amazon, Cloud AI, and Our Nuclear Renaissance Thesis

From Mark Nelson (Energy Analyst):

“Amazon just bought a massive data center under construction at one of America's best nuclear plants.

With the power demand for data centers soaring and major companies like Microsoft and Amazon now openly buying nuclear power to meet their needs, we are in the beginning of a new nuclear age.

Will the nuclear industry be able to meet this demand? That's the next challenge.”

It’s remarkable how many investment themes interact.

The rapid growth in Cloud AI has a tremendous demand for energy. That energy will come from nuclear.

We mentioned a few weeks ago our nuclear utility plan - Talen Energy.

Utilities were one of the few sectors on sale. We mentioned we bought this nuclear utility on Twitter.

Someone gobbled up a bunch of shares, and they are up 15 to 18% in 2 weeks. Unreal.

Amazon is working together with Talen Energy to meet its energy needs:

Fed Chair Powell on CRE

"This is a problem that we'll be working on for years more. I'm sure there will be bank failures, but this is not the big banks..it's more smaller & medium-sized banks that have these issues, we're working with them..I think it's manageable."

We believe we have found a small bank that will have major CRE issues. The stock is publicly traded.

We believe buying puts in August is the way to play it. You need time for the mark-to-market process to play out.

We don’t want to cause calling out banks with bad balance sheets, so we won’t name the ticker here.

We found the bank through our CRE connections. One of the contractors we know has a non-performing loan with this bank. And the bank has not listed the asset as non-performing on its recent filing.

The bank also is known for sloppy underwriting. I worked with them in the past so it was easy to get a handle on this one.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Markets

What’s wild is the big trends were on the earnings calls.

Here’s how we found Dell.

Nvidia’s earnings call frequently mentioned Dell as a distribution partner. We investigated Dell, which at the time had a forward PE ratio of 13.6 and double-digit cashflow and earnings growth.

We looked further, and it made sense.

I suspect ‘big famous tech portfolio managers’ don’t actually listen to the calls. They delegate to analysts and they miss the obvious trends and ecosystem effects.

Similarly, you could see Tesla’s margins eroding over the summer. They shared margin deterioration and China competition on their calls.

Similarly, Meta has enormous free cashflow generation capabilities - especially after headcount reduction.

If TikTok gets sold or banned, Meta benefits.

We do believe Google is an excellent buy here. We bought Google this Monday and Tuesday.

It’s been rallying since.

We were also pleased to see Bill Ackman join our Google thesis on the recent Lex Podcast.

You can see the best out-take clips from Ackman’s interview in this thread

Trump Bump vs. Biden’s State of the Union

We wrote this before the State of the Union address:

Hypothesis: There is a Trump Bump influencing asset prices.

Remember how Clean Energy peaked when during Biden’s campaign.

What’s the short term effect of the SoTU?

That should cause the Trump Bump spread to tighten.

Biden has home court advantage tonight.

Candidates get a boost after their conventions. Same idea.

Two ideas I am hearing:

- A buyback tax

- Increasing corporate tax

Here’s what happened.

Biden appears to have cleared a low expectations bar at the SoTU.

Markets sold off this Friday.

That supports the Trump Bump thesis.

If Biden gets a bump, then Trump vs Biden spread narrows, and markets trade down to reflect a larger risk premium.

Interesting way to look at markets.

Semiconductors whacked.

We noted semiconductors are overbought.

Marvell down 11% this Friday. Broadcom down 7%. Nvidia down 5.55%. ASML down 5.5%.

Don’t chase overbought stocks. Wait until Mr. Market puts them on sale.

There is a difference between ‘value’ and ‘price’.

Price is what you pay, Value is what you get.

We bought Atlassian’s Team on Thursday. It was up 2.8% this Friday.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

APEI stock is up 38% on earnings.

APEI, one of our small caps we wrote about in our stocking stuffer, had a ‘god candle’.

Congrats to all those that observe :)

APEI has given back some of those gains, but remains up strongly this year.

APEI is a good example of how a theme, factor, and security selection come together:

- Theme: Aging Demographics: Major shortage of nurses

- Factor: We want to own small caps at good valuations

- Security selection: ARR business model with strong fundamental growth trends in revenue and earnings, and a moat in the form of 'licensing' and brand

Start from the Macro finish at the Micro.

I first mentioned APEI in early December when it was in the $5 to $ 6-ish range.

Now it's $12.29 ish and change.

This is also another example of how diversification doesn't mean giving up returns.

Concentrate on the themes.

Then find the best expressions in the themes at good prices at that point in time.

There are about a dozen fantastic semiconductor businesses for example.

