- Lumida Ledger

- Posts

- Demographics, AI Narrative, Consumer Delinquencies, Crypto

Demographics, AI Narrative, Consumer Delinquencies, Crypto

Justin Guilder & Ram Ahluwalia

January 21, 2024

Welcome back to the Lumida Ledger.

Here’s a preview of what we cover this week:

Macro: Demographics, China Deepdive

Markets: Lumida’s strategy, Back from the Dead Trade, Bumble, S&P return contributions

Company Earnings: DFS, Apple and Tesla, SoFi

AI: Dot Com bubble vs AI 2023, Internet adoption vs AI

Digital Assets: Bitwise discount hit 50%, Ryan Selkis interview

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

A quick poll to understand your reading preferencesWe are experimenting with the length of the newsletter would love your feedback, click to vote. |

Demographics have been running ‘rent free’ in my mind.

This week we sat down with Charles Goodhart and Manoj Pradhan, acclaimed authors of the book "The Great Demographic Reversal."

I strongly encourage you to listen to either the 20 minute ‘summary and takes’ video that Justin and I prepared, or the full 1 hour with authors of The Great Demographic Reversal.

Here are a few key points:

China over the last 30 years has provided a profound production and disinflationary boost to the world. That trend is now over. China’s population is shrinking today. That's the present reality - not a forecast.

Demographics drive all real economic variables.

Fiscal spending will go up due to entitlements. The fastest growing population cohort is the oldest of the oldest. (Long: Wheelchairs).

There is not enough labor to care for the elderly or the young. Labor will start to demand higher wages, and successfully do so.

We’re already seeing that with worker’s strikes and unions (UAW, Writer’s Guild, etc.)

The economic pie will start to shift towards labor away from owners of capital (which have captured the lion’s share of economic growth benefits during China’s ascent)

Inflation will have pressure - both from deficits and Treasury issuance.

Higher inflation will pressure interest rates higher and bond investors demand a higher real return.

So, the Federal Reserve and policymakers are in a bind. There are no easy choices.

The only bail-out is if there is a massive productivity boost from AI. However, AI does not provide services to care for the elderly or the young.

We need ‘blue collar’ AI. We also need nurses and nannies.

We need robots with human empathy and kindness. There are AIs already that have better bedside manner than physicians - but they are not in a physical human like form.

If we can’t get driverless cars to avoid hitting pedestrians, fair to say we are a looooong way from robots providing healthcare services.

How to Position around Demographics impact investing?

Consider that the best performing stock markets in the world are the United States, India, and Mexico.

The worst is China. Europe is in the middle.

Is that a coincidence? Not at all.

In fact, country stock market returns are highly correlated with population growth.

Here are a few themes - we like. We ‘stress test’ our investment themes against this structural shift to make sure we are well positioned.

After all, a great investment you should hold for 10+ years. We need to look outwards.

Biotech

We need investment in treatments for cognitive decline (e.g, Alzheimers and Parkinsons). That’s necessary to extend the productive capacity of the elderly. (Most R&D is going into Cancer & Cardiovascular). Insurance companies and families spend an incredible amount on end-of-life care. That trend won’t stop. Biotech is a beneficiary, AND we are seeing real progress from new modalities in Biotech such as therapeutics and MRNA.

We will be interviewing the founder of one of the most successful biotech hedge funds in the world - RTW - don’t miss that.

We also have a biotech portfolio curated with our network and access to some pretty sharp people in the space.

Nursing Homes & Assisted Living

There are small cap stocks in the United States, and other firms in Japan that are attractively priced and growing earnings at a mid-teens rate.

There are also specialty care providers. For example, firms that provide oxygen delivery systems at home.

Insurance companies will continue to do well. We shared a few ideas on healthcare and the firms we like in that category as well.

Semiconductors

If there’s one theme that we keep going back to again and again - it’s semiconductors.

It’s also a beneficiary of aging demographics. We need greater automation and productivity.

That will come via AI in the next few years, and robotics beyond that.

Semiconductors power that.

No surprise that Nvidia is up ~20% YTD. Nvidia will beat Amazon in market cap.

In 10 years, we accept Mag 7 will contain a number of leading semiconductor firms.

It’s the category we are excited about because market valuations are not yet bananas.

Target High Growth Population Areas

There’s a housing shortage. But where to invest? We like Florida and Texas, which are growing populations and benefiting from retiree movements.

Real estate prices are highly sensitive to population growth.

The difference between 50 bps of population growth and 50 bps of declining growth is the difference between a suburb of Miami and a suburb of Detroit.

We are highly deliberate about where we are investing against our Distressed Commercial Real Estate theme.

Demographics cuts across many of our investment themes.

Travel & Leisure

Cruise lines are nearly fully booked for 2024 already.

Seniors want to travel. Invest in themes linked to travel & tourism.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Macro

Trump vs. China:

Trump's victory in Iowa is sending China to test new lows.

China may be pummeled during the election debates.

We noted on Tuesday that market is only now starting to price that in.

It won't happen over one day. It could be over a few weeks.

If China has a capitulation event, then the risks should be priced in.

That would then be the time to step into the water around China.

How to step into China (e.g., what sectors) is a different question.

The criteria of the answer would be to find the highest quality businesses.

Find the Mercedes. Don't go dumpster diving.

Take a look at this 10-year view on China.

Markets are myopic, and highly event and theme driven. Markets are not perfect discounters, far from it.

That creates opportunity.

China as a country is essentially a giant value stock.

What about declining demographics? This drives where to focus.

Chinese exporters will do well. Don’t forget China is the world’s largest exporter of automobiles and EVs now. Yes, ahead of Japan. There’s no link to local demographics.

However, even the domestic spend story is interesting. China’s savings rate skyrocketed to 50% due to fear and psychology.

That savings rate should decline to historical levels of 30%. That means domestic brands will benefit.

Over a 3 to 5 year time frame, it’s hard to see how high quality Chinese stocks don’t bounce 30 to 70%.

Focus on the highest quality names with good management and competitive advantage.

Now is a good time to establish starter positions.

The narrative is changing.

BlackRock, JP Morgan Asset say China valuations attractive.

Bell Asset is looking to add exposure in Chinese stocks for the first time in decades.

