- Lumida Ledger

- Posts

- The EV Bubble is Deflating, JP Morgan Retrospective, Mag 7 Check-In

The EV Bubble is Deflating, JP Morgan Retrospective, Mag 7 Check-In

Ram Ahluwalia

January 14, 2024

Welcome back to the Lumida Ledger. Here’s a preview of what we cover this week:

Macro: Inflation expectation, China 10Y Yield

Markets: 2024 outlook; Semis on Sale?; More Small Caps studies

Company Earnings: Banks earnings

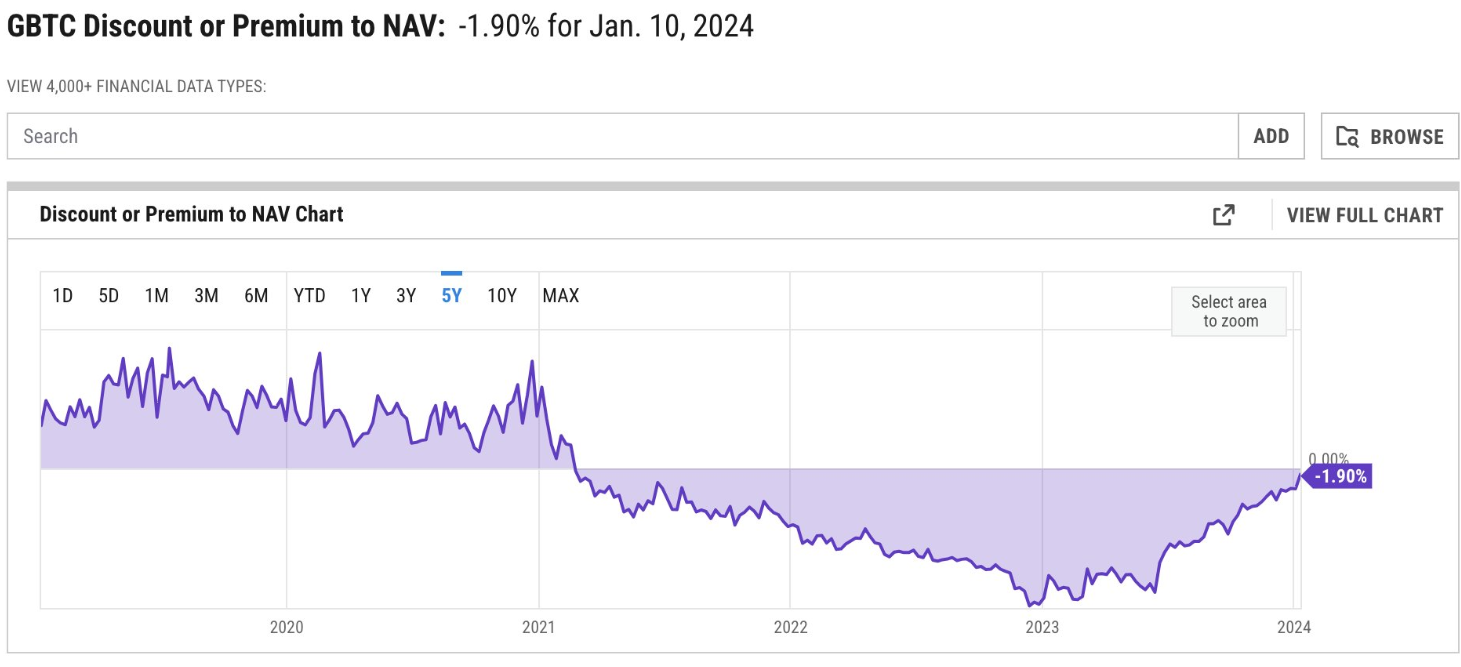

Digital Assets: GBTC, Bitcoin ETF

AI: Fintech & AI trends, SaaS Valuations, Mobileye

This week we had an engaging conversation with Geoff Yang, Founder of Apeiron Life and Venture Capital firm Redpoint Ventures. Geoff is a great investor and a founder himself. He has backed companies such as Ask.com, Juniper Networks, Scribd and built businesses with stars like Matt Damon, Ben Affleck and LL Cool J. He has a keen eye for identifying consumer trends and building scalable businesses around it.

In this Lumida Legacy episode, Justin & Geoff discuss everything on health, longevity, and routines across the 4 health dimensions : cognitive, metabolic, emotional, and physical.

Click below to tune in & don’t forget to leave a review and subscribe.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

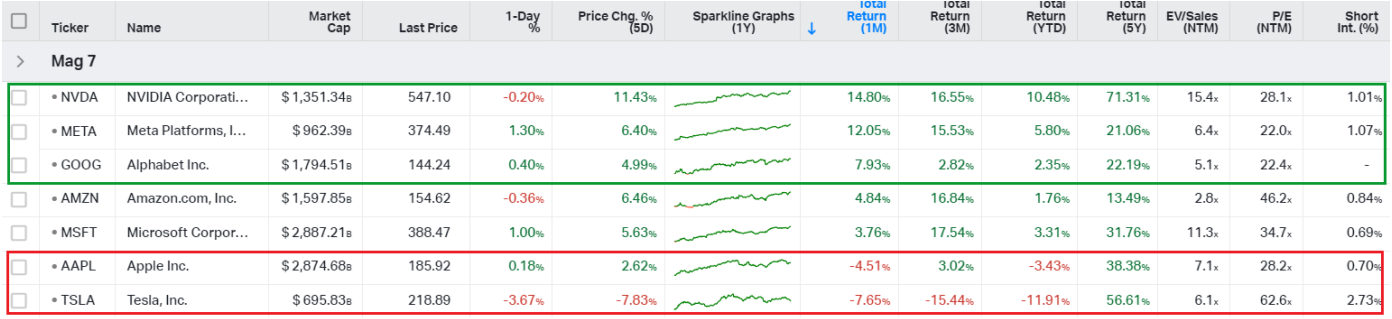

Mag 7 Check-in

Tech started the year at a 99%-ile valuation. And, more importantly, everyone is long.

We pointed out that the tech stocks are overvalued and are due for correction.

Within Mag 7, who is leading? Nvidia, Meta, and Google. Those are our overweights.

Then who is negative for the year within Mag 7? Tesla and Apple.

Whenever I listen to Bloomberg, I always hear ‘Microsoft is how to bet on AI’.

Microsoft is Consensus. It will do a Consensus Return.

What does that mean? It means Microsoft, at best, will earn the market return owing to its ‘beta’ or ‘factor exposures’. If tech does well this year, Microsoft will follow that path based on its sensitivity to technology.

There is no ‘excess’ return opportunity. And there is risk of Consensus shifting should our favorite Google, which is outperforming Microsoft, execute with Gemini Ultra. And our research suggests that Google will gain the spotlight ultimately.