There are a dozen businesses we love in our aging demographics.

These range from in vitro fertilization, clinical software SAAS plays, and hormone replacement therapy to certain biotech plays.

There are ~5 businesses in our Nuclear Renaissance theme.

Not all of these are 'on sale' at any given time.

We have enough quality ideas that when we see a quality idea go on sale and want to increase thematic exposure, we can pounce on it.

On average, if we are skilled at identifying enduring secular trends and can identify winners in those themes before Mr. Market, we'll do just fine.

We can't control Mr. Market.

What we can focus on is doing our best to make a good decision and get a good entry.

On TikTok - Potential Ban:

Congress, for a change, may get TikTok right.

Who benefits from a TikTok ban?

1) Meta

Who buys TikTok if there is a sale?

2) Meta or Google

Will FTC seek to prevent Meta from Buying?

Yes. That favors Google.

@LumidaWealth owns both as top positions so win win.

We call these ‘embedded real options’.

3) What about SNAP?

They have insufficient marketcap to make a real bid

Note: If you don’t think foreign espionage is a real issue or don’t think social media is the new ‘soft power’ you really need to recalibrate your worldview

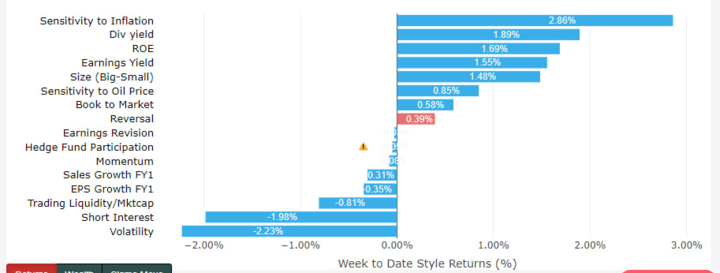

Market Factors

We like studying market factors to understand what Mr. Market is focused on.

Factor trends tend to endure.

The vibe this week is decidedly different from prior weeks

Here’s what we see:

HFs are not buying or selling

Short Interest and Volatility did not work - those factors were hurt hard. This measure in combination I think of as animal spirits. A lot of retail investors own stocks linked to these factors.

“Reversal” is working - that means mean reversion is starting to work again. For the last month, we’ve seen stocks jump up and go higher still (like ShakeShack). Now we are seeing stocks jump and give back gains (like APEI). This is a shift in market behavior. It suggests the tremendous bid in the market is softening.

The Momentum Factor is flat. This factor has been the most powerful factor in markets YTD.

We believe now is not the best time to deploy new capital into OB risk assets. However, there are opportunities within specific sectors—for example, we bought Atlassian TEAM this week.

But you really have to deploy well in this climate.

Notably, Broadcom had Marvel to 10% drops after earnings. It looks like Mr Market is full of semiconductors.

We trimmed our semiconductor gains a few weeks ago and focused more on biotech, small cap, and even firms with high earnings yield. That latter factor - consisting of quality value stocks - is working.

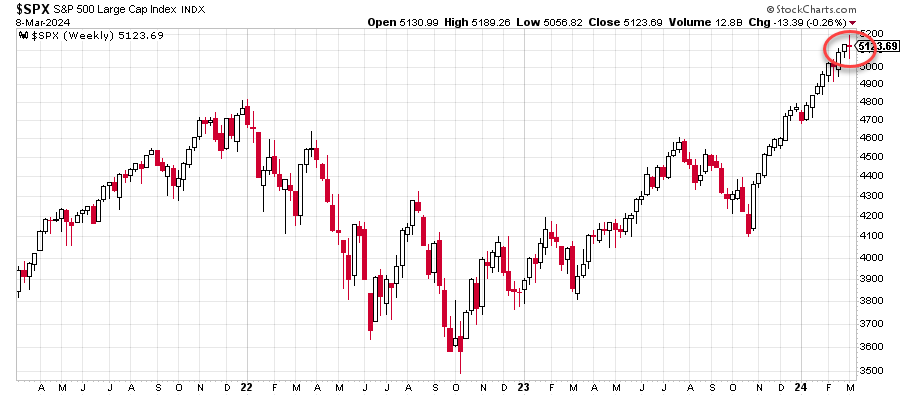

Per Ryan Detrick, we now have a weekly doji on the S&P 500.

“Dojis can be signs of indecision and can often mark turning points.

Not end of the world stuff, but be aware being bullish is getting quite crowded.”

They are paralyzed.

Here’s what’s holding them back:

1) Waiting for Vix to hit 35 and that did not happen in Oct ‘23

2) Waiting for Fed to cut rates

3) Fear of bubble

4) Waiting for a pullback

5) Arm chair macro

6) Outsourcing your thinking to whomever has the hot hand

7) Waiting for the correction

In wealth management you see a lot of pathologies.

