- Lumida Ledger

- Posts

- Fed Watch, Biotech's Rise, Mag 7 Positioning, Puerto Rico

Fed Watch, Biotech's Rise, Mag 7 Positioning, Puerto Rico

Justin Guilder & Ram Ahluwalia

January 28, 2024

Welcome back to the Lumida Ledger. Here’s a preview of what we cover this week:

Macro: Non-consensus macro, China capitulation watch, India

Markets: Technology stocks, PayPal, CRE opportunity, Software, SoFi, EV bubble disinflating

Company Earnings: Aviation, Chip Manufacturing highlights

Case Study: The Rolex Family Office

AI: Google Lumiere

Digital Assets: Crypto Equities vs. Spot Crypto

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Puerto Rico

This week, we had a fantastic time hosting an exclusive event for our clients at the beautiful Ritz in Dorado, Puerto Rico.

The Dorado area within Puerto Rico is turning into something really special.

It's quickly becoming the go-to place for ultra HNWI entrepreneurs, founders, hedge fund managers, retired execs.

Puerto Rico has zero capital gains tax and just 4% corporate tax.

Oh, and next week, Ram will be in Dubai meeting clients and prospects.

If you're around, and want to connect email us at [email protected]

Here’s a video with our on-the-ground impressions at the Ritz Residences in Puerto Rico.

These homes were valued at $5 MM a few years ago, and are now worth $20 MM.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Thoughts on the Market

There is a wall of money trying to find a home to invest.

Trillions of dollars were scared into money market funds in 2022.

But, where to invest?

Credit spreads have not been tighter since the GFC recovery

Cash yields don’t have much to offer after inflation.

Commodities are a good idea in certain spots (e.g., Uranium)…but China is on its back and the commodity bid is weak.

In alternatives, the best move is Distressed Commercial Real Estate which we have written about extensively. This remains our single best idea for tax-efficient, long-term wealth creation.

In liquid markets, the answer remains equities.

But, where to invest in equities? As we discussed, valuations for tech are near 99th-percentile.

Microsoft - the Consensus Bet for AI - has an outsized valuation.

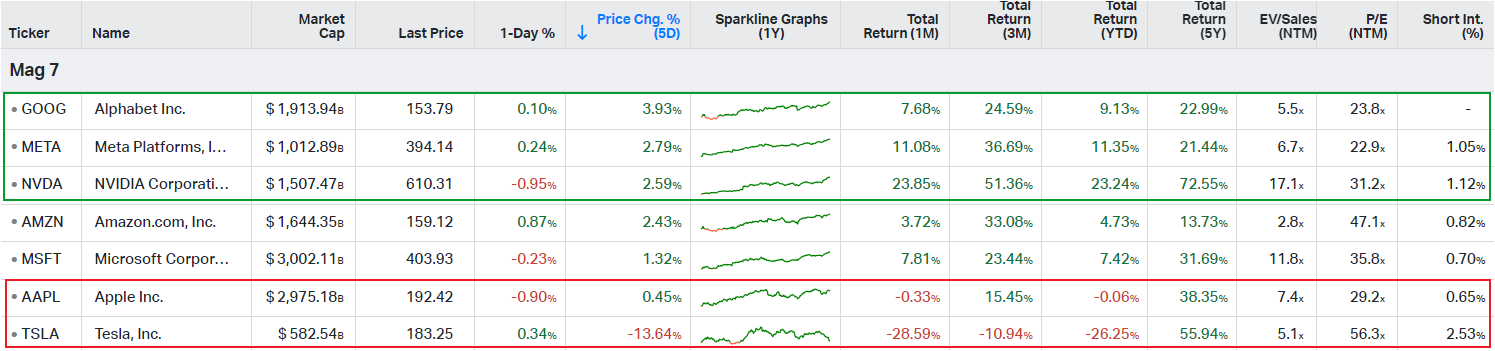

The best returners this YTD: Nvidia, Meta, and Google.

Our thesis is playing out. In Mag 7, those are our weights.

Microsoft posted a 7% return YTD - lagging our preferred names. Microsoft is priced for perfection. At best, you get a Consensus return. That’s what a 7% return is.

Meta and Google have scratches and dents. We like that. That causes the price to be less than fully valued. Scratches and dents can be fixed. And then you find the next opportunity.

The worst names? Apple and Tesla.

Simply matching the S&P or QQQ and not owning Apple and Tesla will allow you to beat the major indices. (Now, Tesla is due for a bounce after the shellacking… we mean in terms of long-term allocation).

So, where does the money go?

The primary driver of returns is multiple expansion followed by earnings growth.

The Mag 7 experienced multiple expansion last year. Now, the next leg needs to be carried by earnings growth. Some multiple expansion is possible from current levels - but the easy move has been made.

New money is going to focus on cheaper names in Mag 7 - those are our names.

Also, investors are frustrated that they missed out on Nvidia and will look to invest on the dips, and buy other semiconductors.

As you know, we’re already pre-positioned in semiconductors.

In fact, ASML, one of our New Year Stocking Stuffer stocks is up 14.64% YTD. And we made a public buy recommendation the second week of October - in the middle of a correction - to buy ASML and Broadcom.

We still like semiconductors on a ten-year secular thesis. That said, it’s quite bid up now, and we don’t like to chase.

Both Goldman Sachs and Altimeter are fanning the ‘AI is bigger than the internet’ meme idea. That’s taking root. And it should help our semiconductor positions benefit from multiple expansion.

Where else will capital flow?

Small caps and biotech.

Thus far, most of the exposures managers have taken to small caps are thru index and macro products (e.g., futures). There’s still a scramble to find the best ideas within small caps.

We have names we like there and are continuing to find more.

The small cap story is getting even better… High yield spreads have not been this tight since the 2008 crisis.

Small caps, on average (but not all of them, have large debt burdens on interest rate expenses. The prospect of a Fed cut and the ability to refinance is a gift from Mr. Market.

There is a significant corporate debt maturity wall in 2025. CFOs of small and mid caps should be calling their bankers and seeking to refinance now.

That should reduce the risk of these firms having a hiccup - and certainly reduce the risk of a credit event that never materialized and we called out as non-sense – again back in October when folks were panicking..

(Incidentally, that post received 150K views - hopefully it helped folks avoid selling the bottom.)

The other area we like? Biotech.

GLP1 have shown the world the power of biotech.

And the Biotech sector, up until November, had plentiful assets trading below net cash assets.

Valuations were at multi-year lows.

Big Pharma is going to see a significant expiration of their IP in the back half of this decade. They need to acquire biotech to maintain their portfolio of drugs.

We’re also seeing for the first time, the promise of new drug discovery. GLPs are one example of that. MRNA is another. Therapeutics is another.

Biotech today however is highly overbought.

For most of the biotech sector’s history, the primary ‘modality’ was molecules - think Lipitor, Viagra, etc.

These new modalities are unlocking new pathways for addressing issues. There’s also a broadening out of research from cardiovascular and cancer to cognitive disease such as Alzheimers.

These results are not yet in the public consciousness. The GLP success will cause people to recognize that biotechnology is finally delivering on the promise that Craig Venter offered when he decoded the human genome back in 2000.