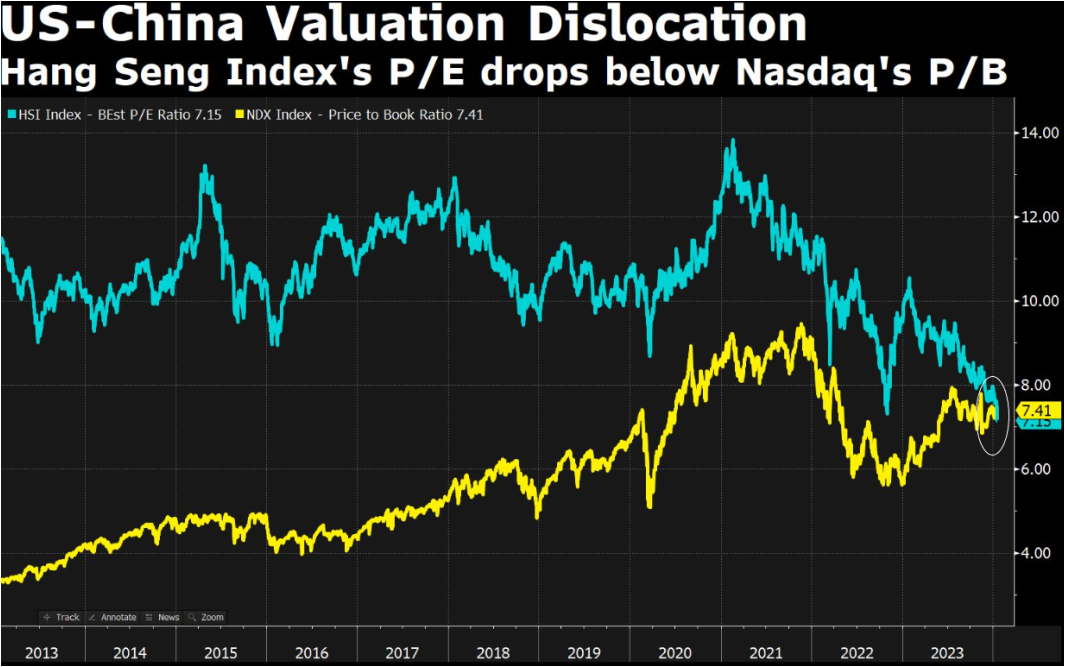

The valuation disparity between Chinese stocks and their U.S. tech counterparts has reached unprecedented levels

The Hang Seng Index’s PE ratio is now below the Nasdaq’s Price-to-Book ratio.

Those two valuation ratios were not even close in the past.

What about the fraud earnings in China? We saw that fear in the United States around Worldcom and Enron. When market confidence is depressed you are compensated for the risk.

Again, stick to the highest quality names - those that are US listed and also are subjecting themselves to US audit.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

There are 3 tells to look for in China:

When property prices stop dropping. The second derivative is positive, meaning the rate of decline is slowing. Markets anticipate, so you can’t wait for the perfect all clear.

A capitulation moment. That’s a waterfall decline in stock prices, which we see every couple of years. We are seeing some capitulation here and there. But there is a lot of sidelined money wanting to buy the dip every time.

What about Geopolitical risk?

China sent more delegates to Davos than any nation, including the United States. China’s premier ‘bent the knee’ in San Francisco.

Wars are unpopular. Youth unemployment is high. Disillusionment is high.

We’ve had a number of podcast interviews on Lumida’s Non-Consensus Investing discussing China with portfolio managers and consumer trends analysts.

The bear case on China isn’t China itself. It’s the opportunity cost of capital

India’s stock market is near ATH. Mexico’s is as well. Those markets have momentum and are benefitting from friend-shoring.

The question is which markets will do best?

We believe the answer is in breaking the problem down to the asset level - look thru the country.

For example, we own ASML which is based in Denmark - even though Europe is in the dumps.

It’s a great asset.

Non-Consensus Macro:

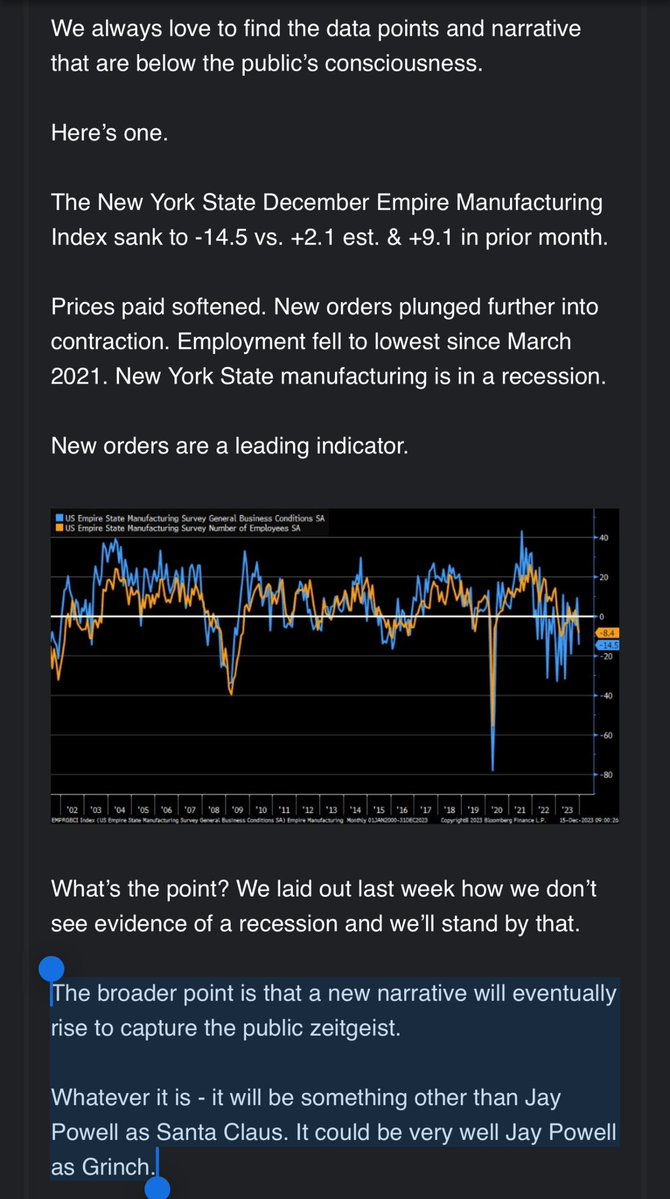

The New York Empire Index, a measure of manufacturing, broke its back last week.

The Empire index was awful last month also…but it went unnoticed by Mr. Market.

Background narratives are always lurking and waiting to take center stage.

Recall this excerpt from the Lumida Ledger last month:

Narratives only take hold during certain climates.

The Zeitgeist last month was ‘up only’ and Fed Pivot.

The bad news did not fit the narrative.

It was subconsciously ignored.

This month sentiment is weakening as markets are shakier.

So the amygdala highlights weaker data.

This is just Confirmation Bias in action.

Empire Index went from ‘background note’ to ‘foreground chord’.

