- Lumida Ledger

- Posts

- Fed Watch, Big Tech in Focus, Dubai

Fed Watch, Big Tech in Focus, Dubai

Justin Guilder & Ram Ahluwalia

February 04, 2024

Welcome back to the Lumida Ledger.

If you find this newsletter valuable, we’d greatly appreciate you sharing it far & wide with your network (social links on top right). That’s how we grow and keep the content free to read.

Here’s a preview of what we cover this week:

Macro: Fed Watch

Markets: Tech Valuations, MSFT, AI Services, Coreweave

Company Earnings: AAPL, META, MSFT, AMZN, GOOG

AI: Cyber security, Apple Vision Pro

Digital Assets: Bitcoin miners vs. Crypto Equities

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

This week Ram was in Dubai attending a conference and meeting clients and prospects

Here’s his quick take on the city.

Ram also describes why Investment Committees at big banks have a group think dynamic that favors stale Consensus ideas. That’s why you get GS putting Apple on its “conviction buy” list.

Over the last several weeks, Lumida has led on buy calls for Haliburton, Meta, and Cloudflare only to see investment banks catch up a few weeks later.

Macro

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Fed Watch. It’s official.

The crowd hallucinates just like AI.

No March rate cuts.

We saw it differently back in December and re-iterated our call last night.

I will link below to our non-Consensus initial Dec call for the receipts: “I still don't expect any easing in the months ahead - and certainly not 6 rate cuts like markets expect.”

We re-iterated our view weekly including the night before the FOMC meeting.

How did Goldman, JP Morgan, and Morgan Stanley’s army of economists and traders delude themselves?

Kind of amazing.

From WSJ:

‘Powell expressly pushed back against expectations that the Fed was preparing to cut rates at its next meeting in March.‘

Other calls we publicly made on X came in

SoFi down (shorted Monday, closed 3 days later)

Brookfield Asset management down (short call, cover 3 days later)

Mr. Market is putting great businesses on sale.

We also purchased Google on sale after it dropped 8% on earnings. Recall, Google and other stocks we like - Z Scalar and Palo Alto Networks (in our cybersecurity theme) - dropped 8% and rallied over the next few weeks in the prior quarter.

Our approach is to do the research beforehand so you know what to buy when you see value.

Markets tanked on the FOMC day - one its largest drops on any FOMC day.

On Thursday, Apple reported earnings and closed lower. As you know, we’ve been skeptical of both Tesla and Apple - and that’s playing out in earnings.

Meta, on the other hand, reported and had a 20% boost. We’ve talked about our preferences in Mag 7 quite a bit.

We were on a podcast with Howard Lindzon talking about Meta, Google, our skepticism of Apple just last week.

Meta was up 20% on earnings, and Apple was down.

Apple is guiding towards a 5% revenue decline next quarter… Hard to justify a high valuation for a growth stock when you aren’t growing.

(See our prior tweets on growth to value transitions - a topic we are keenly paranoid about.)

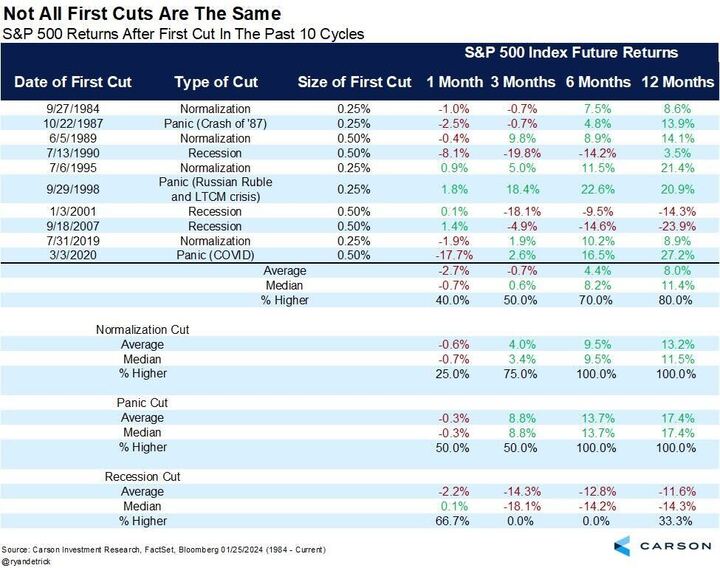

What to make of FOMC and the Strong Jobs report?