The disposition to invest well is hard.

Most people are better off doing a tax loss harvested version of the S&P 500

Most people know this but will try to beat the market, and make these mistakes anyway

If you want to beat the market, it’s doable.

I shared many times don’t own Apple and Tesla and countless other themes and ideas.

But, the personal psychology is the most important. You can’t teach that.

People will self deceive themselves into making mistakes and would rather please their ego like the guy in the mirror meme.

For this reason, I do believe many, many people would benefit from professional wealth management - or the index approach

Investing well is hard.

If you saw the hours and focus we put into investing well, most people would say ‘Ahh… got it. Damn, that’s a lot of work. Yea, that’s not for me’

There’s a lot of minutiae. It’s not all big picture stuff.

It’s a thousand little things and a few big things.

A small fraction of people have the skill to invest well in public markets.

(That 1% does not include JP Morgan or Goldman Sachs or other committee led decision making)

For people that are intellectually curious and want to learn, get a wealth manager.

And then get a self-managed play account.

That way you can scratch that itch, but also do right by you and your family.

Don’t let ego or a pathology hold you back

Apple’s PE ratio is now 26x down from 32x last summer.

That’s some serious multiple compression.

One of my greatest fears as an investor is ‘growth to value transitions’.

If you own growth stocks, you need them to perform.

They need to post triple doubles each night (eg, revenue, earnings, margin growth).

If you look up ‘nifty 50’ or ‘growth to value’ you will see quite a few posts on this topic.

Note: Apple was up today in a red market

Did you cover your Apple short yesterday?

Yesterday: ‘Now is a good time to cover those Apple shorts.’

Meanwhile, look at Taiwan Semiconductor.

The PE is 23x up from 15x last summer!

Check out this tweet for the receipts.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Company Earnings