That bad news helped to re-build a ‘wall of worry’.

We didn’t have that during the Goldilocks talk at the end of the year.

Markets

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

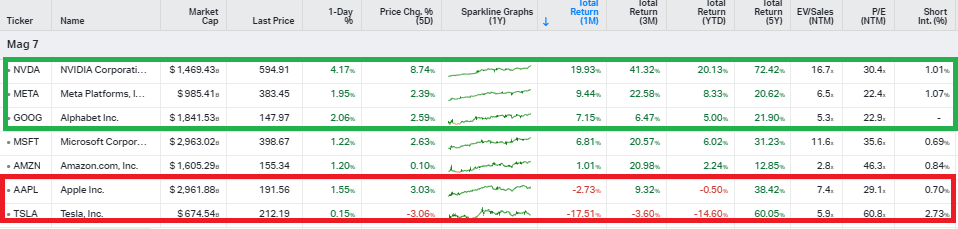

How do we feel about markets now?

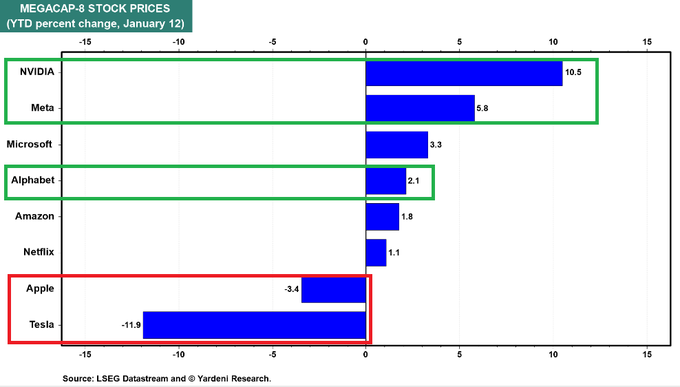

We have a nuanced positioning - we aim to sector match our holdings to the Mag 7 weight.

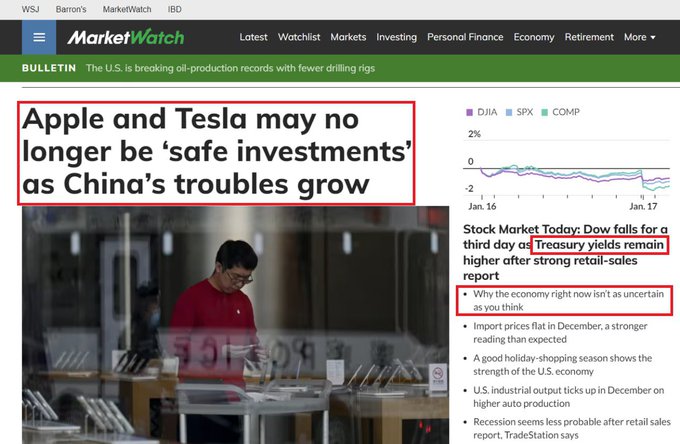

But, we own Google, Meta, and Nvidia and not the rest. (In fact, we shorted Apple and Tesla at the start of the year - but have covered.)

What’s working YTD?

Take a look at this table

Best: Google, Meta, Nvidia

Worst: Apple, Tesla

Middle: Amazon, Microsoft

Funny, those correspond to our Overweights, Shorts, and Neutral positions.

We’ve been writing about these ideas for months now.

Microsoft is a great firm… It’s just Consensus. So, you get the Consensus return.

Amazon - we just want to own the AWS business. Not the grocery chain or the logistics operation. It’s a middle of the pack idea, and it’s a bit pricey.

We’d rather stick to where we have conviction.

But, you do want to own other names outside of Mag 7 so you can get a Non-Consensus return.

We are scooping up ‘Left for Dead’ SPACs that have real businesses.

In 2021, there were many awful businesses like SoFi that went to the public markets.

But, there were also good companies whose valuations have crashed.

One example - Bumble - the dating app. (Dating apps are a great market - look at IAC…).

Bumble is cheap, and the fundamentals look attractive (no pun intended.)

Bumble has an 11.7x forward PE. Analysts expect 17% revenue growth next year and $160 MM in free cashflow on a $2.6 Bn market cap.

Bumble is under-owned and ‘left for dead’.

Similar to how Crypto was ‘left for dead’...and then put in a face-melting return.

Bumble is a brand that is out-of-favor simply because it is a SPAC. It doesn’t have the traditional analyst coverage machine.

Bumble is highly volatile and it’s trending down. So you want to be thoughtful around how you approach this.

We have found about 5 other businesses fitting this ‘left for dead’ theme that we are investing in. I will be disappointed if we do not get a 30 to 50% return this year on them, although I expect there will be a 20% drawdown on the way.

Market Compass

Let’s cycle through our three-prong market compass as we look to the week ahead.

1. The 10 year bond yield closes out the week at 4.1%, up 18 bps over the week.

When the Ten-Year increases, that hurts valuations for long duration stocks.

Biotech stocks were out-of-favor this week, as well as ‘unprofitable tech’ including miners and Coinbase.