So… we like Biotech very much.

The fast growing demographic segment is the oldest of the oldest. The highest spend category in healthcare is end of life care.

Is that not an extraordinarily beautiful setup for Biotech?

What names do we like? We have a list of 20. I started investing in Biotech hedge funds back in 2011. We are not in-house biotech experts. But, we have a first-rate network and host regular idea exchanges to vector in on what we believe are the best opportunities.

These names have smaller market caps so we’re reluctant to leak our ideas here and have them bid up while we continue to deploy new money.

What we just shared is the strategic backdrop. There are other sectors we like as well - but that should help.

Tactically, we had an extraordinary week of successfully front-running the investment banks both on the long side and our tactical hedging short side.

The ideas we shared on Twitter were successful.

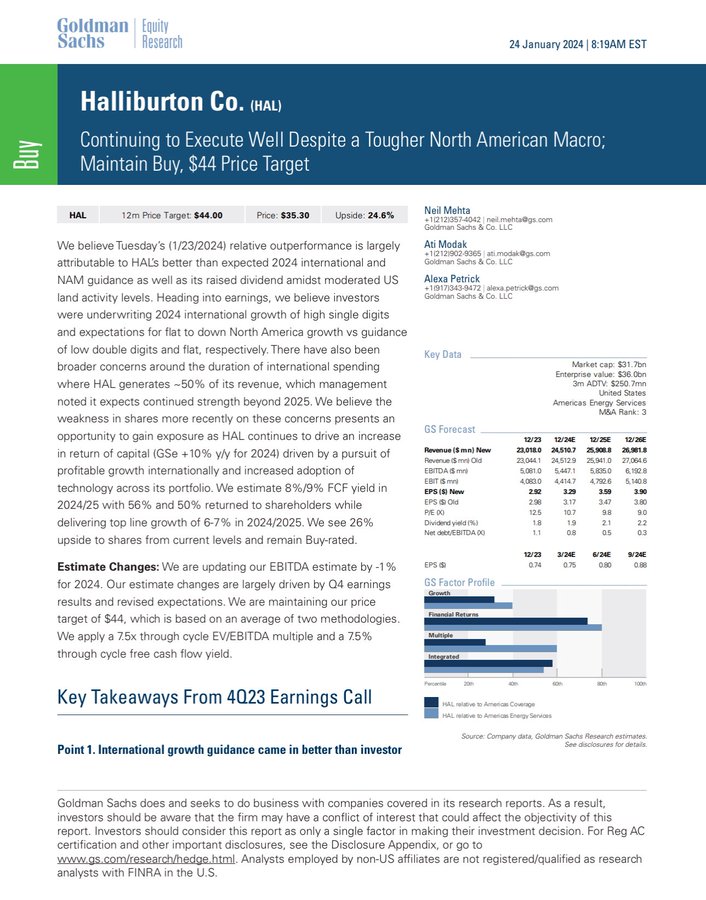

We allocated to Haliburton and Goldman Sachs came out with a buy rating earlier this week - a week after we purchased - lifting our positions higher.

We also identified Tesla as a stock to short. Morgan Stanley lowered its ridiculous price target. Recall we wrote about the ‘Disinflation of the EV Bubble’ and have been tracing the price cuts impacts from Tesla - and its competitors: Lucid and Rivian and a host of others.

Elon Musk is now calling for trade protection against China. We don’t like this sector at all - the competition is intensifying, and China is producing high-quality luxury and commodity care. Mercedes and BMW are getting in the mix also.

The Tesla earnings call was a disaster. The ‘FSD’ feature has no demand from other automakers. That’s not a surprise - you can get the technology from China.

Tesla was a big hype stock wrapped with hero worship and we’re proud that we saw through it and avoided any exposure. Elon Musk has made major contributions to humanity at the 99.9999% level - but Tesla is simply not a good investment when the forward PE is 70x - despite the mauling in the stock market.

Tactically, Mr. Market started the week neutral. It’s getting close to overbought - so our tactical hedging should do well this coming week.

Over the past week, we wrote about how we had shorted ARM to protect gains on our semiconductor portfolio. You can read about our rationale here. We covered those gains and that was successful.

We also covered our short in SoFi. We started shorting at the $9.60 level then again at the $8.50 level. And we wrote about it publicly.

Now SoFi is at $7.57. Making money with these quick tactical ideas creates value and controls our exposure. We need to make money on a relative value basis. But when the shorts produce profits as well - we’re in heaven. And we seek to do that if we can.

We should note the indices were up 6 days in a row (up until Friday), and these shorts tanked despite that. That is the definition of alpha.

We have zero trust in SoFi management to report clean earnings. So, we covered our shorts there. I noted in November that if SoFi were to get to $10, that would be a gift.

That remains true today.

One day SoFi will report earnings and it won’t end well. It’s hard to predict exactly which quarter - but sometime this year. This post explains why SoFi is a walking write-down.

Here is a thread that expands at a high-level on our technique and approach if you want to learn more.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

One of the Lumida Wealth stocking stuffer stocks, ASML, reported this week.

It's up 19% in the last week, and 40% over 3 months.

Here’s the link to the post for the timestamp.

The green line on the chart is when we made our buy call.

There are so many better businesses in the world than the optics game SoFi is playing.

Is ASML worth buying now? It's really expensive now.

As I say often, 'you make your money on the buy'.

You have to wait for Mr. Market to offer you a good hand and be patient.

And when the opportunities present you need to act.

Most of the time there is nothing to do.

Deconstructing Legacies: Rolex

We are launching new content streams soon, here’s a sneak peek from Lumida Legacy, where Justin will deconstruct legacies of some of the best brands, founder and businesses. We will curate the learnings and add expert insights on tax, estate & generational planning.

Don’t forget to Like, follow and comment your opinions.

And consider subscribing our Lumida Legacy newsletter for deeper dives.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Macro

Non-Consensus Macro:

March rate cut probabilities were 88% one month ago and now stand at 52%

The day of the FOMC we wrote that the public is hallucinating rate cuts. The same phenomenon occurred last year.

Receipts below.

You know from our prior newsletter we went out on the limb with this call.

If you understand Non-Consensus investing you will see we weren’t going out on a limb at all.

If you have an 88% chance of a rate cut 3 months from now, that means Consensus has plenty of time to alter narratives based on incoming data.

Now we have a 3%+ GDP print…all time high stock prices.

Mr. Market was sloppy at the December FOMC meeting. We recognized that, called him an Uber, and charged him a hefty fee for the service.

If you look at the stocks of Loan Depot, Rocket Mortgage, and Better – mortgage originators – you can see equities have mostly discounted the kicking out of rate cuts.

At this Wednesday’s FOMC meeting, we would expect to see the FOMC solidify expectations for the market.

There are two scenarios:

1) The Fed signals they will cut in March. If that happens, we get a melt-up in equities circa 1999. The downside is melt-ups are followed by melt-downs.

This could cause an air pocket or hiccup for rate sensitive equities - including biotech, small caps, and financials.