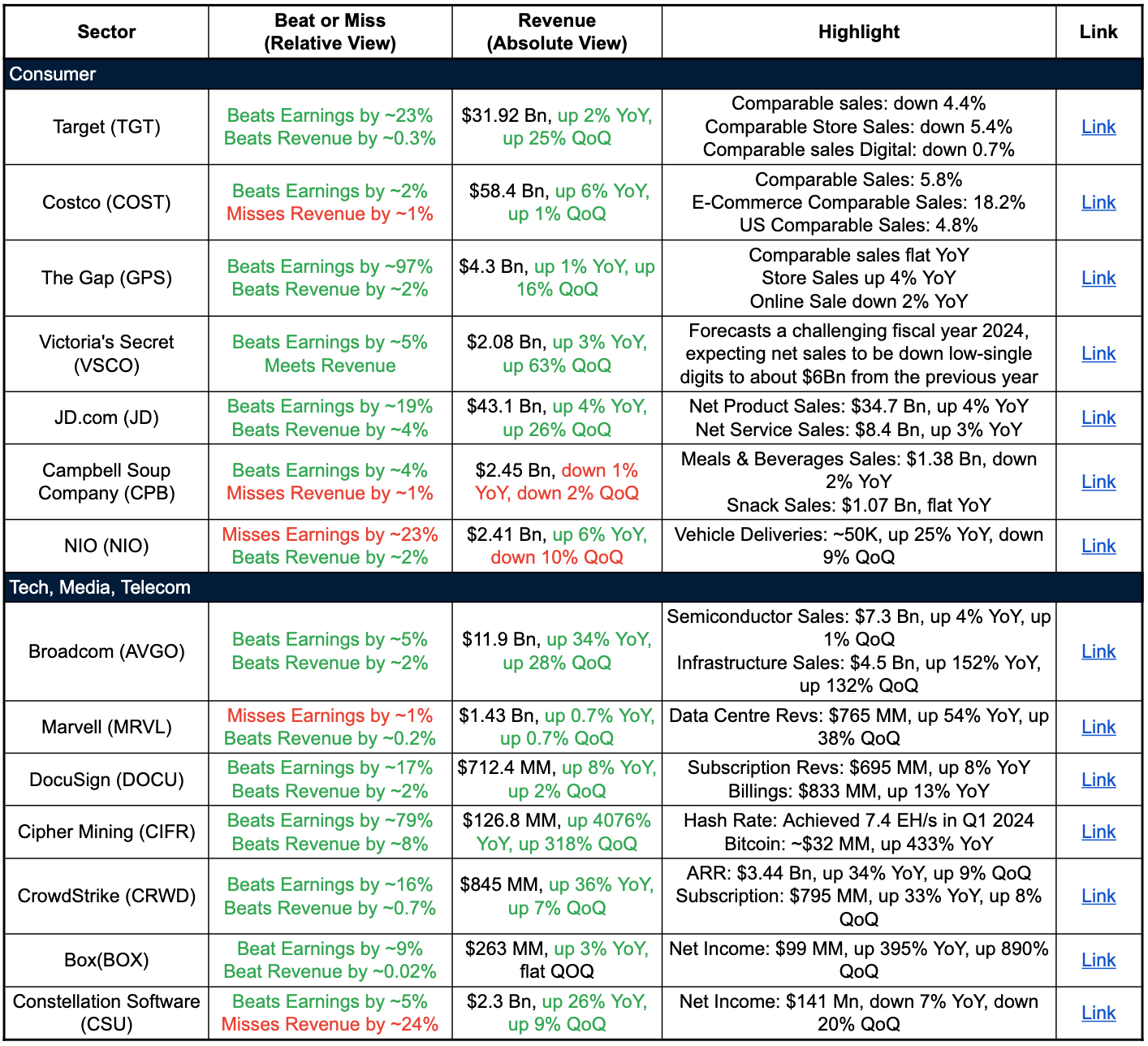

Here are the sector-by-sector trends and insights based on the earnings data provided:

Consumer:

Retailers are navigating a complex landscape of changing consumer preferences and economic uncertainties, amidst cautious consumer spending.

Big box retailers like Target and Costco are seeing modest sales growth, but traffic/comparable sales are down as consumer spending moderates

Apparel retailers like Gap benefit from solid in-store sales

Specialty retailers like Victoria's Secret forecast a tough year ahead as discretionary spending tightens

E-commerce players like JD.com in China delivering steady top-line growth driven by product and service revenue streams

Consumer packaged goods companies like Campbell Soup witness softer volumes across meals/beverages and snacking categories

Tech/Media/Telecom:

Software, semiconductor, and cybersecurity demonstrate significant growth.

Semiconductor companies like Broadcom and Marvell are getting a boost from data center/AI demand

Enterprise software vendors like DocuSign and Box seeing continued revenue growth Cybersecurity firm CrowdStrike maintaining robust ARR expansion driven by strong enterprise demand

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

On AI

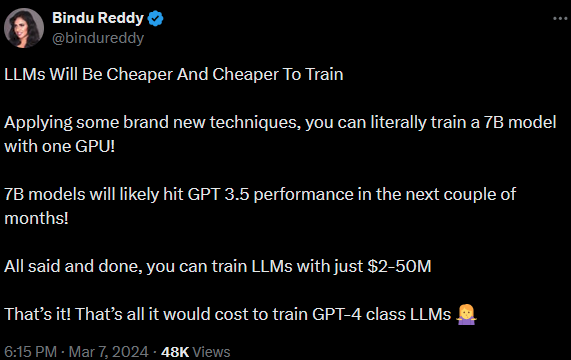

LLMs Will Be Cheaper And Cheaper To Train

We do believe investors who FOMO into foundational LLM models will find that these capex-intensive businesses are wildly overpriced.

Stay focused on the picks and shovels layer.

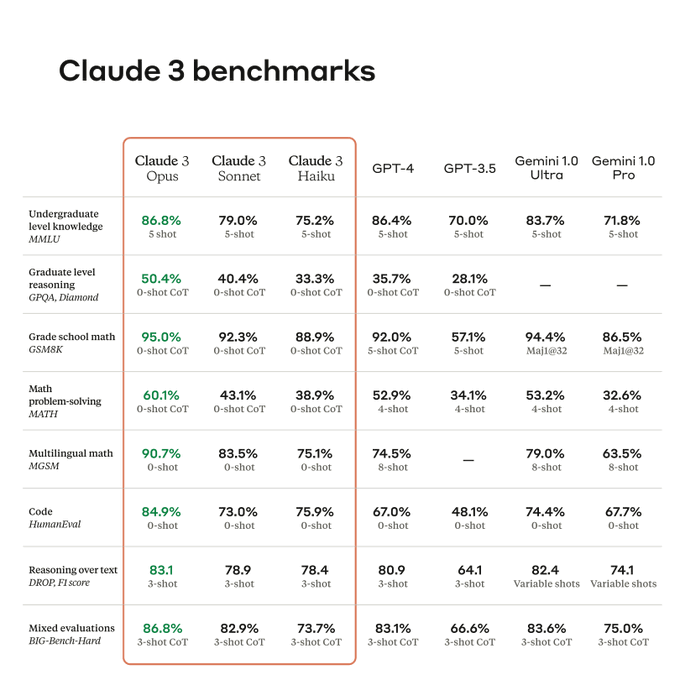

Check out Claude 3 and Perplexity. These LLMs are pulling ahead of Open AI in several respects.