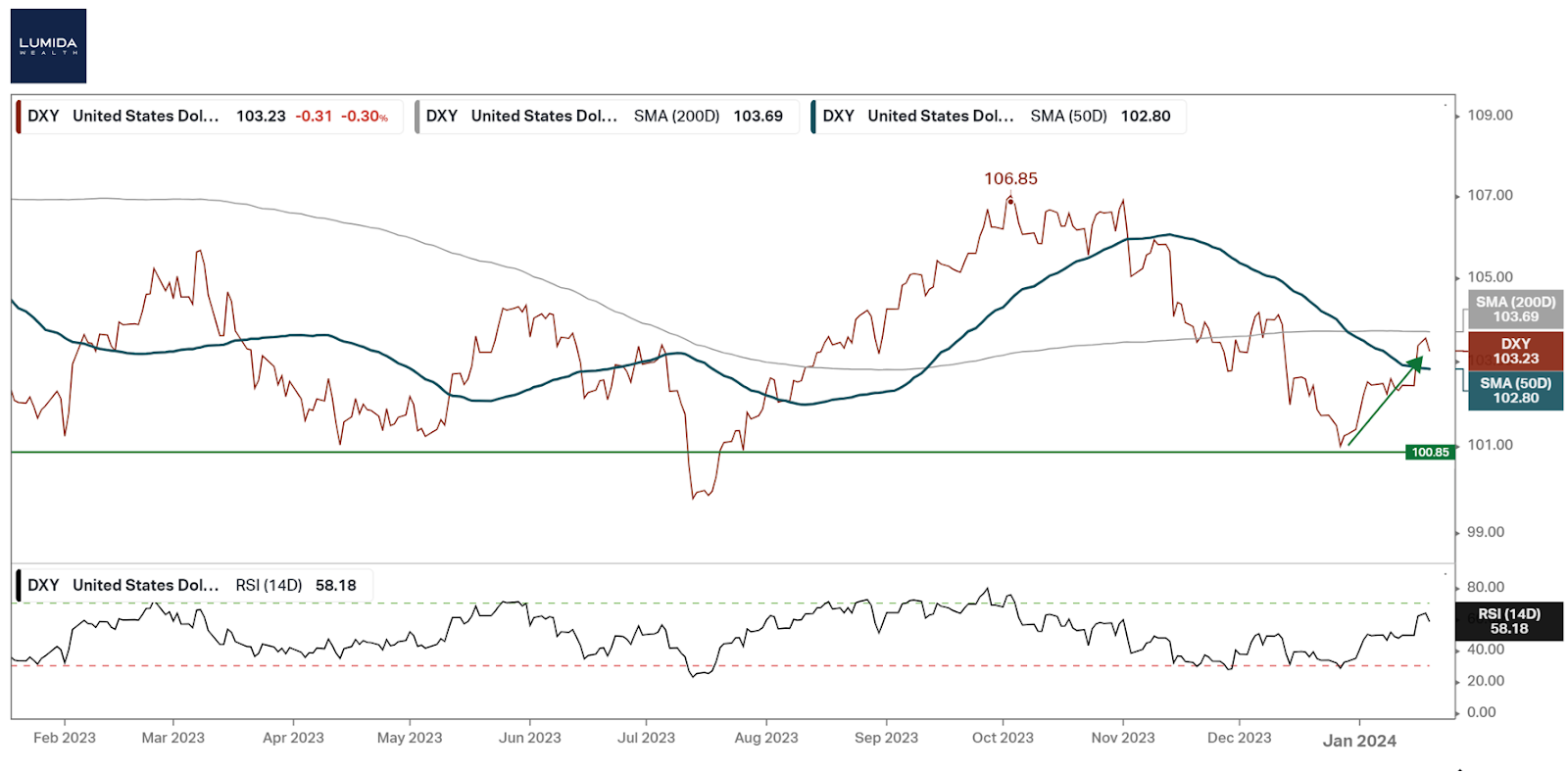

2. The US Dollar is turning up (Up by 1.8% MTD)

When the USD increases in values, US equities decrease in value.

The ‘top is in’ on the dollar. You can see that it took place in October ‘23. Over the medium term, that’s bullish.

3. Semiconductors are up.

Semiconductors are an expression of AI narrative.

That's headed up by ~8% in the past week.

SMH, the semiconductor index, is above the 50 day and 200 day moving average.

We don’t believe now is the time to chase semiconductors. We bought more Nvidia for our clients at the beginning of the year. It’s rallied sharply - as has AMD.

We believe AMD is overbought and expectations are running too high going into earnings season.

We prefer Nvidia - it has a competitive edge due to the Cuda Moat. We have discussed this on prior Lumida Non-Consensus Investing podcast interviews with Dylan Patel (Semi Analysis) and the CEO of Groq.

We wrote about healthcare a few weeks ago and how we like that.

Guess what? Healthcare is overbought now (see XLV below). Part of that is driven by the GLP narrative. Eli Lilly is the leading component of XLV.

Now is not the time to chase healthcare.

Further, with tech bouncing there we believe there will be less interest in owning defensives like healthcare.

Focus on what Mr. Market is offering on sale, and gradually you will have a quality portfolio.

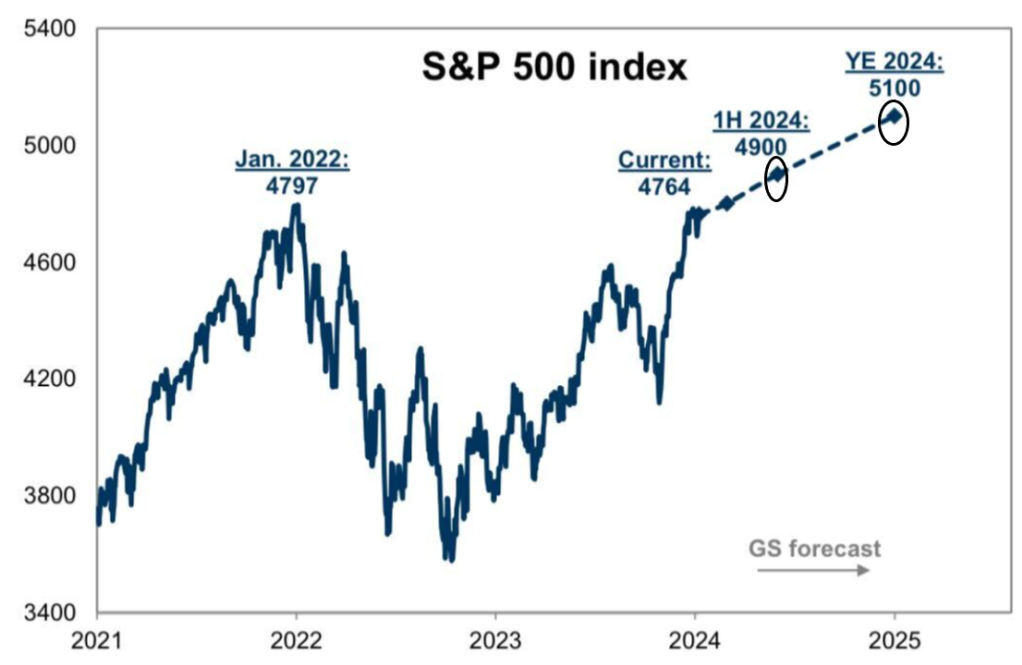

Markets: S&P 500 index path to 5100 at year end 2024

Goldman Sachs predicts the S&P 500 to rise to 4900 by mid-year. 5100 by year end.

Year-end projection anticipates a 7% increase from the current level.

All I can say is Mr. Market will do something completely different than what Goldman forecasts.

Expect a lot more volatility for starters - especially as risk assets start to discount no rate cuts in March.

Probabilities declined to 60% at the lows this week.

I can tell you exactly when markets will price this in.

The day Goldman’s Chief Economist Jan Haziatus changes his view on rate cuts. Jan is an excellent economist (they are a rare breed). He is steadfastly clinging to the idea that we will see rate cuts in March…

But in his research notes he is tracking the commentary from Governors in their weekly speeches - all of whom are saying ‘higher for longer’.

We believe Jan has his clients in a pickle. He’s giving them a few weeks to get out of these losing positions.

Then he’ll revise his rate call.