2) The Fed clarifies they do not intend to cut in March. If that happens, then rate sensitive sectors and recent ebullience gives back

If there is an air pocket, you want to have your buylist ready in case there are bargains to be had.

The main risk to our bull thesis is a (i) Fed kicking the can down the road ‘March rate cut idea’ - it’s a fly in the ointment along with (ii) bullish sentiment that needs to get worked off over the next few weeks.

Overall, markets are ahead of themselves.

We expect we’ll finish the year strong, but need to get past these two issues in Q1.

Demographics Are Destiny: India Edition

India’s population surpassed China’s last year.

India’s population is growing. China's economy is shrinking.

Is it a surprise that the best performing stock markets globally have the best demographics?

India, Mexico and the United States.

The worst: China and Europe.

(Japan, the outlier, is a corporate reform story)

India and Mexico are also benefiting from ‘friend shoring’

What about Brazil?

My view is Non-Consensus:

Brazil deserves the overweight.

India is a great story, but you need to search for value (such as the banking sector).

The index is too expensive.

India (too expensive). See charts below.

We have an overweight stance on Brazil.

The Economy is nearly as good as it gets

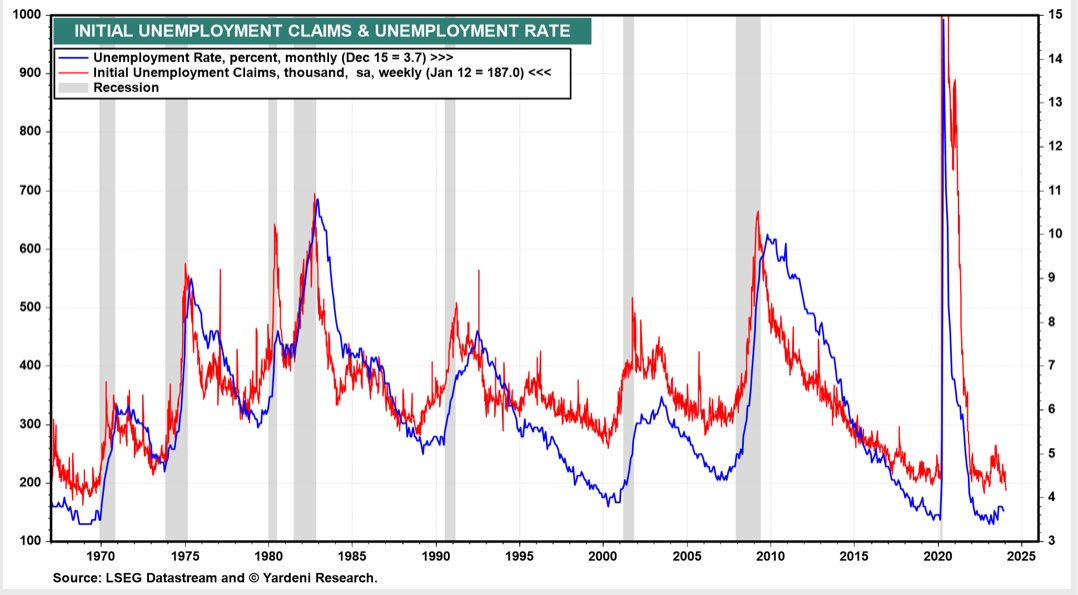

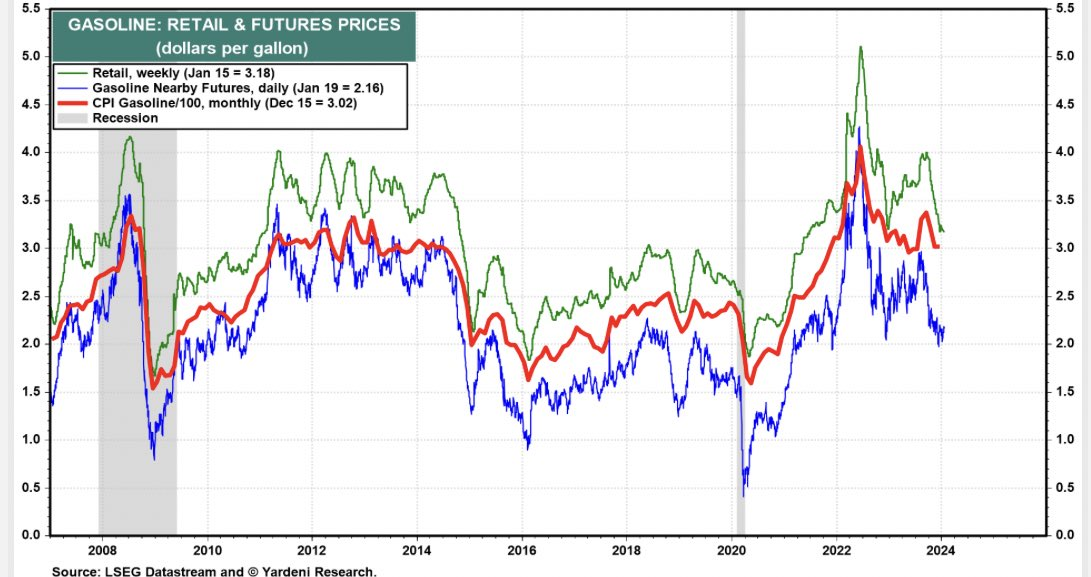

Unemployment, inflation, and gas prices are down.

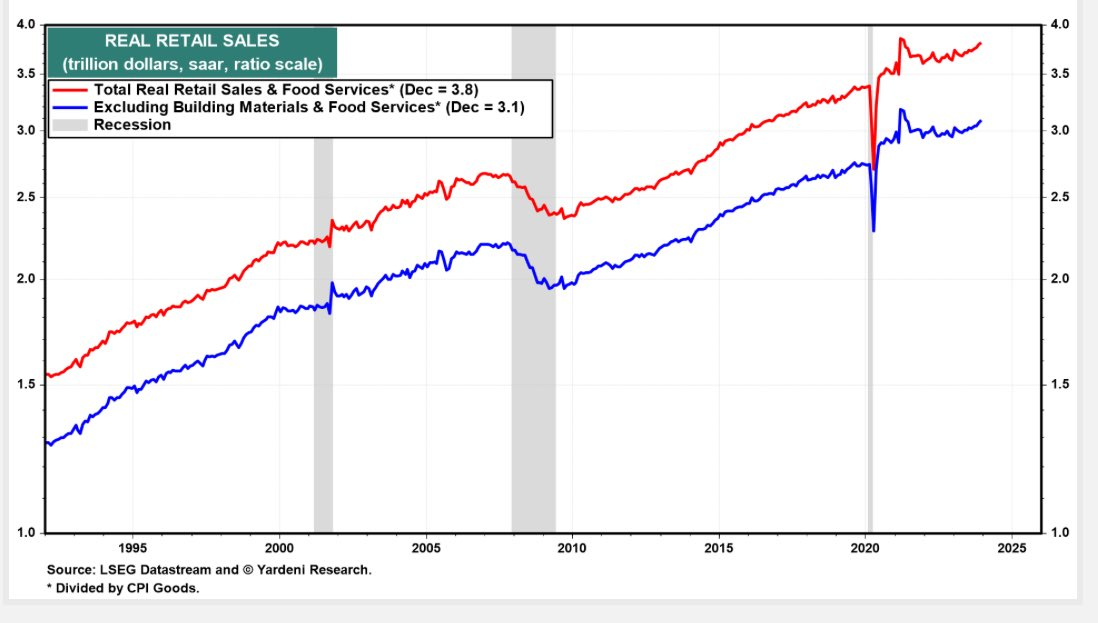

Retail sales are up.