Last year, markets also got ahead of themselves with Fed pivot talk.

The pivot never arrived - even with the March and April banking crisis.

The key is the economy continues to grow.

We believe so long as the consumer and economy hang in there, the market can digest FOMC expectations.

Here’s a nice table showing the performance of equity markets under various scenarios.

We should note, February is one of the weakest months for tech stocks. And, we now are on the other side of ‘positive AI catalysts’ since earnings for Apple, Google, Amazon and Meta are behind us. (Nvidia reports quite late in the cycle.)

We’ve noted for some time that AI is the dominant theme in markets. It’s not Mag 7. It’s AI all the time - and that narrative is fanned by Goldman Sachs and Altimeter and Brad Gerstner and more.

We like that thesis - but are betting on the semiconductor layer.

We believe we are close to a local top in the AI thesis and we should see some weakness in Feb or Q1 more generally.

We would caution folks on getting overly bearish however.

As we noted in our early January studies comparing the overbought market to 1986 and 2017 - pullbacks should be short.

The market is certainly in need of a pull-back and expensive prices can cause a buyer’s strike.

Inevitably some counter-trend economic news, or perhaps China, or a geopolitical escalation will cause some weakness.

These are tactical considerations though - they guide maneuvering more than anything else.

Some of the hedges we like in this environment are ARKK. High volatility momentum stocks had a terrible January as the retail bubble deflates. That can continue.

ARKK somehow has managed to combine all the hype stocks into a single ETF.

Remember Beyond Meat? Tesla? Palantir? These are not the best stocks to own in our view.

Goldman Sachs put out this note on FOMC day

‘FOMC will likely aim to keep a March rate cut on the table’

My, oh my, did they screw this up

We led GS on Haliburton, Cloudflare, Tesla and now the rate call.

We routinely call our views in contrast to the big banks.

Consider that Goldman’s army of traders and economists are wrong.

They can’t help be a part of Consensus formation.

See Ram’s video here to understand why committees are terrible at investing.

There’s a reason why investment firms are noted by their leaders: Seth Klarman, John Templeton, Ken Fisher, Peter Lynch.

Take the leader out and you’ll get dramatically different results.

This is an oldie but a goodie meme that caused us to chuckle.

If there’s a lesson we would like to reiterate - be skeptical of sell-side research.

How Non-Consensus Macro Works

This thread shows the steady progression of 80% chance of rate cut to 60% chance of no rate cut…

We start from the day of the FOMC and gradually show news in real-time and track the probability shifts including our own commentary.

This was a terrific non-consensus macro call.

When markets are at an extreme and you have several months to go before a key event, the asymmetry of probability favors the other side.

It’s almost inevitable that news arrives and challenges the Consensus.

Markets

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Market Compass

Let’s cycle through our three-prong market compass as we look to the week ahead.

1. The 10 year bond yield declined over the week at 4.02%, down 12 bps WoW (mostly noise).

When this increases, that hurts valuations for long duration stocks.

2. The US Dollar is turning up, currently at 103.97 (Up by 2.55% YTD)

When the USD increases in values, US equities decrease in value.

The US dollar is at a crossroads. If it breaks that resistance level, we’re in a risk-off mode.

3. Semiconductors are up.

Semiconductors are an expression of AI narrative.

The SMH ETF moved up by ~1.5% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average.

We don’t believe now is the time to chase semiconductors.

NVDA is up ~33% YTD. We own it and bought some the second week of January. Now we are sitting on our hands.