CyberSecurity

One of our stocking stuffer names hit an all-time high this week - Palo Alto Networks.

Wait for a pullback before adding to that position. It’s overbought now and we expect it will pull back.

Much of this week was the market hitting the November and December note this week - that’s partly driven by the vibes coming out of the historic CES conference. January is one of the best months for tech and this week especially.

MLK week is generally weaker.

Non-Consensus:

There is an invisible bubble that no one is talking about.

That bubble blew up and is deflating now.

Electrical vehicle stocks (EVs) are a bubble and that bubble is deflating.

Competition is intensifying.

China manufactures more autos and EVs globally now.

The leading indicators for TSLA are Lucid and Rivian.

Those two are getting hammered.

How about fundamentals?

Look at Tesla’s share price (black line) versus forward earnings estimates (blue line) on this chart

Tesla is forced into price cuts to maintain revenue growth.

It’s a high operating leverage business - like the airlines - where you are as smart as your dumbest competitor.

(Meaning if your competitor prices low, you have to match so you can capture your share and fill the plane and cover fixed costs)

Tesla’s stock has gone nowhere in 3 years.

It appears to be rolling over.

And the prospect of Fed rate cuts was the last hurrah.

You heard it here first: EV was the latest bubble to blow…

and we expect more downside in Tesla.

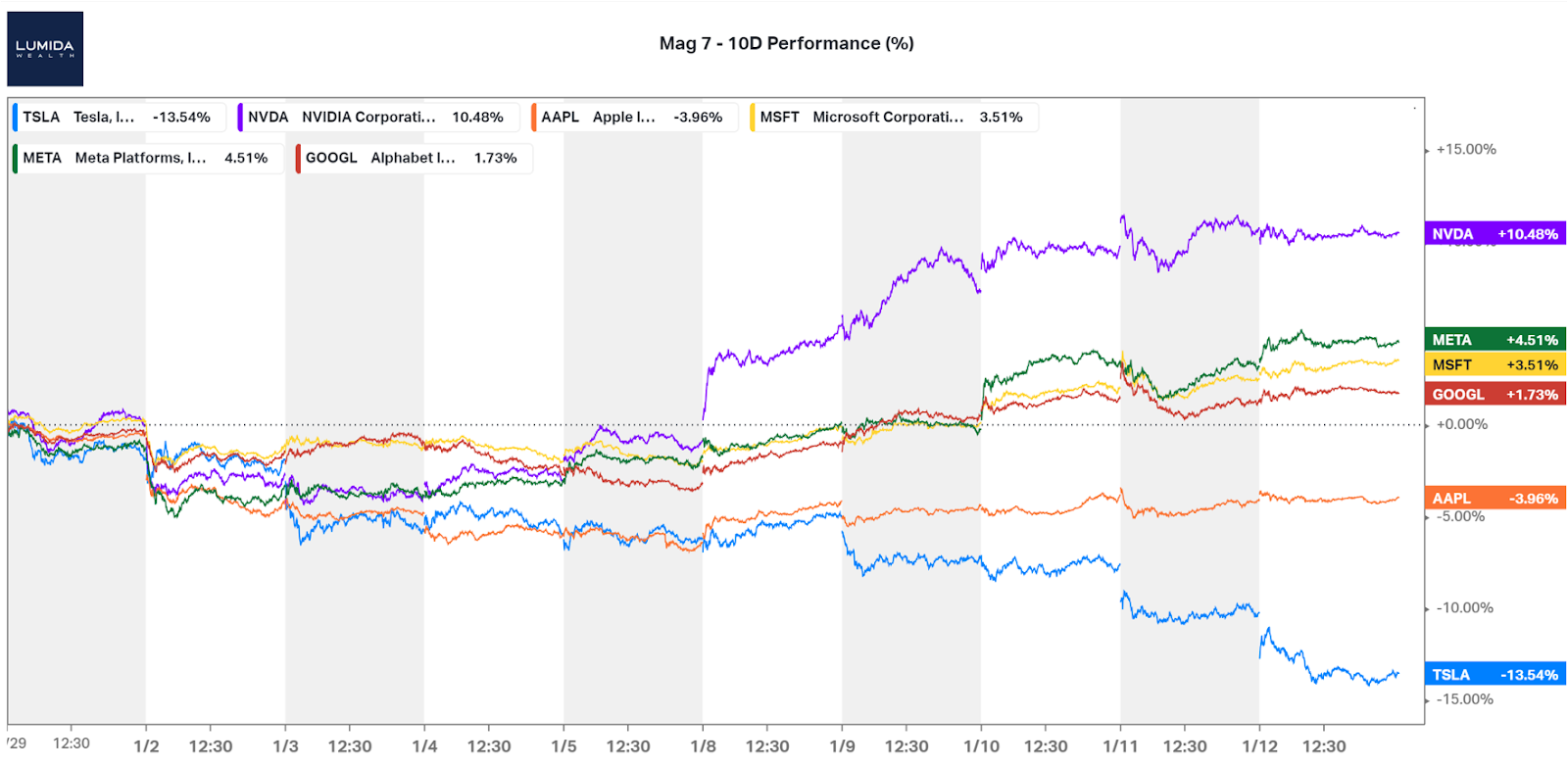

Tesla

Tesla has lagged in comparison to other Mag 7.

We recommended last week to short Tesla effectively as a hedge against other names.

Tesla has broken to new lows. On 12/30 we noted “Tesla sticks out like a sore thumb.”

Take a look at Lucid and Rivian. These are smaller EV companies that are leading indicators for Tesla. They are plumbing new lows.

China is now the leading EV manufacturer.

When competition intensifies, we want to get out of that sector. And when valuations are at nosebleed valuations - you need to rotate out.

We have noted many times, Tesla’s stock has gone nowhere in 3 years. It’s no longer a wealth creator.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Investing Tip:

There is no such thing as a single idealized portfolio that everyone should own at any time.

This is an important concept to grasp.

And when you get it, you won’t look at ETFs or legacy wealth managers the same way again.

Example: We bought JP Morgan in March. We wrote about when we did it on Twitter, and called a bottom in financials.

We were 2 weeks early on that, but got the main idea (and rewards).

Would I buy JP Morgan today? No way. It’s fully priced now.

Should you sell? No. Long-term capital gains. Just hold it in your portfolio and let it compound. JP Morgan has a 30%+ ROE in its consumer bank - you’ll do fine.

But for new investors buying JP Morgan is not the right idea.

The optimal portfolio for you depends on when you invest due to capital gains taxes and the fact that “you make your money on the buy.”

If there were no taxes, all of our clients would have identical portfolios.

Clients that we deployed in October were able to buy semiconductors near the lows and are up sharply.