Consumer sentiment is up.

We’re also in an election year. Congress usually behaves by doing nothing.

You see this reflected in credit spreads, as we noted above.

The bull market is ensuring there is a ‘wall of worry’.

A wall of worry keeps cash on the sidelines to provide fuel for a bull market.

At the beginning of January, markets corrected because there was no wall of worry.

The New York Empire Index results reinvigorated fear. We saw put/call ratios (the demand for insurance) spike.

That headline re-built the wall of worry, and markets rallied back to all time highs.

We are getting close to perfection again - and we’ll be keeping an eye on the market’s reaction to the Wed FOMC meeting as well as upcoming earnings reports from Apple and Amazon to see if Mr. Market gets sloppy and creates opportunities.

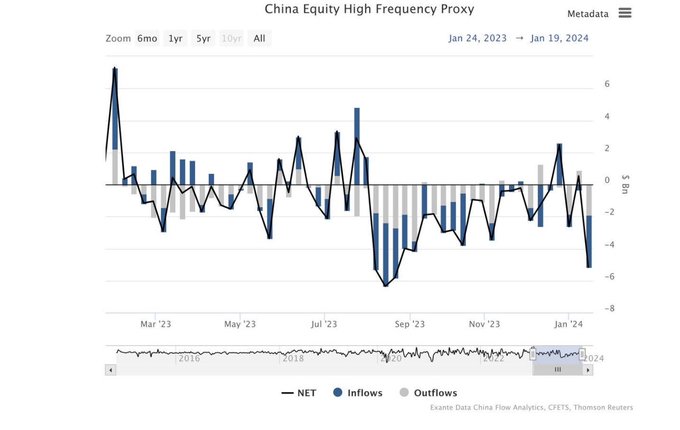

China capitulation watch

A large China focused hedge fund shuttered its doors.

Forced liquidations are a sign that we are getting close to capitulation.

Also, I saw a Chinese Ramen Noodle maker stock get crushed.

That’s starting to look like indiscriminate selling.

BUT, Chinese equities are now at a level where certain structured products issued by banks may go under-water.

That could trigger further losses for the bank issuers or millions of retail investors.

That could cause a new round of downside volatility.

It’s similar to the banking system getting a margin call.

The government is now exploring a bail out.

If I were to map this to 2008, it’s similar to September when TARP and short sale bans were introduced.

US markets bottomed in 2008 the same month Buffett started buying banks.

Markets rallied for a few months then hit new lows and found an enduring bottom in March 2009.

That was after regulators suspended mark to market accounting which was wreaking havoc on bank balance sheets (not unlike the structured products issues in China), and everyone stopped trying to catch the bottom.

We have the NH primary today.

A Trump win should hurt Chinese equities.

This is the point in China where it is darkest before it gets more dark.

Capitulation watch continues.

China now sells at the cheapest valuation EVER relative to global equities.

That’s a 50% discount to global equities.

MSCI China Index is at an all time low

Source: Richard Bernstein Advisors

We did buy an insurance company at a 4.5 PE ratio. I had met the management personally in China several years ago.

So far, it’s up. But, there is no clear evidence that we have a capitulation.

We might not also get a capitulation, so a mixed strategy of picking up quality assets when they are cheap is a reasonable approach.

Be selective, be patient, and stick to the highest quality assets.

There are so many people trying to catch the bottom, that behavior paradoxically prolongs the bottoming process.

Bottoms happen when nearly everyone gives up in despair and goes home.

Trump’s political ascension should hurt China equities.

The day China’s stocks don’t get hurt as Trump’s poll numbers improve is a sign that risks to China are priced in.

Keep this fact with you: China has issues, but they are not nearly as severe as the 2008 crisis.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Markets

Market Compass

Let’s cycle through our three-prong market compass as we look to the week ahead.

1. The 10 year bond yield remained flat over the week at 4.14%, up 32 bps YTD.

When the Ten-Year increases, that hurts valuations for long duration stocks.

The 10-year is thus far behaving.

2. The US Dollar is turning up (Up by 1.63% MTD)

When the USD increases in values, US equities decrease in value.

The US dollar is at a crossroads. If it breaks that resistance level, we’re in risk-off.

The US dollar is waiting for the FOMC news on Wed and in a holding pattern.

3. Semiconductors are up.

Semiconductors are an expression of AI narrative.

The SMH ETF moved up by ~2% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average.

We don’t believe now is the time to chase semiconductors.

AMD is up ~29% MTD. We believe AMD is overbought at these levels.

We shorted ARM this week at $78 to protect gains in our semi portfolio, and we successfully covered at $71.

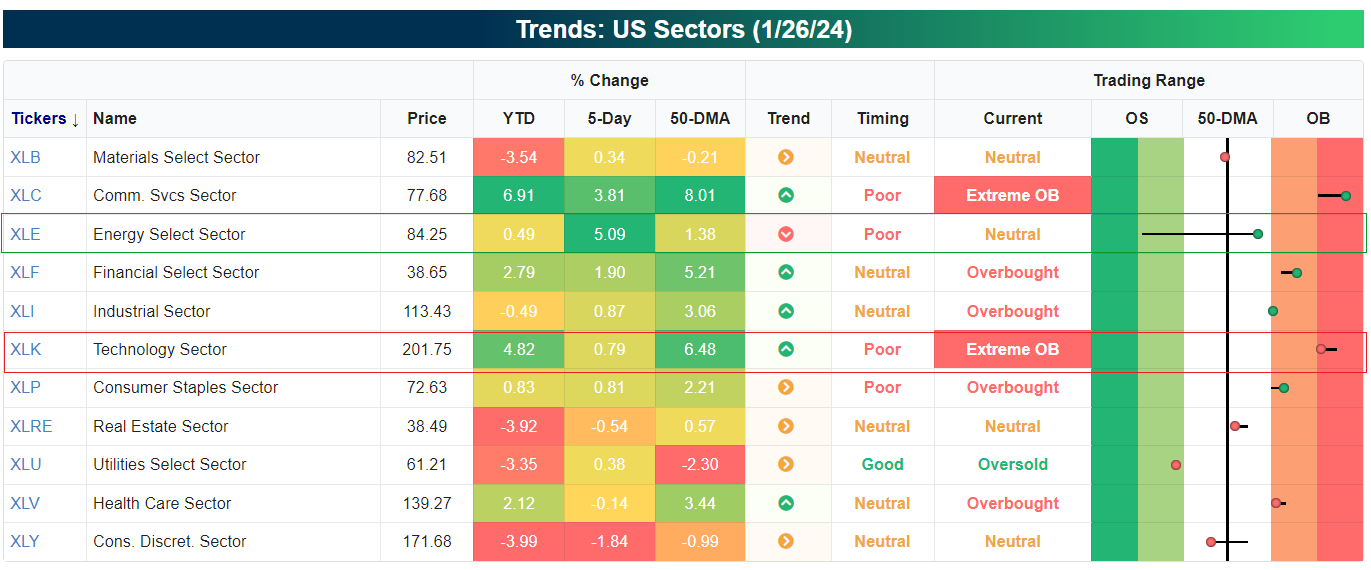

4. US Sector Trends

Energy is up ~5% since last week. Energy prices remain low despite heightened geopolitical risk.