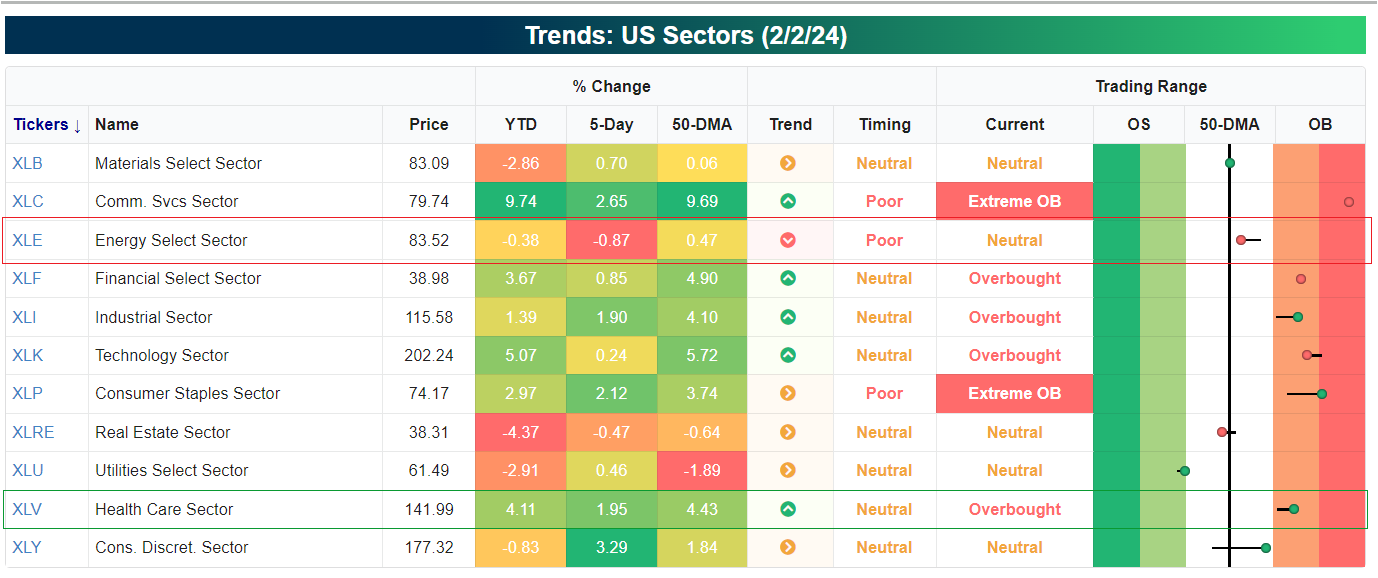

4. US Sector Trends

Healthcare is up ~2% since last week.

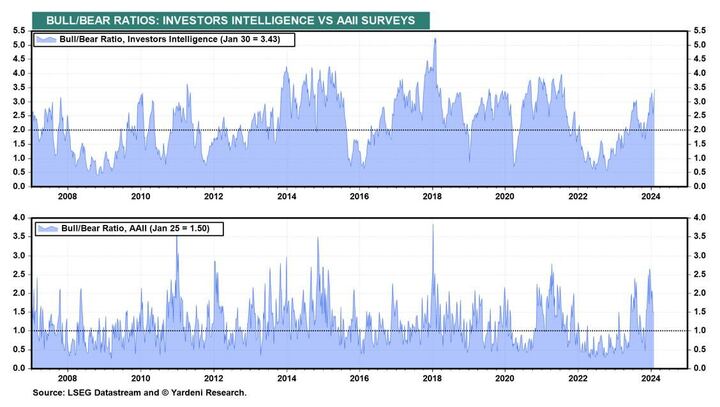

Here’s more data showing sentiment is running too hot.

If you were to overlay this sentiment chart with the S&P 500, you would notice the best times to buy were when sentiment is depressed.

Now, this is a bull market. But, you want to be mindful of not chasing.

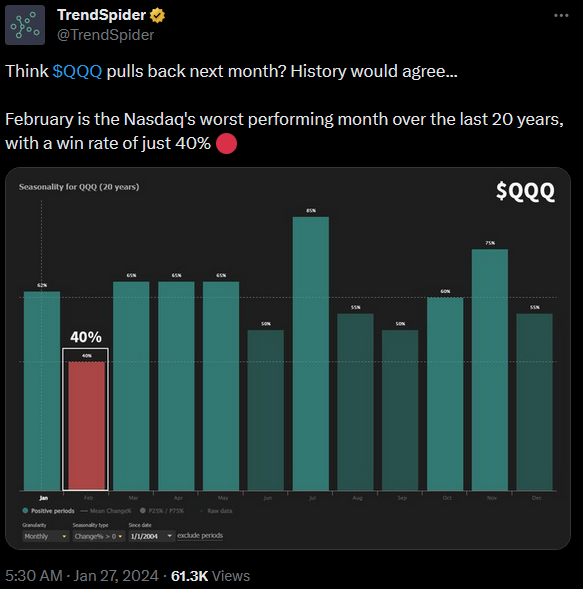

February could be just what the doctor ordered. February is the Nasdaq's worst performing month over the last 20 years, with a win rate of just 40%.