Nvidia was the only ‘cheap’ semiconductor in new year, and that was the only semiconductor we purchased

We do have an asset allocation that we target and seek to build over a 3 to 6 month deployment period.

So, the sector weights and style factors will resemble one another, the exact names may vary.

We always have our basket of preferred names in each sector. And we are constantly assessing that against the prices Mr. Market is offering.

We attempt to vector to the best long-term names we want to own backed by a secular investment theme we believe is durable. But we insist on a valuation worth paying for.

Hedge Funds Are Not as Good as Separately Managed Accounts

A hedge fund is a commingled vehicle. Everyone has a pro-rata share of the same holdings.

And everyone has a pro-rata share of the taxes.

So, if a clever hedge fund bought semiconductors in October and banks in March and Uranium in the early summer (like we did), you’d be buying at today’s prices. And not all of the ideas make sense at current prices.

Hedge funds are a dated form of technology.

Consider that legacy wealth managers neither think nor operate like this.

Goldman Sachs vs. Lumida Approach

I had a portfolio review with a prospect the other day who wants to transition away from Goldman Sachs.

As a part of our review, we’ll do a consultative ‘quick take’ on their current holdings.

What we found, and we see this often, is:

Only ETFs: this deprives the client of the ability to tax loss harvest at the security level. That’s a BIG deal. On average, ⅔ of the members of the S&P are down at any given time. If you can’t tax loss harvest those names, you are leaving money on the table. You should not own broad based sector equity ETFs except for highly tactical purposes.

The ETFs are all built by Goldman Sachs Asset Management (GSAM) - the Goldman Affiliate. That’s a conflict. Is GSAM the absolutely best ETF designer for all strategies everywhere and anywhere? No.

There are no individual securities. If you can add value identifying mispricings, there is considerable upside from doing so.

For example, we called out American Public Education (APEI) and Build a Bear (BBW) in our Top 10 Stocking stuffer list.

The average of those names is out-performing the IWM small cap index handily.

Take a look at APEI here. We first mentioned it on Twitter in early December… Next time someone says ‘You must own Mag 7’ just show them this chart.

We prefer APEI as overweight in small caps. APEI is one of our stocking stuffer picks.

The stock is cheap relative to its growth rate with PEG (NTM) ratio of 1.32x.

The damn thing is up 100% in two months. It’s running up as we are growing new clientele and seeking to deploy while maintaining discipline. (BBW, another stocking stuffer pick, is flat.)

This is why we are feverishly researching other small cap names - and there is value out there. We bought Crox two Thursday ago. Then it jumped 20% on the following Monday.

This is what happens beneath the surface of the indices.

The big money managers are rotating to small caps by macro-focused index products. Those lift the largest market caps in the space. There is plenty of opportunity in small caps remaining.

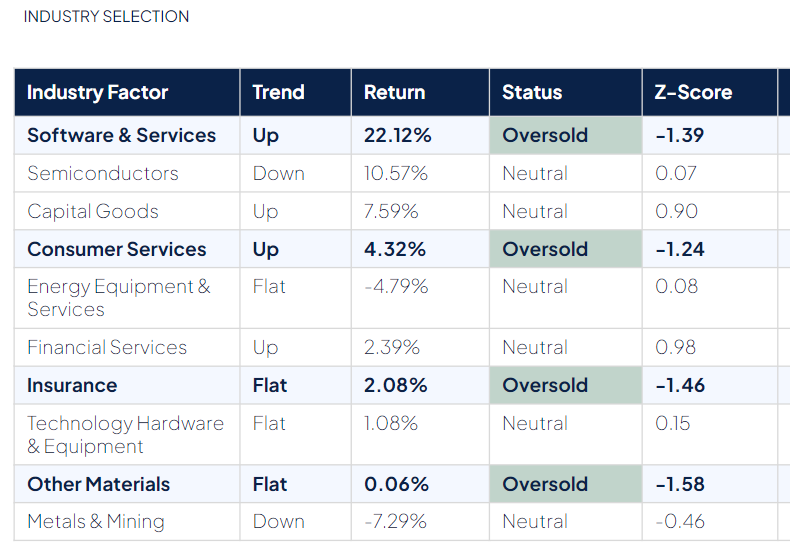

We do want to iterate that if you want to get back in the market, now is a good time. Small caps, biotech, and energy should be accumulated in this period. Within tech - the software services sector is statistically oversold and we’re picking up there as well.

(Note: We have a much broader list of small caps we like, but we try to illustrate a few ideas to show our thought process.)

Index level returns mask the broad level of return dispersion underneath the surface.

A widely quoted statistic is that small caps have a negative forward EPS outlook.

That’s true. On average. But it’s not true for those two stocks. When the entire category is trading at a discount, that creates an opportunity to sift thru and find quality businesses and own them.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

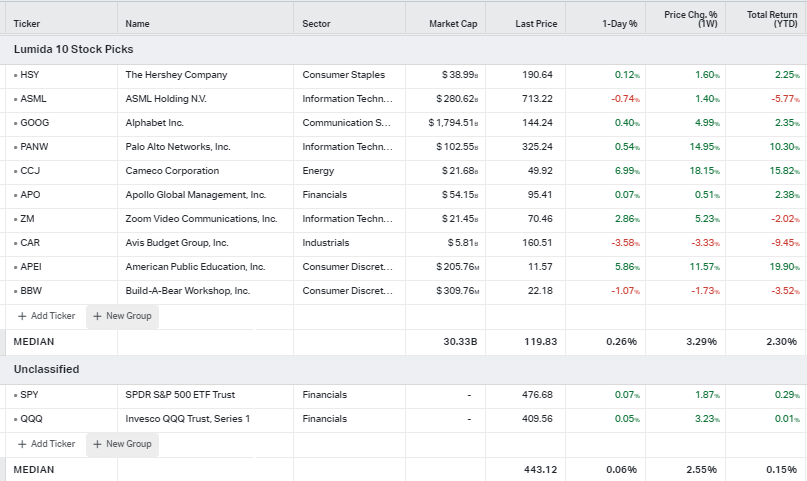

Lumida Stocking Stuffer Portfolio Check-In

At any given time, we likely hold dozens and dozens of positions and perhaps half-a-dozen or so shorts to offset certain risks.

We put this Lumida 10 Stock Stocking Stuffers portfolio. It only has 2 tech stocks. And we wanted names that are Non-Consensus.

How is it doing vs. the S&P and QQQ?

It’s up 2.3% on the year.

The S&P is up 30 bps. The QQQ is flat.

We believe several of these names are overbought now.

February, deep into earnings season, is generally went corporates start updating buyback policy.

We want to see what Hershey’s and Build a Bear has to say then.

As we noted earlier, on any given week, the ‘optimal’ portfolio to acquire is not the same as last week.