Part of that is the idea that the US is energy independent and producing ample energy for itself and the world.

I can’t stress enough how impressive the US’s global position is - from (less worse) demographics, earnings growth, the quality of American management, and entrepreneurship, technology leadership, military dominance - and much more…

The technology sector is overbought.

Don’t chase folks. Buy the sector when it is oversold, and focus on the names with the best relative strength.

Hint: Not Apple.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

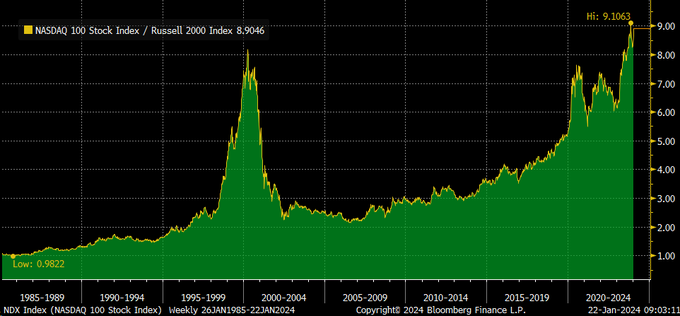

The Nasdaq 100 to Russell 2000 Ratio Unveiled

In the dawn of 2020, the Nasdaq 100 to Russell 2000 ratio stood at 5.1x.

Fast forward to today, and it’s at an astounding 8.9x.

This ratio measures how the large-cap tech stocks that dominate the Nasdaq 100 are priced relative to the small-cap stocks of the Russell 2000.

When the ratio rises, it indicates that investors are valuing large-cap tech stocks more highly relative to small caps.

Currently, this ratio is almost double the historic average, signaling that we’re in an unusual market phase.

The widening gap between the valuation of large-cap tech stocks and small-cap stocks cannot persist indefinitely.

Mr. Market tends to seek equilibrium.

Can this ratio increase? Yes. In fact, that’s what is happening this year as Mag 7 names generate earnings growth.

Here’s why.

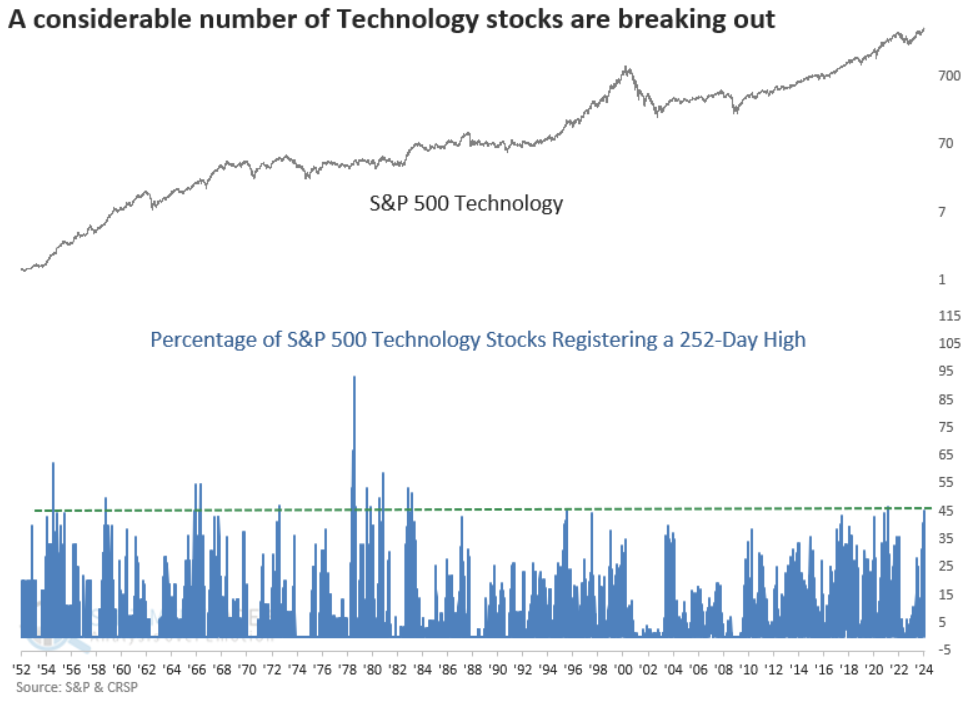

Market Study: Technology stocks

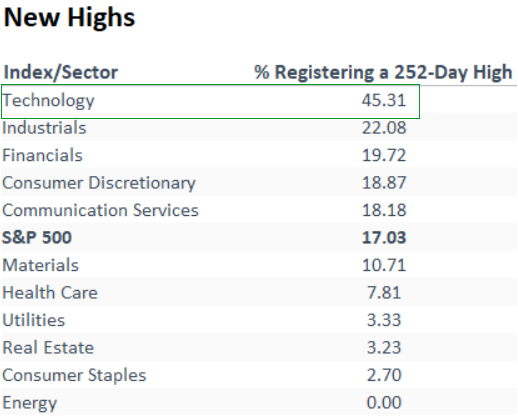

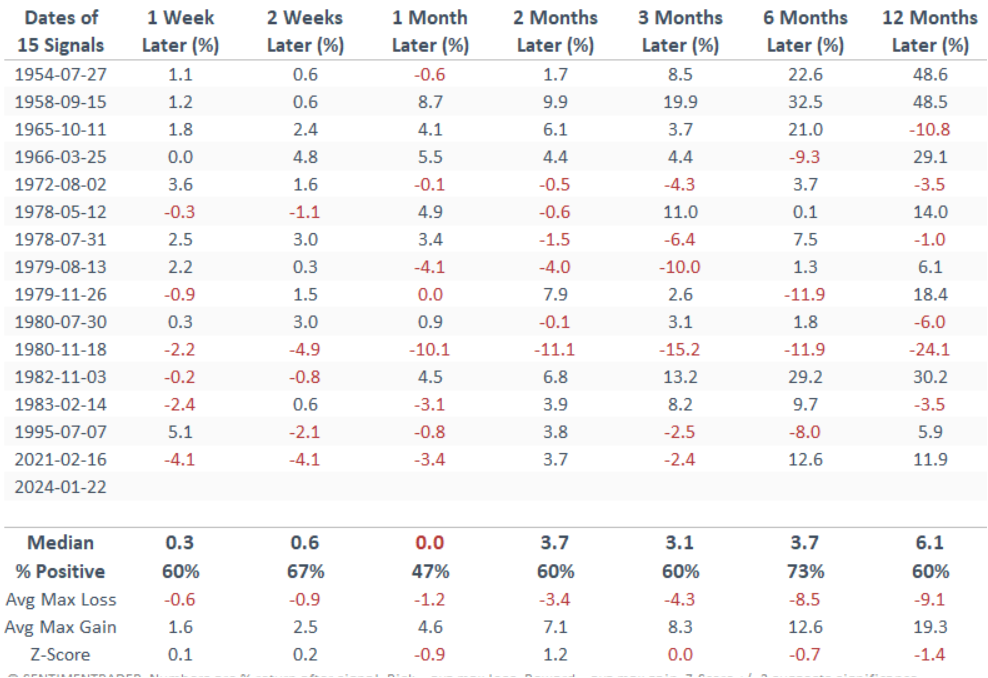

The percentage of S&P 500 Technology stocks registering a 252-day high exceeded 45%.