Seasonality has been working - Q4 rally, Aug to September weakness, January tech rally.

Stick with it.

Tech Valuations

We began the year noting tech valuations were at a 99% percentile.

The deflating of the Tesla bubble (and it will have more room to fall), and the capping of Apple’s valuation is helping to fix these market valuation issues.

Tesla had a big weight in the S&P and QQQ.

Market cap weighted indices are digesting bad news from Tesla and Apple - and lowering their share of the indices. Markets are also shrugging off FOMC and China news.

That deserves a mark in the bullish column.

When bad news doesn’t impact stocks for more than a day, then that is bullish from a longer-term perspective.

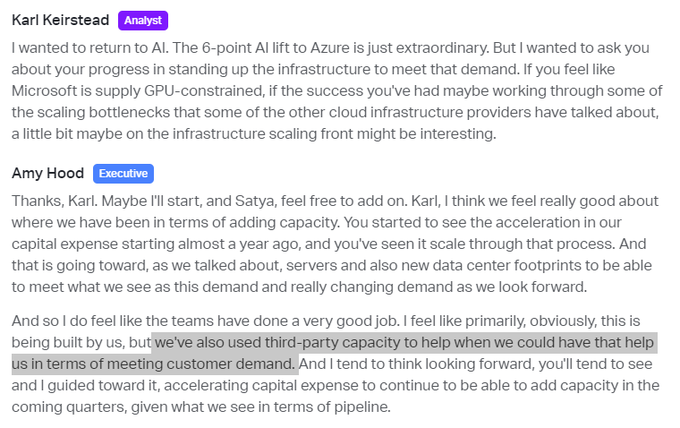

Microsoft

Here’s a thread with our highlights on Microsoft’s earnings.

We view Microsoft as Consensus AI. It's a world class business - perhaps the best in the world. It’s also expensive. There is no Non-Consensus return opportunity with Microsoft.

It’s better to own businesses that have some dents and scratches. Management can address those. Then you sell the business when it is nice and shiny back to Mr. Market at a higher price.

A good example is Lending Club. The stock is up 60% in 3 months.

We don’t own it. But, it’s a good example of a ‘left for dead’ stock that has quietly rallied.

SoFi is the opposite. It is over-hyped. It has a social media bot farm promoting the stock. That, in a contrary manner, hurts the stock. There’s no one left to buy.

Be suspicious of heavily promoted stocks on social media. Notice those stocks - Tesla, SoFi, Lucid, Rivian, Bitcoin miners - are not working!

Meanwhile, one of Lumida’s Stocking Stuffer stock picks - Hershey’s - is out-performing both the S&P 500 and QQQ!

No one was talking about Hershey’s… Now, it has some initial momentum. It starts with leadership - like our call. Then other people see our view. Then Mr. Market comes to our side of the seesaw. And they sell the over-hyped securities to make room.

Do you see the difference in our contrarian approach? Be skeptical of the crowd.

SaaS- Altimeter Highlights

In the last 3 quarters AI Services run rate has gone ~$500 MM to ~$2B and now to ~$4B $MSFT.

AI is accelerating, not at the consumer level, but at the enterprise level.

Microsoft’s Azure now has a ~$74B run rate growing 28% constant currency

There are two AI traps:

Many AI software firms do not have the same AI revenue growth as Microsoft or other players. But they identify around AI. A good example is IBM.

There are AI firms that are subject to the Innovator’s Dilemma. They are embracing AI, but there’s a fair chance AI will disrupt them in a few years. That thesis is not worth acting on today, but you need to keep that risk factor in your foreground. Examples:

Midjourney reduces the need for Adobe

AI CRMs reduce the need for Salesforce

We also like AI incidental winners - such as Cybersecurity firms.

We love this thesis and our preferred names here have done quite well. One, Palo Alto Networks, is a Lumida Wealth stocking stuffer and its up double-digits YTD.

Palo Alto Networks is now overbought. We don’t advise chasing it here, wait for a pullback.

CoreWeave

Have you heard of CoreWeave? If not, you should learn more.