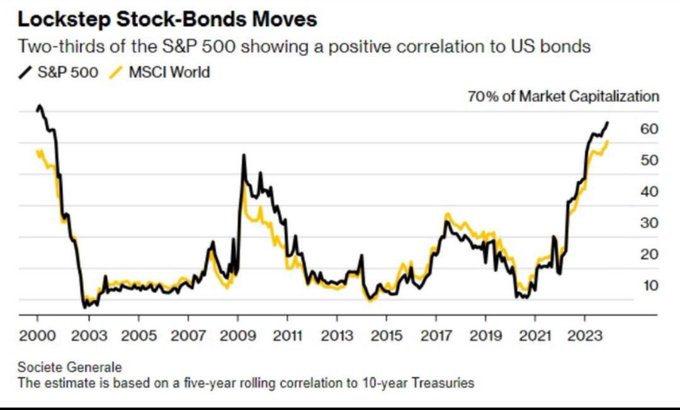

Markets: Bonds Remain Positively Correlated to Stocks

‘2/3 of the S&P is positively correlated to bonds’

Where is the diversification?

Why own a 30-year government bond?

The loose out to inflation?

60/40 stock/bond portfolio mix may be outdated.

Lumida Wealth is going to disrupt the legacy wealth management complex.

I struggle very much to understand why anyone owns a 10-year or 30-year Treasury bond.

Go buy Barclays or Citibank stock instead. You’ll get a dividend, and it will increase over time. And it’s an inflation hedge.

How is Lumida Wealth doing this year?

We're beating the S&P handily.

This chart is one reason why, and our Overweights on small caps and biotech.

We also made money shorting Apple, Tesla, and SoFi as well.

Morgan Stanley put out a $400 price target on Tesla.

Thank you Goldman and Morgan Stanley for your conflicts of interest and uncritical research.

We are off to a great start.

Fun Fact: Most of Lumida's clients are former clients of Goldman, JP Morgan, and Morgan Stanley (in that order)

This chart is beautiful. It summarizes what we like and we don’t like, and we’re pleased that our deep research is paying off.

On SoFi

We have successfully called shorts on SoFi 3x. It’s all documented on X.

And we get a lot of pushback from ‘SoFi bros’ who think SoFi is a next generation financial institution.

We think SoFi is a bank sitting on a pile of credit risk that likely should be marked below par value.

Also, we have observed social media farms with NPC accounts pumping SoFi stock - like @sofi007girl. These are not real people. We’ve tried to make contact with them.

When you message them it’s like getting a phone call from a ‘Canadian Online Pharmacy’ powered by a call center in India.

SoFi or an affiliate, I allege, is influencing social media to prop its stock price. I can’t be sure who is financing it, but this doesn’t help the integrity of our capital markets.

Take a look at this tweet from @sofi007 girl. There are dozens of accounts like this.

This is not a ‘cult’ account. These are NPCs with zero personality and their full-time job is pushing products and stocks.

In any case, we’ve made our investors 20 to 30% shorting SoFi stock.

If the bull case is a bunch of fake accounts, and they are marking up the fair value of their loan book despite an increased delinquency rate…well, that call was pretty easy to make in hindsight.

That red line is when we initiated our position.