There might be overlap, but it’s rarely the same. And, in fact, our views may go negative. For example, we believe Palo Alto Networks is too expensive now and this setup is begging for mean reversion.

Any given week, views can change because the prices and valuations matter.

Last week we bought Crox two weeks ago. That would have been on that weeks ‘Top 10 List’. We were lucky, and the following Monday the stock jumped 20%. Would we buy it at those levels? No.

So, these lists including static ‘Conviction Buy’ lists are little more entertainment than good investing.

They reveal just how backwards the legacy wealth management industry is.

If you want to replicate our strategies, the best thing to do is just give us a call and get back to what you do best.

On SoFi

We are long the tech sector but have a highly differentiated approach as our readers know.

Now and then we take small short positions in stocks that help us bring our portfolio factor exposures into balance. It’s great when we also have a view on the stock.

The weights of these positions are around 1 to 2% on average - less the more volatile the security.

We also don’t stick around for long, we like to turn those over and monetize quickly the more volatility the security is.

Simplifying a bit, but that allows you to isolate the alpha. And rotating quickly let’s you pick off excesses of the market. Keeping positions small let’s you avoid a short running up against you and having it matter.

Pleased to report that we are now 3 for 3 in calling out our SoFi shorts.

Here’s our summary view of SoFi with a little humor: Join in on the conversation

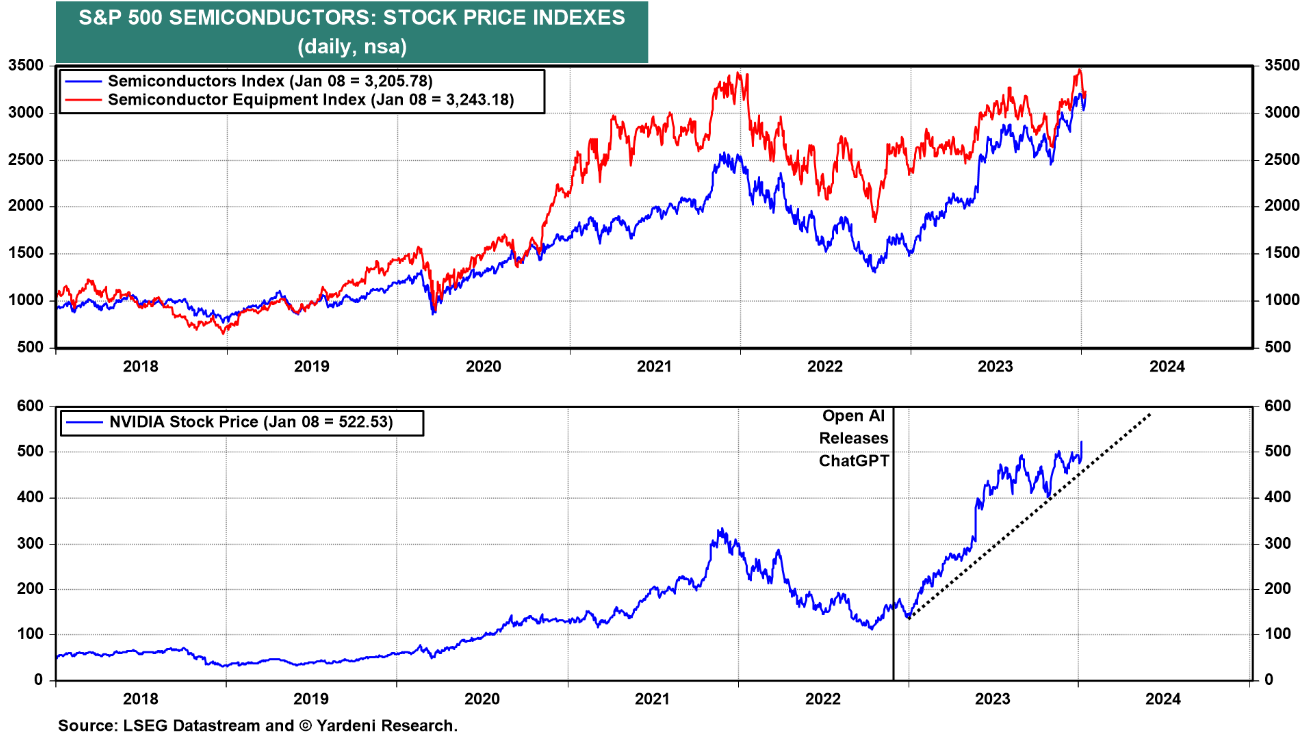

Nvidia:

Nvidia had its best 2-day gain since its May 2023 earnings blowout.

Recall, we highlighted in our newsletter one two weeks ago that Nvidia will outperform other semiconductors - including ASML and AVGO.

You can read our “call” below”

We also noted in our 12/30 letter that Nvidia has a lower forward P/E than Apple. That’s stil true today.

The reality is very few wealth managers apply critical thinking in portfolio construction.

Morningstar, the leading provider of SMAs and indices to wealth managers, has two flagship products: Growth and Value. The top holding in the Growth index? Apple. The top holding in the Value fund: Berkshire Hathaway. That is another way of saying Apple. (50% of Berkshire ownership is in Apple).

Apple was a great buy in the past - and we owned it then - but not now.

We expect NVIDIA to rise further.

Market Compass

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Let’s cycle through our three-prong market compass as we look to the week ahead.

1. The 10 year bond yield closes out the week at 3.94%, down 15 bps over the week.

The 10-year has tightened to 3.8% last month. It’s now heading back up to the 4% range we believe.

When the Ten-Year increases, that hurts valuations for long duration stocks.

2. The US Dollar is turning up (Up by 1.02% MTD)

When the USD increases in values, US equities decrease in value.

The ‘top is in’ on the dollar. You can see that it took place in October ‘23.

The trend is down. That’s bullish for risk assets. That’s the primary trend.

Don’t miss the squiggle for the trend.

3. Semiconductors are up.

Semiconductors are an expression of AI narrative.

That's headed up by ~5% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average.

We don’t believe now is the time to chase semiconductors.

Nvidia was the only semiconductor we bought with new money post January.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Macro

China’s 10 year yield is back to 5 year lows

The dip in yields is a deviation from typical global market movements.

Lower 10-year yields signal slower growth and greater risk aversion.

Investing in markets when sentiment is dour and the growth outlook is poor is historically when you are rewarded the most. That was the United States setup in 2023.

(It’s not too dissimilar from Europe today.)

AliBaba is starting to put in higher lows. BABA also rallied on days when the Nasdaq was down. That’s a sign that sellers have sold, and bad news is fully impounded.

Establishing starter positions in high quality names with audited accounting is a reasonable idea.

If you have a 3 to 5 year holding period, it’s hard not to see how you won’t be up significantly in that time frame.