They should IPO on or around Q4 ‘24. We own the stock.

CoreWeave is the 3rd party provider powering Microsoft and OpenAI.

We aren’t a big fan of IPOs where VCs unload unproven models on to the public… but Coreweave looks like a real opportunity.

It will be one of the mostly hotly anticipated IPOs I expect. Check out their podcasts on Odd Lots or Acquired to learn more.

Long: CoreWeave

The Big Takeaway is Big Tech Cloud AI growth is accelerating

We noted a few weeks ago that SaaS revenue is also accelerating.

We like owning both of these trends.

Microsoft noted the “period of massive optimization only and no new workloads has ended.” We are shifting from a cost-cutting mindset to a growth mindset.

That’s bullish for the AI thesis, semiconductors, and software longer-term.

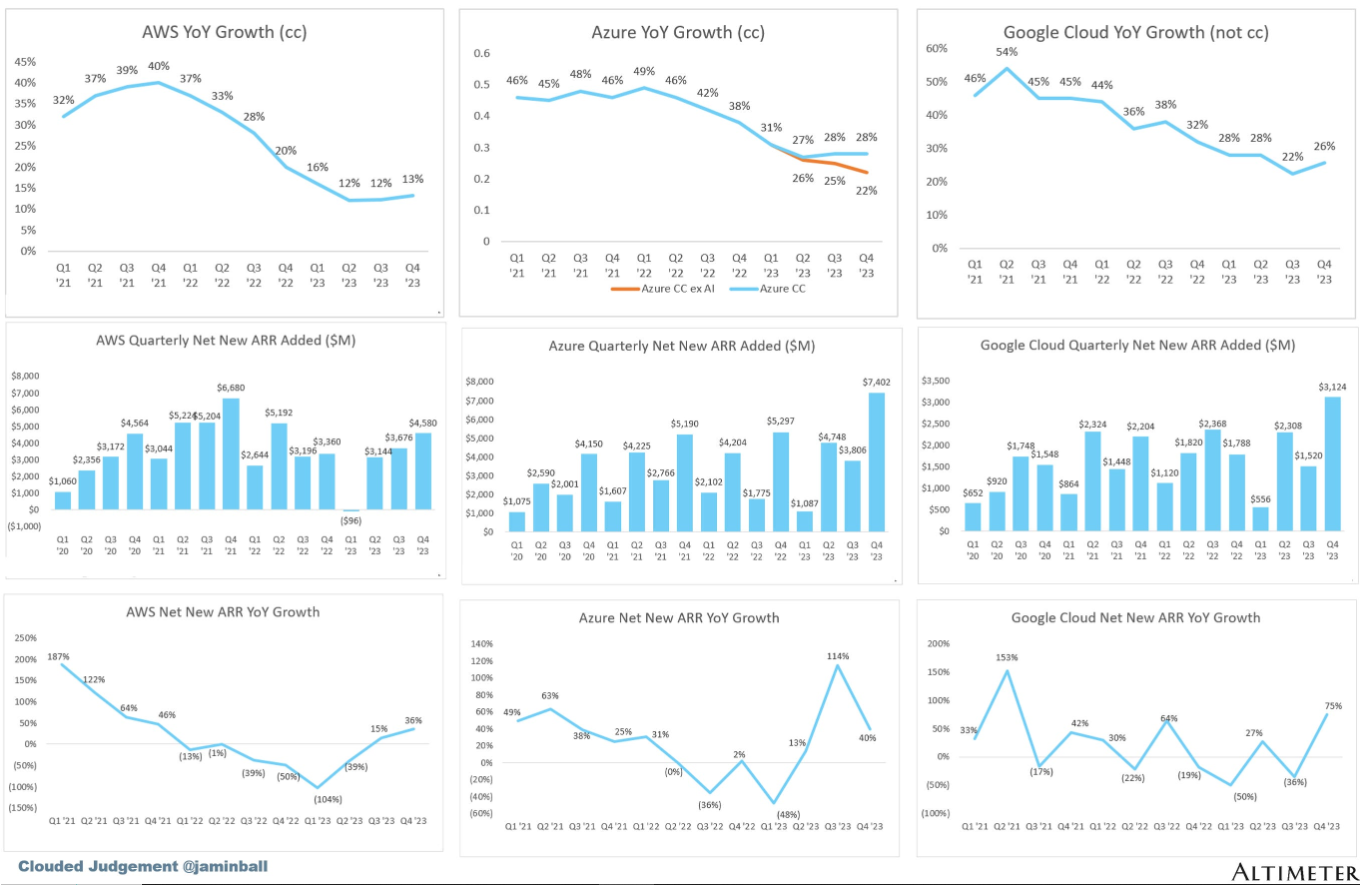

AWS (Amazon): $97B run rate growing 13% YoY (last Q grew 12%)