Claude 3 set new industry benchmarks across reasoning, math, coding, multilingual understanding, and vision.

Will We See Uni-Founder Unicorns?

That’s the prediction from Sam Altman.

It’s already happened.

A few times.

1. Satoshi N.

2. Vitalik B.

3. Anatoly Y.

4. Sam A.

And many, many more.

More than TradFi imagines.

How to Build a Statistical Arbitrage Model Using Chat GPT3

I am trying to understand 'momentum exhaustion' (naturally after I put our kids to sleep :).

The opposite of momentum peaks is 'capitulation'.

We saw that in China last month.

Capitulation is much easier to see in hindsight.

Momentum is easy to measure.

And you can detect it waning.

But it's harder to know when it has ended versus taking a breather before renewed vigor (such as after Nvidia's earnings).

The “problem”, if you can call it that, is that psychology is dynamic.

Still, there were some promising results that could serve as guideposts.

Here are a few charts and initial findings with GPT

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Digital Assets

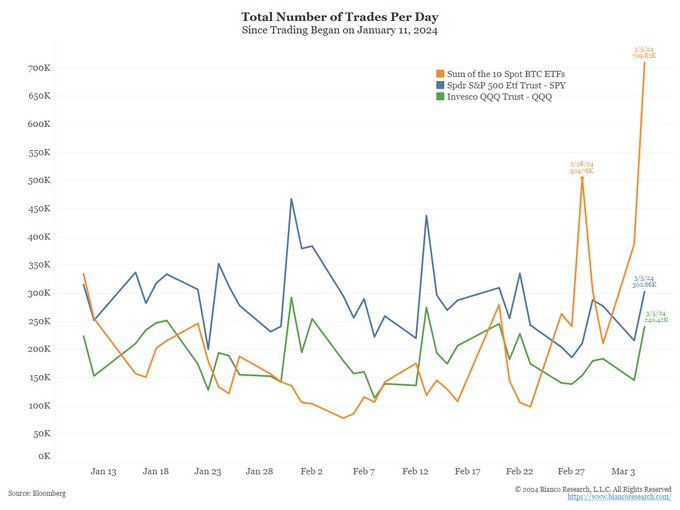

There is more demand for Bitcoin than Blockchain or Coinbase’s website can handle.

Per Jim Bianco, the 10 spot BTC ETFs traded 709,820 trades yesterday, March 5 (orange).

This is more trades than SPY (blue) and QQQ (green) combined.

This works out as 33 trades a second, more than the BTC blockchain can process.

Another major development this week was Arizona Senate considering adding spot Bitcoin ETFs to the states’ retirement portfolio.

If other states such as Florida and Texas follow, that’s a big deal symbolically.

Here’s a great thread from Bitwise’s Matt Hougan on Alt Season.

Lumida Wealth will be announcing a new crypto wealth management as a service this Monday.

It will include a:

(i) Yield strategy. Holders of stablecoin can earn double-digit yields (because the demand for leverage is high)

(ii) Growth strategy. These are tokens that we believe have ‘quality characteristics’ and may grow quickly. High risk, high reward.

(iii) Momentum Quality strategy. This is a high turnover strategy that seeks to identify tokens on the upswing.

We also have a hedge fund we invest with and are constantly looking at sub-advisors with novel strategies.

We’re excited. Stay tuned.

Michael Jordan on putting winning over feelings:

“I pulled people along when they didn't want to be pulled.

I challenged people when they didn't want to be challenged.

And I earned that right because my teammates who came after me didn't endure all the things that I endured.

Once you joined the team, you lived at a certain standard that I played the game, and I wasn't gonna take anything less.

Now if that meant I had to go in there and get in your ass a little bit, then I did that.

You ask all my teammates, "The one thing about Michael Jordan was he never asked me to do something that he didn't fucking do.”

When people see this, they're gonna say, "Well, he wasn't really a nice guy, he may have been a tyrant."

Well, that's you.

Because you never won anything.

I wanted to win, but I wanted them to win and be a part of that as well.

Look, I don't have to do this. I'm only doing it because it is who I am.

That's how I played the game.

That was my mentality.

If you don't wanna play that way, don't play that way.”

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Meme of the Week

Quote of the Week

“Whereas most technologies tend to automate workers on the periphery doing menial tasks, blockchains automate away the centre. Instead of putting the taxi driver out of a job, blockchain puts Uber out of a job and lets the taxi drivers work with the customer directly.” —Vitalik Buterin

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.