We have been interviewing portfolio managers and experts on the ground on Lumida Non-Consensus Investing podcast.

We have ideas on how to approach China.

But, at this time, we are focused on accumulating small caps and biotech while patiently keeping an eye on China.

Note — the automobile sector is already in a major bull market in China.

You would never guess China was in a prolonged bear market looking at this sector.

These are the kinds of incongruities we look for. We want to challenge the status quo thinking, and ensure we are not lulled into the complacency of the Consensus narrative.

We have to remain mentally flexible and adjust our views when we see improvements that others are ignoring.

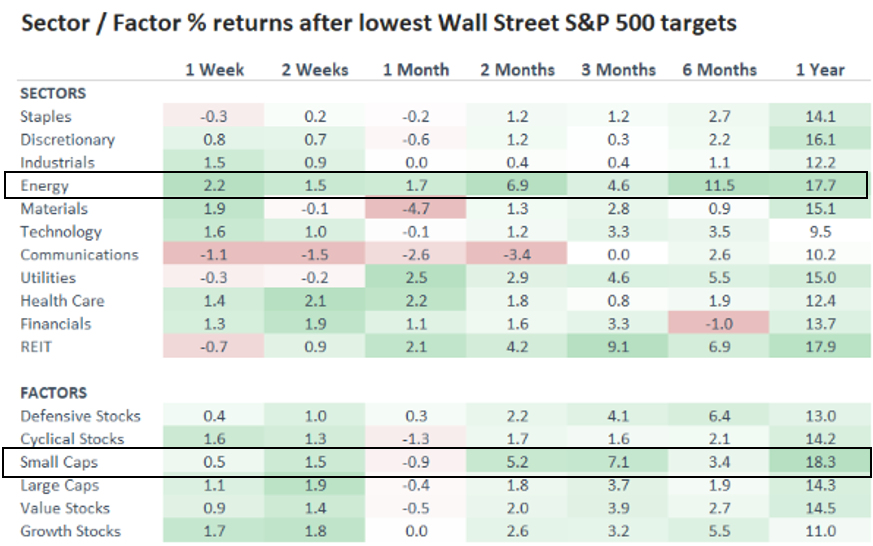

On Energy:

Here’s another bullish study on energy.

Wall Street put in a set of S&P 500 targets that are quite low. First off, that’s bullish for equities in a general sense.

Second, the sector that statistically performs the best? Energy and small caps.

The worst sector? Technology. At the start of the year, Tech was at a 99%-percentile valuation. That statistic squares with this table.

We do own technology: Meta, Google, Nvidia - and names like MongoDB, Zoom Info, PayCom, PAR Technology and quite a few others…

We want to match the S&P’s sector weight on tech – but then focus on our investment themes and insist on growth at a reasonable price.

Utilities should do well also… we pointed out in October utilities were oversold.

If you want conservative income and an inflation hedge, that’s a space to consider.

Earnings Season Is Upon Us

Analysts have lowered their expectations.

Earnings growth predictions have fallen from 6% to just 2% YOY for the coming quarter.

Lower expectations work in our favor. This is the pattern we want to see.

Recall in October, the growth expectations were 0%?

That was a contrarian's bullish cue.

Recently much of the buying was in the large-scale, macro products (broad market instruments).

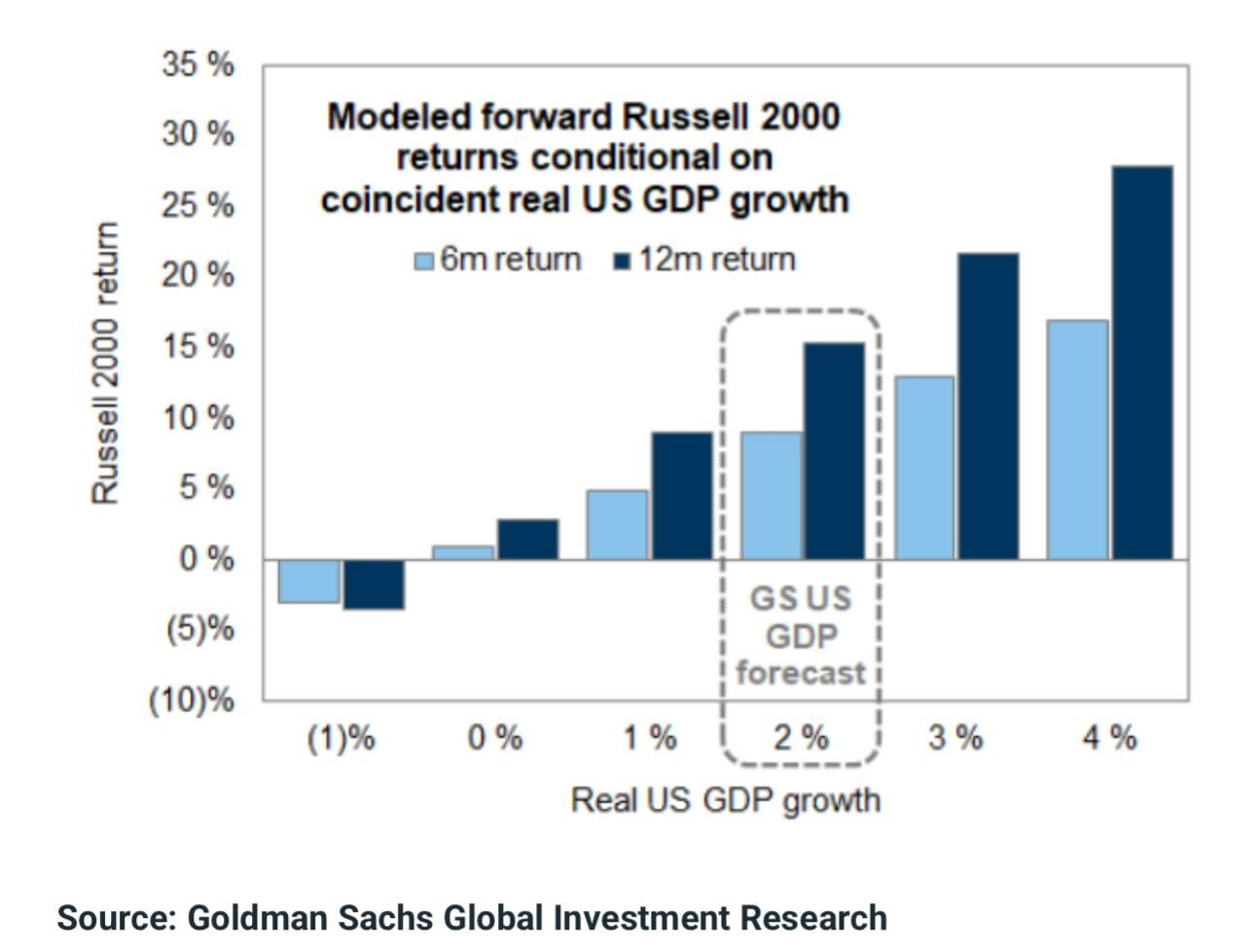

Markets: Another Bullish Study for Small Caps

Provided there is no recession, small caps should do well this year.