Technology and other cyclical sectors dominate the list of annual highs.

This is a common feature of bull market environments.

Historically, when the percentage of S&P 500 Technology stocks hitting a 252-day high surpasses 45%, the sector tends to experience additional upward momentum in the subsequent weeks.

However, this momentum fades a month later, resulting in a flat return and a marginally lower coin toss win rate.

The medium to long term returns remain positive.

This is consistent with our ‘expect Q1 weakness’ thesis - that we have sentiment and OB conditions to work out, but after that we’re off to the races.

Keep this study in the back of your mind as we navigate the next few weeks.

February may have turbulence, then bullish seasonality comes back around March and April.

Classic buy the rumor, sell the news - PayPal (PYPL)

On January 17th, PayPal's CEO said he was going to "shock the world" on January 25th.

Just now, PayPal released new AI features and a way to earn cash back through the PayPal app.

The stock just dropped nearly 5% in a matter of minutes.

It is also down nearly 15% from its high after the CEO said he was going to shock the world.

It seems like the world was indeed shocked, but to the downside.

Keep this in mind the next time you see new product hype from a company such as the Vision Pro or an over-enthusiastic reception to earnings.

Incidentally, we are warming up to PayPal.

What’s our view on PayPal?

Now that it dropped, we like it!

PayPal has a good story. It sports an 11.5% forward PE, 7% earnings growth, and new product initiatives focused on improving the customer experience.

PayPal also has a new stablecoin product.

PayPal has made the ‘growth to value’ transition. We believe the bottom is in for PayPal and it has a home in our model portfolio - only after this recent correction.

Goldman Sachs reiterated their Neutral rating on Tesla

Neutral is code for GTFO.

GS lowered their price target. (That’s like calling the firemen after the house burns down)

Tesla, and EVs more generally, are capex guzzlers in a high rate world with intensifying

Competition.

Our followers here and on X or Linked In know we have been bearish on Tesla for months.

Both Tesla and Morgan Stanley completely whiffed the ball.

And both are chasing Lumida on our long Haliburton and Cloudflare calls.

Did we mention? We bought Cloudflare (NET) last week thursday. Morgan Stanley upgraded the stock a week later after NET was up 10%.

These banks have committees and need to generate pretty reports. The committees make it harder for them to think in a non-consensus way.

Plus, no one wants to call a short on a technology company that needs investment banking services.

As Warren Buffett says, ‘be skeptical of what Wall Street sells’.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Alternatives: Distressed CRE

Our highest conviction opportunity remains Distressed Commercial Real Estate.

14% of all commercial real estate (CRE) loans and 44% of office building loans are now in "negative equity."

In other words, the debt is now greater than the property value on all of these properties.

Currently, US banks hold over $2.9 trillion of CRE debt, the majority of which is held by regional banks.

Office building prices are down 40% from their highs and CRE as a whole is down over 20%.

All as rates rise and many of these loans are due to be refinanced.

CRE is beyond bear market territory.

The hard part of the thesis is manager selection.

We expect a 3 to 5x MOIC before tax benefits.

The S&P can’t do that over the same time frame.

We are having success in our nuanced approach to public equities…But we are cognizant the best opportunity remains in the alternatives space.

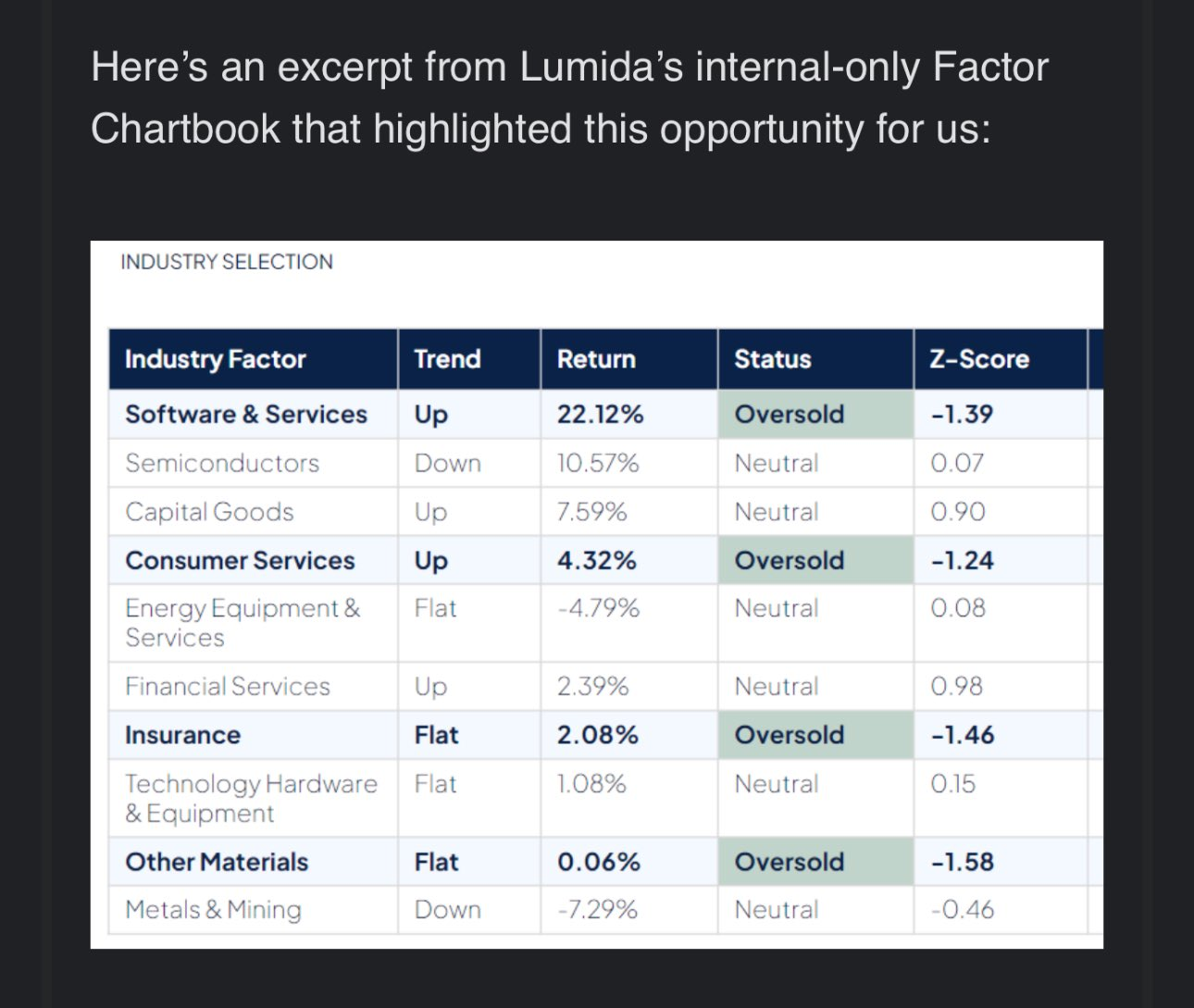

Software sector is still eating the world.