Azure (Microsoft): ~$74B run rate (estimate) growing 28% YoY (last Q grew 28%)

Google Cloud (includes GSuite): $37B run rate growing 26% YoY (last Q grew 22%, neither are cc)

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Company Earnings

Observations:

Winners:

Meta has set a record for biggest 1-day earnings pop ever. Amazing. We still think Meta is a great asset to own.

Mastercard / Visa - some of the best businesses (oligopolies) in the world.

Google is on sale. We bought it and are adding more after the stock dropped ~7 to 8% like last quarter.

Losers:

SoFi popped 20% on earnings. Then it bled back all the gains. This is classic SoFi as management seeks to pump their stock on earnings. We had no position in SoFi going into earnings. We initiated a short near the close of Monday and closed a few days later for a nice gain.

Broader trends observed this earnings season:

Sellers to China are feeling the pinch

We saw Apple get whacked due to exposure to China

Now Starbucks is feeling the pinch

Nike showed the pain from China exposure last quarter

Underweight equities exposed to the China consumer

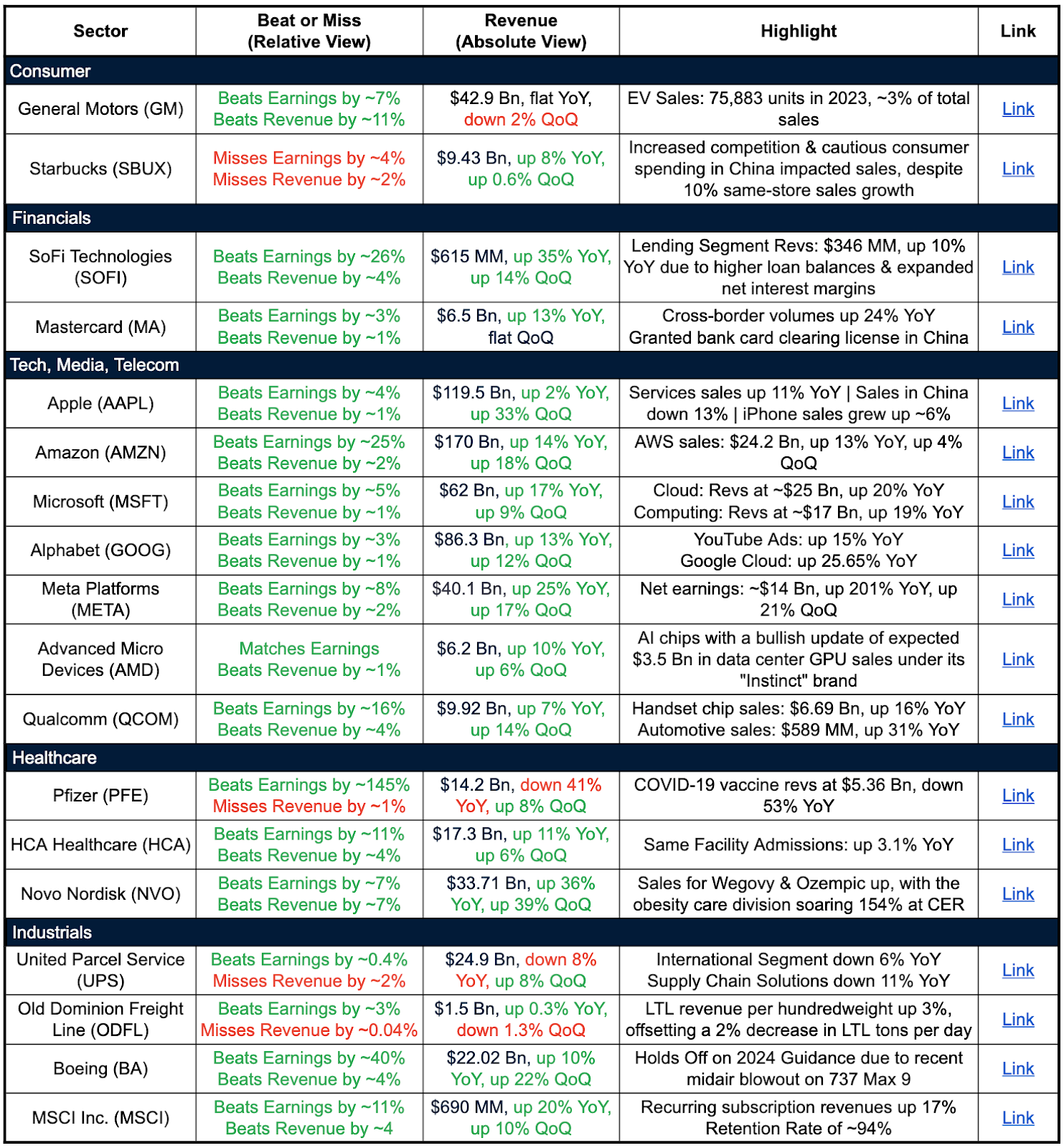

Tech, Media, Telecom

Companies reported: AAPL, AMZN, MSFT, META, NFLX

Trend:

All companies beat estimates on earnings and revenues

Cloud services & digital ads still seeing strong growth

Aviation - Travel

Companies Reported: UAL, AAL, UPS, ODFL

Trend:

Reported strong earnings, however, revenue was down QoQ, (suggests a slight decrease in demand for air travel)

American Airlines, achieved its best-ever Q4 and full-year completion factor, with the lowest number of cancellations

Decline in freight volumes, challenges in logistics and supply chain

Chip manufacturing

Companies Reported: INTC, ASML, LAM, AMD, QCOM

Trend:

All companies beat estimates on earnings and revenues

Revenue is up QoQ across companies, with only LAM being down YoY

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

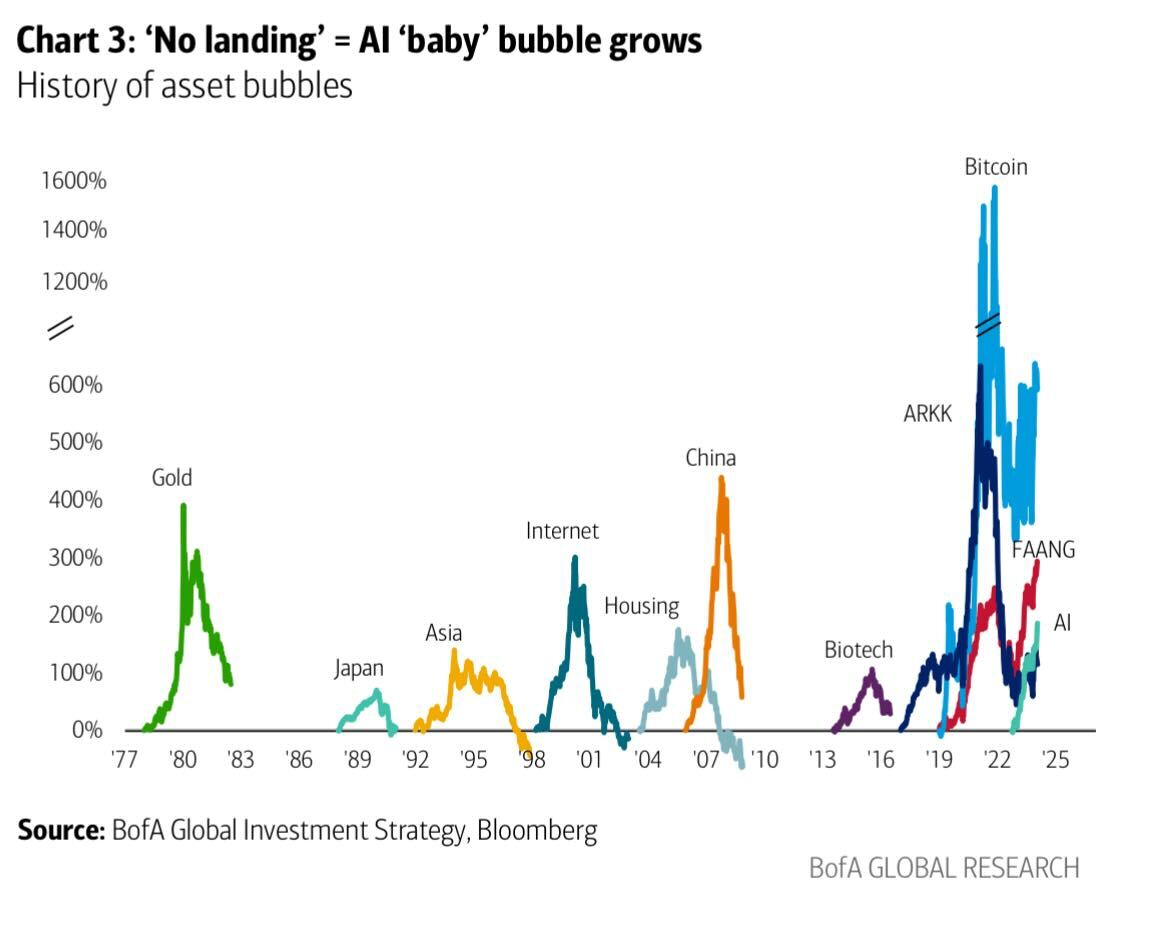

Markets and Bubbles

Have a look at the following charts. We are certainly in a speculative zone given how the 10-year and equity indices are positively correlated.

ARKK does a great job of capturing bubble stocks and then disinflating.

Bubbles are constantly inflating and disinflating: cannabis, neo-banks, the GBTC widowmaker, biotech stocks, GLPs, bitcoin miners…

Maintain a sense of awareness of where we are and don’t get swept up with FOMO.

Bubbles are an inevitable part of human psychology.

You can’t avoid them, and you shouldn’t. The S&P is a market-cap weighted index and it is benefitting from the growth of the biggest bubble yet to come - the AI bubble.

We still have room to run longer-term on that theme, even if February we see a pullback.

What’s working and not working

The top of the list will tell you where there is momentum. The bottom of the list will tell you where there is value.

China’s equities look like they will capitulate in February, and possibly this week.

We are starting to see increased signs of indiscriminate selling. China’s local market retail investors are increasingly throwing in the towel.

Chinese investors are giving up hope and giving up. Those are markers that an intermediate bottom may be near.

As Trump’s political fortunes rise, however, that will continue to pressure China’s equity markets.

There are many cross-cutting factors here. Better to be patient and wait for concrete evidence of capitulation before leaping in.

On AI & Cybersecurity

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Hackers have valuable confidential security information from the US Government.

This trend will only increase over time.