If real GDP comes in at 2% or more, small cap returns exceed 15% on average when looking across history.

50% of stock price returns are explained by multiple expansion. Small caps have plenty of room to run even though at the index level they are now close to their longer-term trailing PE.

We are still finding small caps with valuation ratios in the 6x to 10x range.

Finding these names takes a lot of work. There’s a lot of garbage to sift thru. But there are diamonds out there.

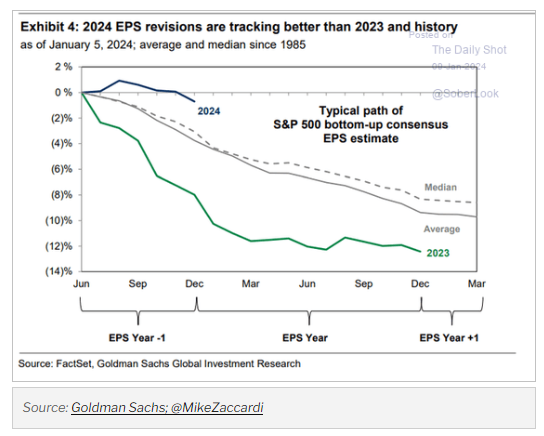

EPS Revisions 2024 vs 2023

The scale of downward earnings revisions for 2024 has been notably less compared to the usual trend.

Analysts are reducing their earnings forecasts…but not at the same pace as prior years.

We would prefer, like in 2023, that analysts grow bearish, and throw in the towel.

Mr. Market is dealing a mostly fairly valued hand unlike what we saw in 2023.

Active management, stock picking, and sector selection will do well this year. And as we see in our Top 10 Stock Stuffers and our own client portfolios we’re seeing that play out.

Jamie Dimon’s Comments on the Economy

“The U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing. It is important to note that the economy is being fueled by large amounts of government deficit spending and past stimulus.

There is also an ongoing need for increased spending due to the green economy, the restructuring of global supply chains, higher military spending and rising healthcare costs. This may lead inflation to be stickier and rates to be higher than markets expect.

On top of this, there are a number of downside risks to watch. Quantitative tightening is draining over $900 billion of liquidity from the system annually, and we have never seen a full cycle of tightening.”

JP Morgan Retrospective

We decided to look back at our call for a bottom in financials and JP Morgan itself during the banking crisis in 2023.

Take a close look at this chart and study the main headlines overlayed to the XLF (Financial Sector ETF).

You'll find invaluable insights for the next time there is a crisis.

1) Note how Regulation & Capital impacts the bank sector

2) Note the 'buy the rumor, sell the news events'.

The day PACW was bought was also the day the sector started to sell off.

The day JP Morgan acquired First Republic, the bank sector sold off.

3) Note the capitulation during March, and the elevated volume down days. Those technical factors help give a clue as to when to get a good entry.

You want to do these studies now so you know how to approach the next dislocation.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Company Earnings

Banks benefited from a 10-year that was around 3.8% at year-end. That helped their hold to maturity positions.

Commercial real estate risks have also disappeared from headlines. Although that’s primarily a risk for the regionals and small banks.

Roughly 20% of commercial buildings are vacant.

Now that we are in ‘24, annual audits and materiality testing will force a new round of lower ‘marks’ for the portfolio.

That should trigger more selling. There’s about $1.5 Tn in CRE debt that needs to be refinanced. So, those headlines should be coming back soon.

That said, banks have been in a clean-up and work-out model.

Let’s take a closer look at stats around the banking sector.

The forward P/E ratio for the industry is currently 10.5, up from a recent low but below historical averages.

Small banks have aggressively increased reserves due to their significant commercial real estate lending.