Last week, the move to make was to buy software.

Software firms like Cloudflare and MongoDB were oversold.

See this chart for our internal research factor book:

So we bought them on Thursday, after Mr. Market got overly depressed on Wednesday according to various measures.

Dealing with Mr. Market is like playing the game of ‘slaps’ as a kid — you have to recognize opportunities and move quickly.

That means having your homework done in advance.

Take a look at this positioning study from Goldman on Software & Semis.

We remain overweight in both these categories.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Weekend Reflection on 2023

I had an 'aha' moment that's causing me to adjust a few mental models.

Headline: 2023 would have played out very differently without the BTFP.

The conventional wisdom is that 2023 was a banner year because (i) recession was priced in and (ii) the US economy was stronger than anticipated.

(i) is partially true. Indeed, hedge funds did have 99th-percentile short positions.

And the recession was widely telegraphed and measurable in CEO surveys.

But, the peak-to-trough market declines you see in a bear market with recession (e.g., 2000 and 2008) never materialized.

It was a soft bear market, and relatively quick (9 months).

The big difference between deep bear markets and garden variety bear markets (like 2022) is whether you have job losses from recession.

Did the yield curve break anything?

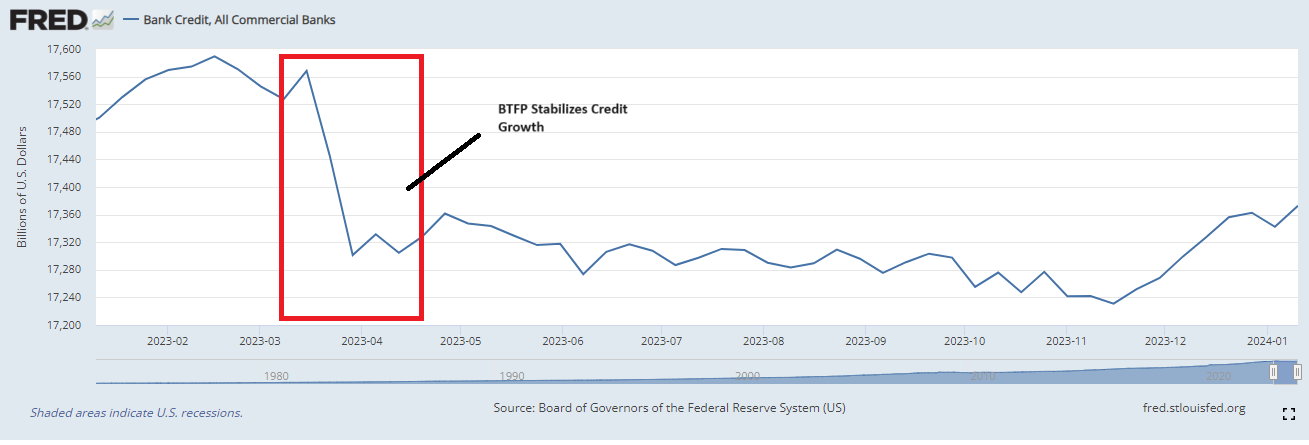

Yes. The inversion of the yield curve did break the banking sector - and the CRE loan complex.

Here's the crucial point:

(1) Bank credit growth fell to 0% during the crisis.

This was the pivotal moment.

The Fed's Bank Term Funding Program rescued the banks.... and that intervention stabilized credit growth.

(2) Credit growth is a major driver of the business cycle.

Recessions can be caused by contractions in credit growth.

Show me credit contracting and I'll show you a recession.

So, the story is more than merely Expectations.

If the BTFP program was not created, credit growth would have gone negative.

Banks would have gone into a crouch position, along with Consumer sentiment.

What's the point?

The Consensus would have been right - had there been no BTFP.

And equity markets would have dropped lower, as the '22 losses were still below what you would see in a bear market accompanied by a recession.

All the macro and positioning reasoning in the world going into '23 pales into comparison to the single policy intervention of the BTFP program.

It should also give us a lot of humility in our mental models of the world.

A single discrete intervention on a certain date can change the timeline..

The world is not a deterministic path of outcomes where we measure 'did we get it right' or 'did we get it wrong'.

It is highly probabilistic with different outcomes and possibilities.

But for the policy intervention, I now believe the Consensus would have been correct in '23...

I did not have that view yesterday.

Here are a few charts that show credit growth during that pivotal time frame, and credit growth today.

This chart shows the timeliness of the BTFP intervention. Without the intervention, credit growth would likely have contracted causing a recession.

On SoFi: The FT weighs in on SoFi's opaque accounting practices

"The dark art of bank fair-value accounting needs more transparency, SoFi's Choice"

Excerpts:

"It can be argued that some of the assumptions SoFi is using are aggressive, especially relative to the few other lenders using this method."

I would say so... Look at how SoFi increased the value of their loan book in Q3 while credit spreads widened during the quarter.

At the very least, banks should be required to report the difference between CECL and fair value treatment in their financial and regulatory reports, so the differences are clear to the markets and regulators.

Absolutely. You can't allow banks to game the system.

“Only six US banks had non-mortgage consumer loans (personal, student, etc), measured at fair value, with SoFi’s loans making up more than 95% of the total”.

“And only SOFI’s loans were booked at a large premium to their unpaid balance, resulting in higher loan revenue."

According to Bologna, if SoFi had elected to account for loans at amortized cost and had to take CECL reserves similar to peers, its tangible book value per share reported for the third quarter of 2023 would fall from $3.42 to $2.00 and its CET1 ratio would be cut from 14.3 per cent to 8.9 per cent.

SoFi needs to raise more capital and slow origination growth. If they do that OR if delinquencies increase (take a look at Discover...), then SoFi's earnings will take a major hit.

EV sector is a bubble that blew up and is deflating now

Earlier this month, we shared our thesis that the EV sector is a bubble that "blew up and is deflating now".

Since then, take a look at the charts of Nio, Rivian, Tesla, and Lucid.

Some of those names dropped 50% since then.

What was the tell?

On Semiconductor missed earnings last quarter.

On is a major EV component supplier to these firms.

By the way, we bought After it went on sale.

EVs are a secular trend.

However, at the retail level, EV firms are locked into a death match consisting of intense competition and high rates.

We prefer owning the picks and shovels play.

It's very similar to our view on AI. Why own the Application Layer - a capex heavy 'winner take most' death match?