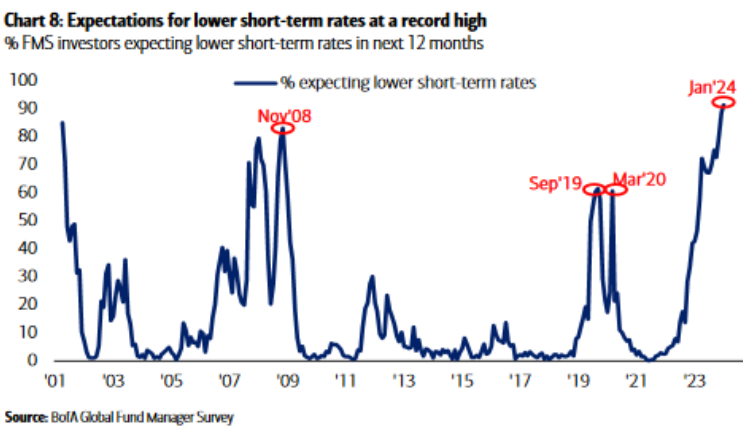

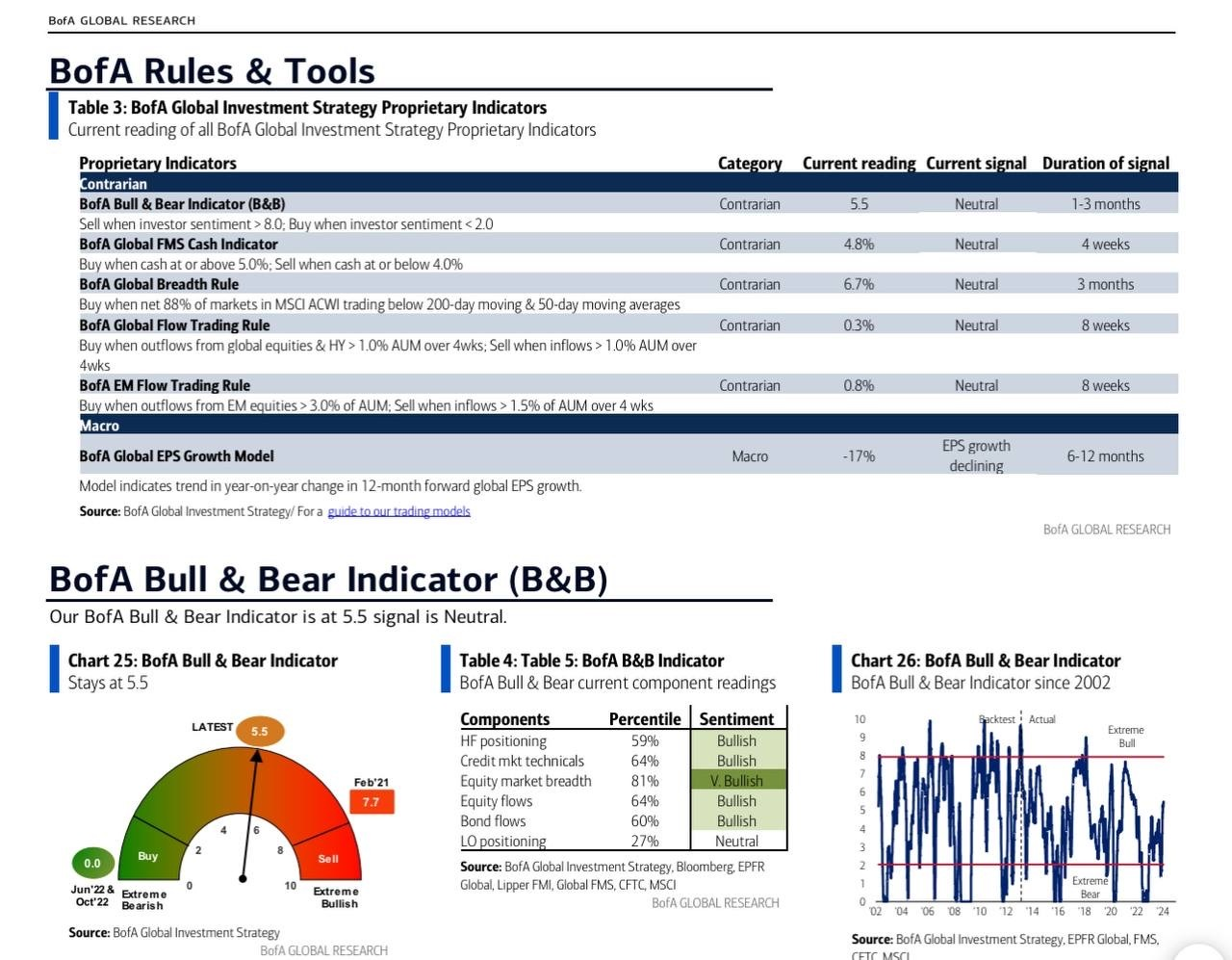

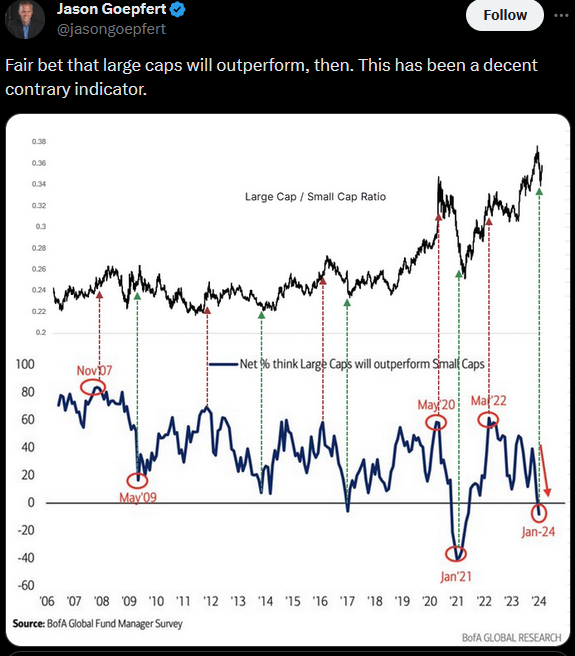

Bank of America Global Fund Manager Survey result - January 2024 result:

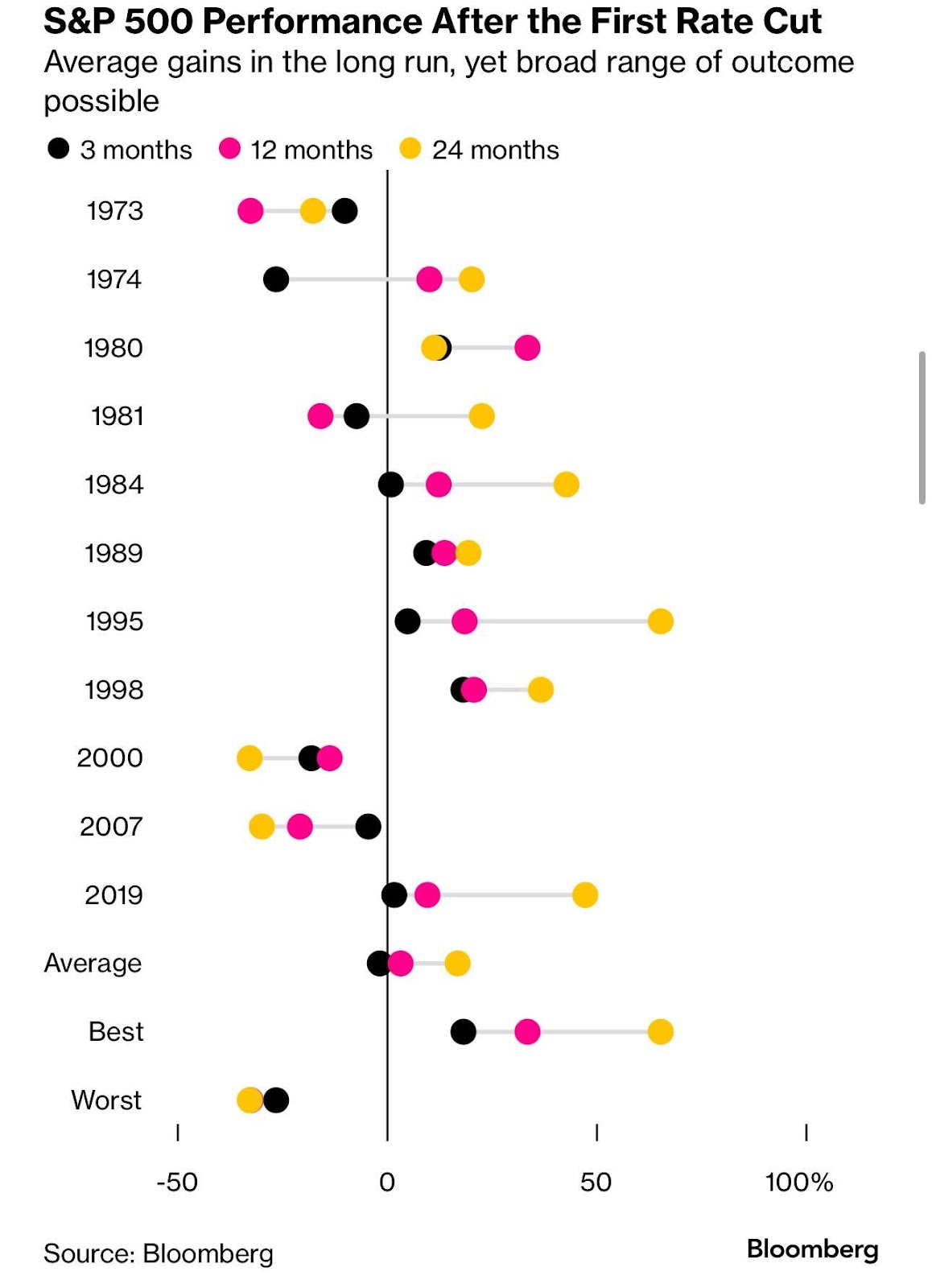

How does the S&P Perform after First Rate Cut?