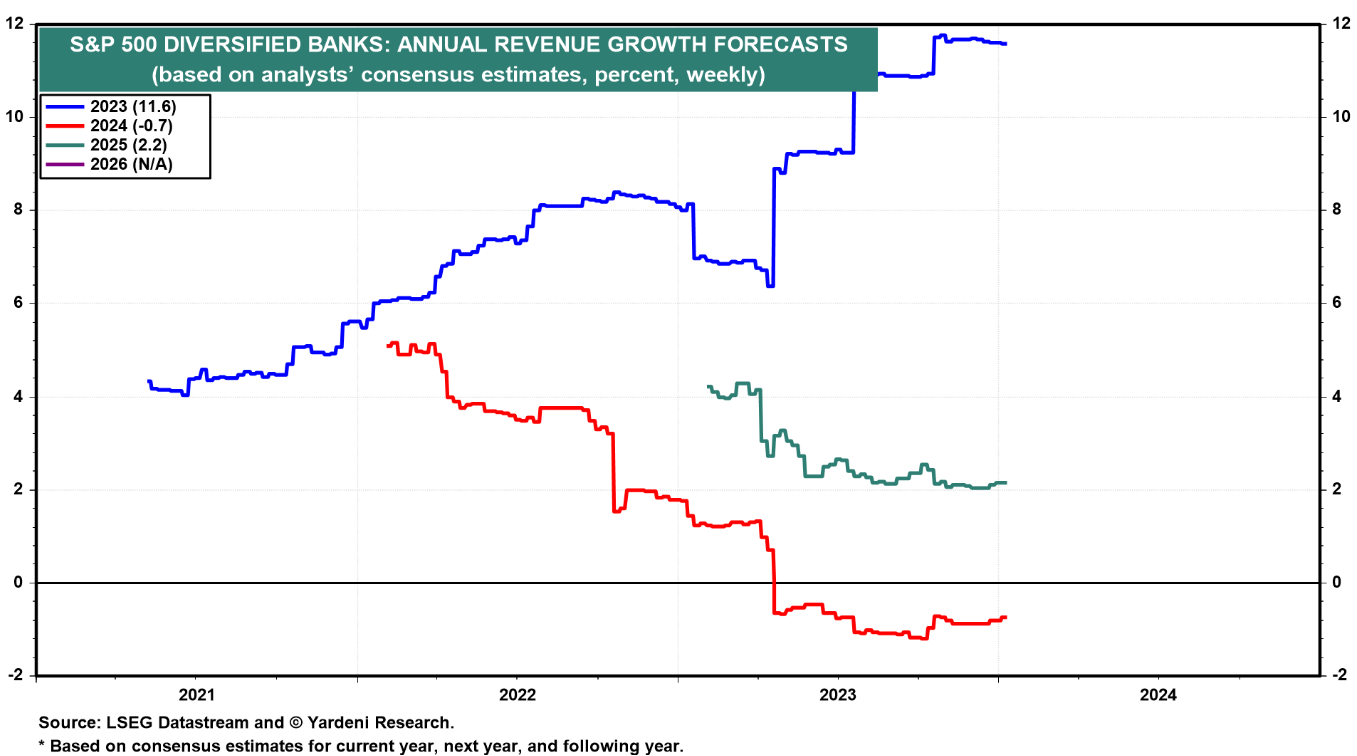

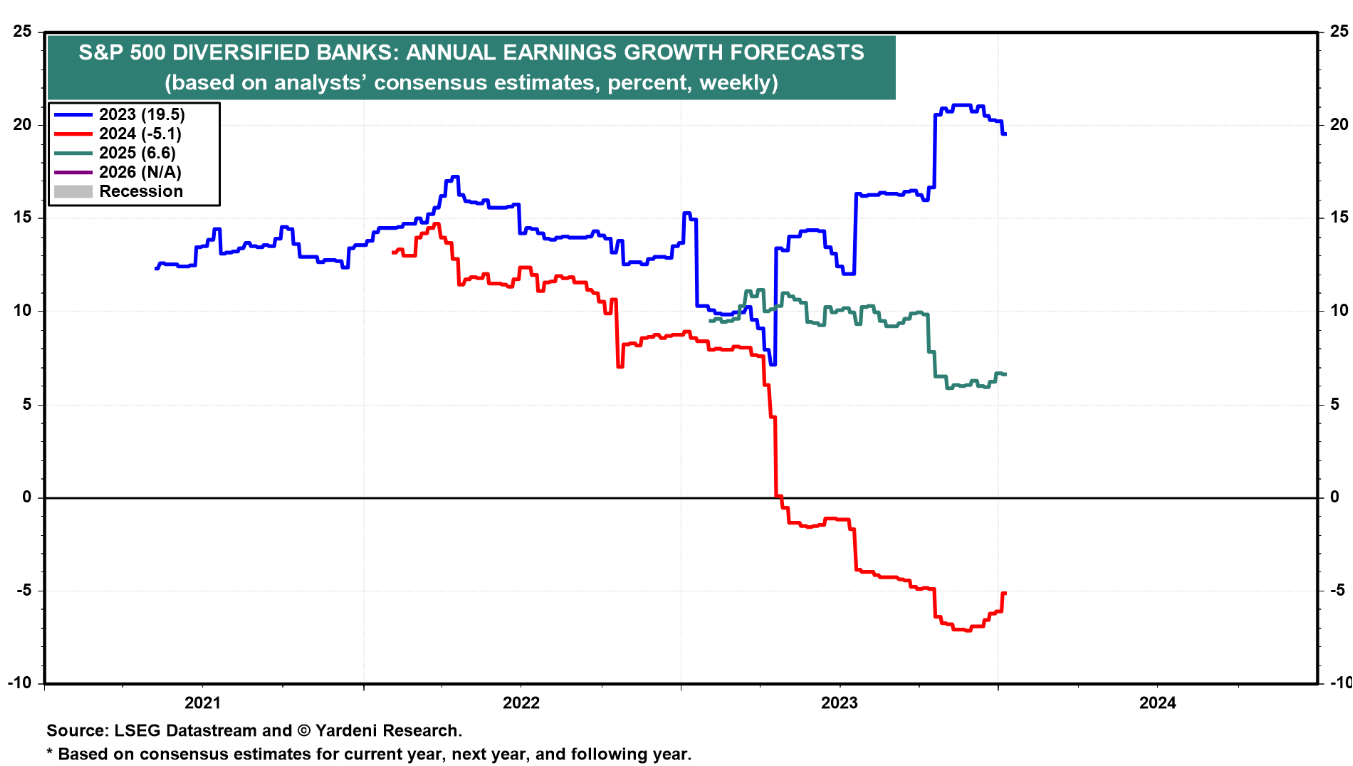

Banks' earnings expectations have come down

Analysts have significantly lowered 2024 revenue and earnings projections for S&P 500 Diversified Banks.

The sector's revenue is expected to decrease by 0.7%, with earnings predicted to fall by 5.1%.

This is the kind of pattern we like to see.

The KRE index went nowhere when 2023 expectations (blue line) were going higher.

As we noted earlier, finding banks that have clean balance sheets, excess deposits, and can hire the lending teams from regional banks will do well.

Also, that 10.5X forward PE? That means the bull market has a lot more room to run. The leadership can broaden.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Digital Assets

The Widowmaker trade, which laid waste to 3AC, Genesis, BlockFi, is over.

There is something to be said for financial engineering and leverage destroying wealth.

A carry trade funded with short term borrowing, and unstable delivery price

There was no need for a government bailout or intervention.

Crypto bottomed on Nov 16th - the day Genesis failed.

Fee disclosures for Spot ETF

BlackRock is bringing distribution.

Capitalism works because it drives lower costs for consumers

Bitcoin traded down in a classic ‘buy the rumor, sell the news’ event. That was the main expectation coming out of the podcast Lumida hosted the week prior.

We believe positioning around an Ethereum ETF is a good move… and we have some other ideas too.

ETH shot up to $2,600 last week. We bought ETHE on Monday for clients when the stock dislocated from a random news headline.

These markets are thinly traded so we’re reluctant to leak each idea on the newsletter.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

On AI

If you are curious about the cutting-edge trends shaping fintech in 2024, you can’t afford to miss our fascinating conversation with industry experts Frank Rotman (CIO at QED Investors, 6x Forbes Midas List), Marc Weill (Senior Advisor at Two Sigma Ventures), and Simon Taylor (Founder of 11:FS).

We dive deep into AI, payment solutions, open & embedded finance, and the evolving roles of cryptocurrency, big tech, and banks.

Tune in and don’t forget to subscribe!