Own the Cap Ex receiver layer.

There are mini-bubbles inflating and deflating all around us.

How to beat S&P and QQQ? Avoid Apple and Tesla.

Nvidia is up 23% YTD (over 19 sessions).

The Nasdaq? Up only 2.9%.

This market requires a highly nuanced approach…

Simple way to beat QQQ and SPY?

Don’t own Tesla and Apple :)

Now, Apple I expect will continue to rally along with QQQ. But its upside and relative strength is capped. It will lag.

Apple is already down 3 days in a row during a period where QQQ was up. This happened in December as well and it previewed the Jan 2nd mini-correction.

Tesla I am surprised it has not bounced yet.

Goldman Sachs issued a BUY on Halliburton

We bought Haliburton Thursday January 18th. Here are the receipts on the call:

We wrote about it on X and here in the Lumida Ledger newsletter.

Take a look at Halliburton - up 10.3% over the week.

This was the most satisfying entry all year.

Now, Mr. Market is noting what we saw in this world class energy business.

Same pattern with MS following our call to buy Cloudflare.

Or GS coming to our view on rate cuts.

These big banks are all late. We remain one step ahead and love it when they buy into our wake.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

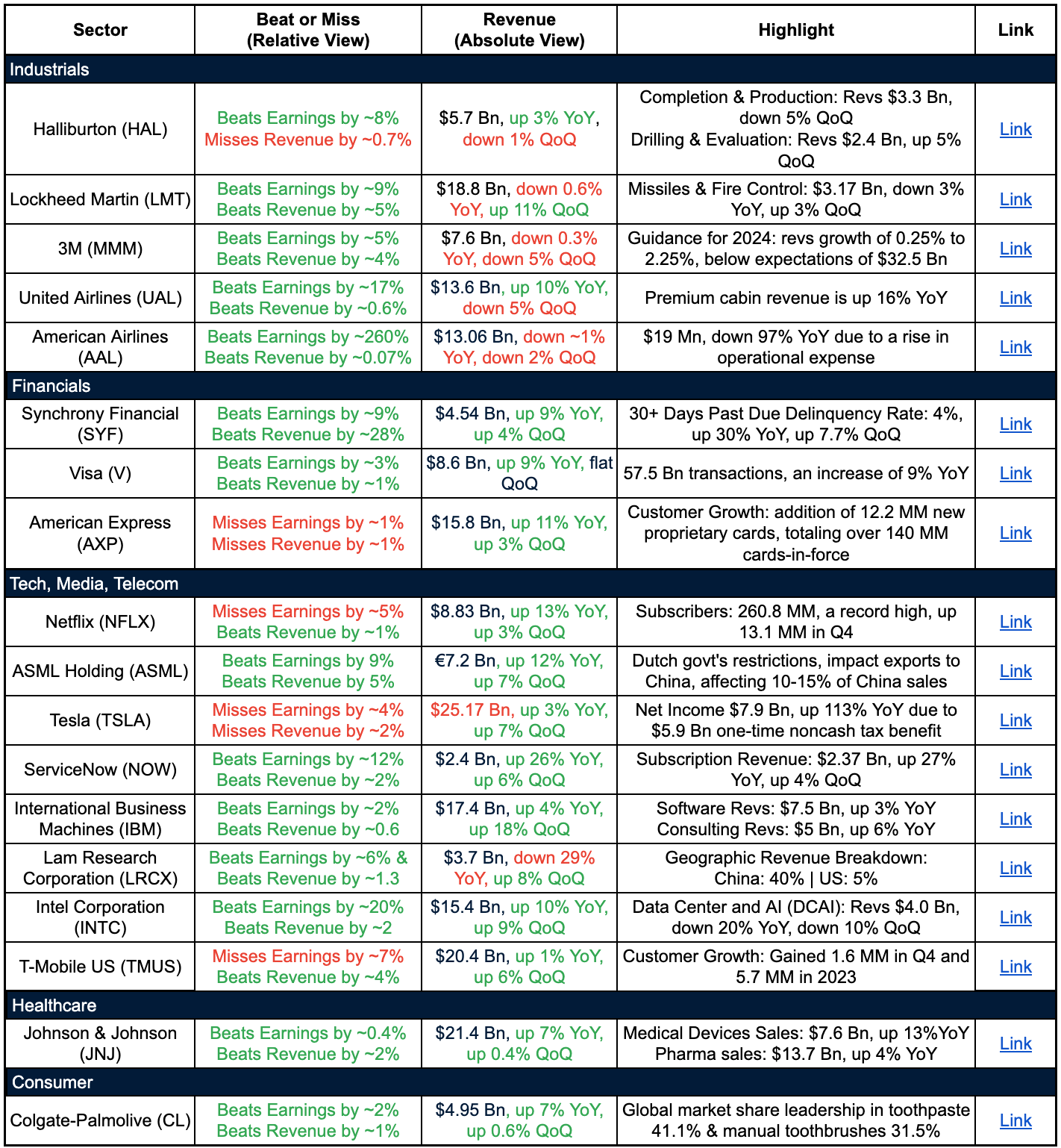

Company Earnings

Aviation - Travel

Companies Reported: UAL, AAL

Trend:

Reported strong earnings, however, revenue was down QoQ, (suggests a slight decrease in demand for air travel)

American Airlines, achieved its best-ever Q4 and full-year completion factor, with the lowest number of cancellations

Chip manufacturing

Companies Reported: INTC, ASML, LAM

Trend:

All companies beat estimates on earnings and revenues

Revenue is up QoQ across all three companies, with only LAM being down YoY

Link to Full Chart

AI

Google introduced Lumiere this week - its own text to video generator.

However there’s one key difference: it does not build the video frame by frame, rather it conceptualizes the entire video at start.

This model is a step towards building contextual AI LLMs. The model claims to blow the competition out of the water in terms of benchmark performance.

Check out the full thread here with our video cuts.

To dive deeper into the hardware and software wars in the battle for AI leadership don’t forget to tune in to our podcast with Jonathan Ross, Ex-Googler, builder of TPU and now founder at Groq.

Digital Assets

I spoke with one of the largest bitcoin holders out there in Puerto Rico. The mood was somber.

I asked him what he thought about the Bitcoin market - answer: “bullish selling”.

I never heard of bullish selling, but there you have it.

The best thematic move here is long spot crypto (via discount to NAV products) and short crypto equities (such as miners or MSTR) that trade at a premium to NAV.

This takes a lot of sophistication so leave it to a professional.

The vibe in crypto resembles May 2021 one month after the peak hype of the Coinbase IPO.

Except now, the focus is on the Bitcoin ETF.

The outflows from Grayscale GBTC redemptions have slowed which is helpful.

The spot market is in a funk and may need a few weeks to clear out excessive sentiment surrounding the ETF.

Don’t forget - the Superbowl is coming soon. I expect we’ll see some crypto ads.

A relative value expression in crypto offers the best risk-adjusted return.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Quote of the Week

“If you’re prepared to invest in a company, then you ought to be able to explain why in simple language that a fifth grader could understand, and quickly enough so the fifth grader won’t get bored.” - Peter Lynch

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.