Here’s a nice chart.

The summary - it depends on why there are rate cuts.

If rate cuts are due to economic weakness (such as 2007 or 2000), then equities get slammed.

We should not see Consumer Sentiment spiked higher this month.

Initial jobless claims are at a decade low.

All recessions are fundamentally about employment.

Labor shortage issues are receding.

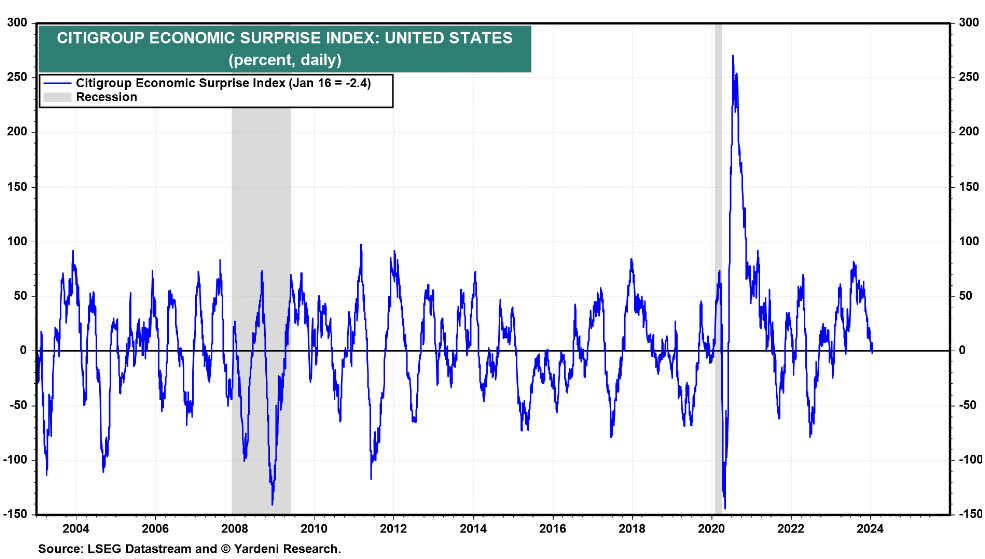

The fly in the ointment is that the Citigroup Economic Surprise index is now back to zero.

That means the narrative of the US outperforming expectations will fade.

So, the driver of US equity returns will shift from multiple expansion to earnings growth (and whether they are above or below consensus.)

Here is the Citigroup Economic Surprise index.

Generally this index oscillates around the zero line.

So there’s a good chance we’ll see disappointing economic results.

That will create volatility and buying opportunities.

How do we feel about Markets?

These markets are incredibly dynamic. On Wednesday, we thought markets were oversold. So we covered and bought Thursday morning.

Now they are back to overbought after two strong back-to-back days.

There are sectors we like - including software & semis - but you really need to pick your spots.

Semis are getting bid up quickly now. We’d rather not that be the case. We have conviction - we want to buy these when they are cheap.

We saw this chart and it does a good job of illustrating our view on markets - Neutral.

Very ‘Meh’. No reason to short anything, not much reason to buy anything.

Earnings Season

The opportunities will be during Earnings Season.

If we’ve done our job picking good themes and stocks, they should do well.

We expect high quality companies to see their stocks drop 5%+ after they report. We will be buying them when that happens.

Last quarter: Google, Palo Alto Networks, Z Scale all dropped 8% on the date they released earnings in the after-market. Now all of them are at all time highs.

If you want to get into tech - we suggest waiting for this opportunity.

You need to know what you want to buy in advance.

The bullish catalyst is AI narrative - that means Big Tech earnings.

Tesla and Apple report on 1/24 and 1/25.

The leaders - Microsoft, Meta, and Google - report 1/31 and 2/1 - right after the Fed.

We’ll have to re-assess as we get closer.

A delay in Fed cuts should spill cold water on Financials, Small Caps, and Biotech.

This does not strike us as a ‘runaway’ market - because the markets are still pricing in Fed rate cut delays.

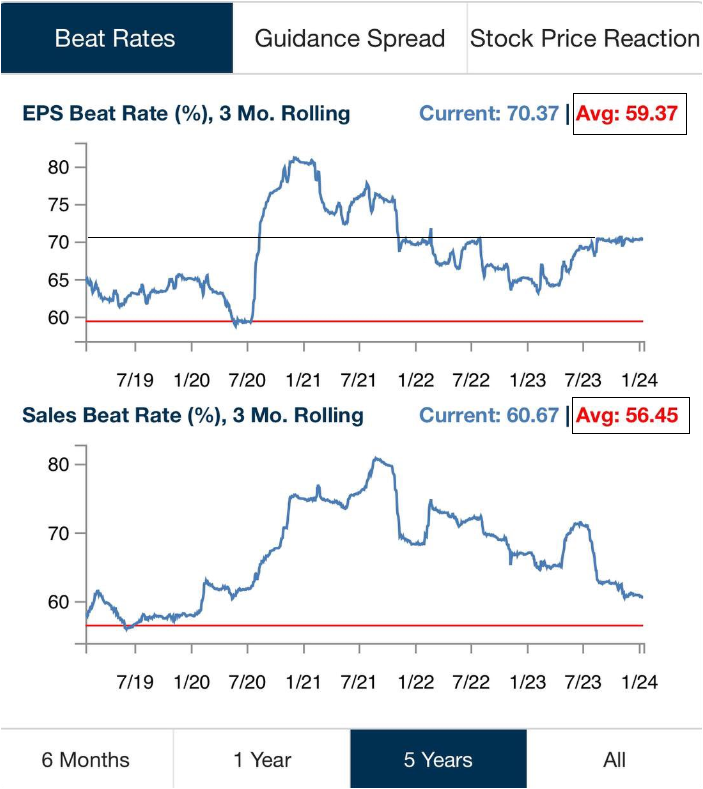

Revenue beat trends are slowing

Earnings and revenue beats are highly managed. They don’t mean too much these days.

But, take a look at the declining sales beat rate. That’s a sign of softening revenue.

This rhymes with the Citigroup Economic surprise index.

So, we’re going to see more volatility in earnings this quarter.

2023 was a great year because recession was Consensus.

This year could have a bit of an oscillation between 2022 and 2023 vibes - Jekyll and Hyde.

Mr. Market will throw off enough data points to give everyone Confirmation Bias - causing them to make the worst decision at the worst time.

A good general idea is to fade extremes. When people expect Goldilocks, get skeptical - like we did on January 2nd.

When people expect recession or bad news hits (like the Empire Index), get more bullish. That’s the wall of worry.