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

On SaaS:

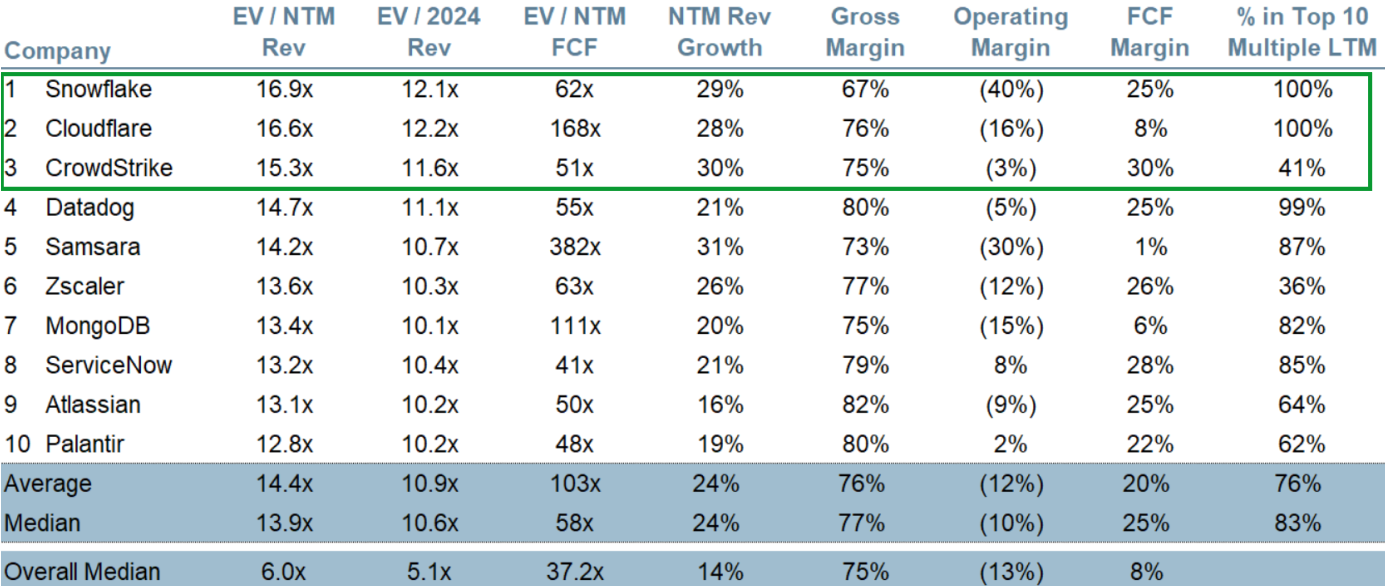

We’re starting to review Altimeter’s Jamin Ball’s weekly SaaS highlights and curate the best takes here.

We believe Altimeter was wrong on their bear case for Google.

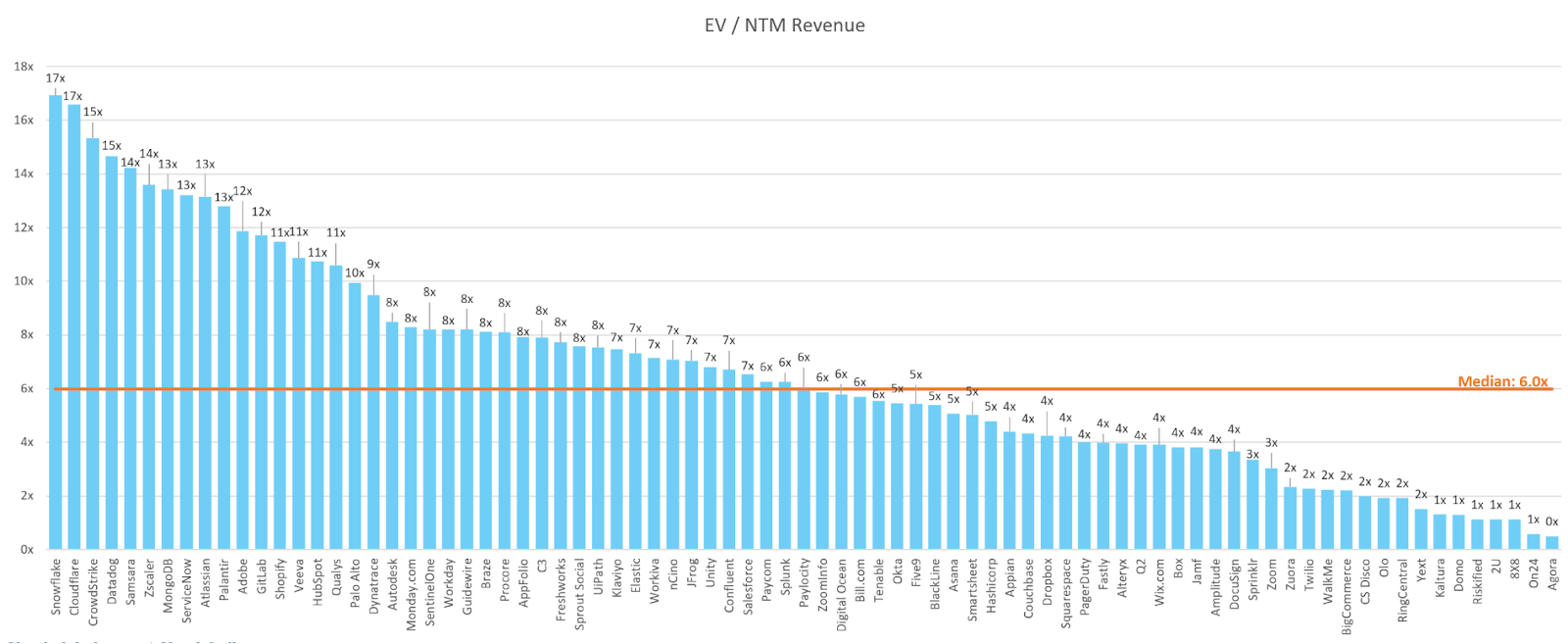

Here is what they like in SaaS: Snowflake, Cloudflare and CrowdStrike based on NTM revenue growth.

Our view… We agree. On all of them. That’s unusual.

We like quite a few names on this list. In fact, I feel like I am looking at my favorite SAAS tech companies list. MongoDB is great. So is TEAM.

Palantir is over-valued and over-rated though - stay away.

The software sub-component of technology was oversold going into last week.

Although at the index level tech is expensive, there are pockets of value inside. This sector was one of them.

Here’s an excerpt from Lumida’s internal-only Factor Chartbook that highlighted this opportunity for us:

Were you buying?

If not, why not? Nasdaq rallied this week.

This is why you need professional money management folks.

Here is a nice chart of Enterprise Value vs. Next 12 Month Revenue:

Fabricated Knowledge calls for Downturn in Automotive Cycle

This resonates with our theme above regarding Tesla and Lucid and Rivian…

Fabricated Knowledge, a leading semiconductor substack, argues the automotive market cycle appears to be turning, with weakening signs already evident.

Industry-wide inventory corrections are expected, with Microchip's guidance cuts potentially setting a precedent.

Other semiconductor companies like Infineon are predicted to lower their guidance soon.

Mobileye's guidance significantly lowered, surprising the market.

What’s On Your Mind: How to Make a Good Decision?

Have you ever second-guessed your choices, wondering if you made the right decision? Join Ram and Justin as they unravel the art of smart decision-making, sharing their invaluable insights, strategies & mental models.

Click to watch on youtube & don’t forget to follow @jguilder on twitter

Quote of the Week

“Be Fearful When Others Are Greedy. Be Greedy When Others are Fearful.” Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.