Sovereigns, corporates, and households need to invest in cybersecurity. We love that investment theme…

Apple Vision Pro

Our take?

Not enough to move the revenue or earnings needle for Apple even at $5 Bn in sales.

Further, Vision Pro needs to prove out product market fit.

Remember the Amazon Zune? Or Apple’s Newton?

Distribution alone is not enough to create a new category.

Flops happen.

Apple is betting the farm on Vision Pro. At Apple’s current valuation, one should not give the benefit of the doubt.

Here’s a cool clip of the Apple Vision Pro - we try to stay open minded.

Jay Powell is Speaking on 60 Minutes This February

We should note February has weak seasonality for Technology stocks.

We’re also just past peak hype from a slew of AI earnings related calls.

Nvidia won’t report soon to save the day.

We suggest not chasing, and consider hedging. Stay net long, but a good hedge can help to blunt some volatility. We think ARKK is a great hedge.

Also, Powell is speaking this Sunday on 60 Minutes. He’s not going to deliver an inflation victory lap here.

Digital Assets

Crypto

The halving is two months and change away.

We believe miners, which will lose 50% of their revenue, are in a bad position and have too much debt.

The least levered miners will gain share and likely acquire the rest.

Mining will inevitably consolidate.

Spot assets should continue to out-perform crypto equities.

We prefer certain publicly listed closed-end funds where you can continue to get a discount to NAV.

If you find this newsletter valuable, we’d greatly appreciate you sharing it far & wide with your network (social links on top right). That’s how we grow and keep the content free to read.

Quote of the Week

“We don’t have to be smarter than the rest. We have to be more disciplined than the rest.” - Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.eech