So far we’ve been surfing alongside Mr. Market nicely with this Non-Consensus approach.

Stop trying to figure out ‘Who is right - Goldman vs. Bridgewater’ instead fade extreme Consensus views.

Be Thankful when Someone Hates Your Stock

Altimeter took a sledgehammer to Google on the ‘OpenAI is the Death of Search’ thesis.

That caused Google to lag other Mag 7 the first half of last year.

It was overdone. We at Lumida Wealth started buying. ‘We love Google’ at these prices.

Thank you @altcap I did not attack Altimeter personally. On the contrary, they gave us a gift.

Now Google is near ATHs.

I would never have been able to accumulate Google at low prices without Altimeter advancing this narrative.

Now that narrative is fully discounted.

As long as you are a net saver, you should welcome lower prices and bear markets

Your goal is to accumulate the best assets at the lowest prices and hold for as long as you can.

You sell (gradually) at retirement. At retirement, you want to sell at inflated (preferably bubble like) valuations.

If you are not drawing down against your investments, and putting more capital into investments each year, you should relish bear markets.

This is why Warren Buffett says: ‘Whether we’re talking about socks or stocks, I like buying quality merchandise when it is marked down.’

The world, in aggregate, is a net investor.

There are tens of billions of programmatic buying from pensions and endowments saving for your retirement.

Lower entry investment prices means they have a higher chance of success.

The only ‘losers’ are short-term traders speculating on the long side.

That’s a zero sum game.

True investors welcome lower prices.

tl;dr SoFi investors should not complain about my view on that stock.

You get to accumulate more at lower prices

It pays to be contrarian

We saw this headline and wrote the following on X:

“1/2: ‘TSLA today? $248, and I expect it heads down this month.’

1/17: TSLA is now at $215 (down 15%).

Fear was palpable.

Now we monetize our hedges and sacrifice another pizza to the market gods.”

Truth be told, we use a number of analytics… We saw a spike in the put/call ratio (e.g., fear).

So we covered our shorts on Apple and Tesla and wrote ‘we expect a technical bounce’.

On Thursday morning we bought Cloudflare and some other tech stocks.

Apple bounced back. Here’s how we handled Apple.

It pays to be contrarian.

The time to exit Apple was shortly after the hype around the Vision Pro when the stock rallied way ahead of expectations despite declining YOY revenue growth.

There’s really nothing to do now with Apple. It is ‘neutral’.

Mr. Market gave us a good ‘hand’ to hedge tech stocks on January 2nd and we took advantage of that.

Incidentally, here is where we bought Cloudflare (NET) after our ‘we are due for a bounce’.

It takes a lot of patience and discipline to get those entries. It’s up 5%+ already.

We are scanning dozens of stocks on our ‘Conviction List’ to find these. There were other names we like that just did not present the same way Cloudflare did.

We also bought Haliburton (HAL). Hal is a leading energy company with a 10.4 forward PE and a 20% earnings growth expectation.

This entry was lovely - take a look:

This illustrates our approach to technical analysis. It’s the last step not the first step. Our top-down thematic and fundamental research tells us where to focus and what to buy.

Then we ‘stalk’ and wait for a good entry. Could HAL fall from there? Perhaps, although it is up a few points.

All we can do is make the best decision possible, and we like that decision.

On Dave

SoFi is down 20% over the last 10 days.

Meanwhile, another FinTech - Dave - is up 20% over the exact same timeframe.

Dave is up 136% over the last 3 months.

Dave is part of my "Return of the Living Dead" theme.

Dave was a SPAC. SPACs were left for dead. They are hated and under-owned...but some of them have real businesses.

Why own SoFi, when you can own Dave?

Compare the metrics.

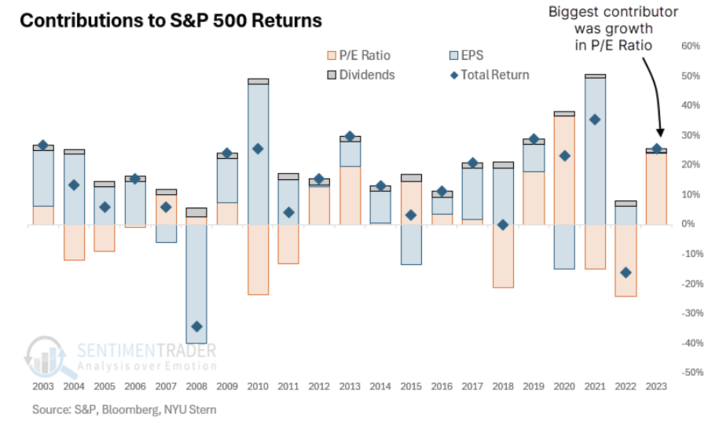

What happens when multiple expansion causes prices to go up?

The rise in a stock (or index) can be due to three primary factors:

1) An increase in earnings per share,

2) An increase in the valuation investors place on those earnings, and

3) Dividends.

Almost all of the S&P 500's returns last year were due to #2, an increase in the valuation investors were willing to put on earnings.

Very little of it was driven by an increase in actual earnings per share or dividends.

Dividends are almost never the primary driver.

We expect the S&P 500 to rise in the current year, driven by the combined impact of EPS and P/E.

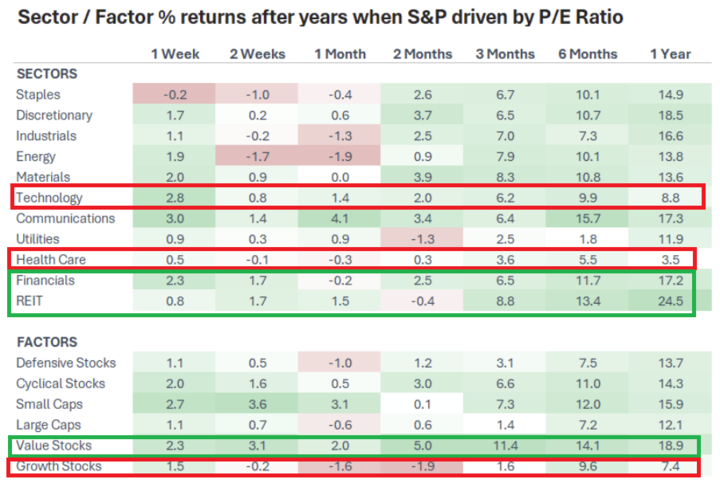

Value stocks outperform growth stocks when S&P is driven by P/E.

Historic 1 year return for value stocks is 19% vs 7.4% for growth stocks.

Real estate outperforms other sectors in the P/E driven market.

Bank of America FMS indicates large caps are likely to underperform small caps stocks.

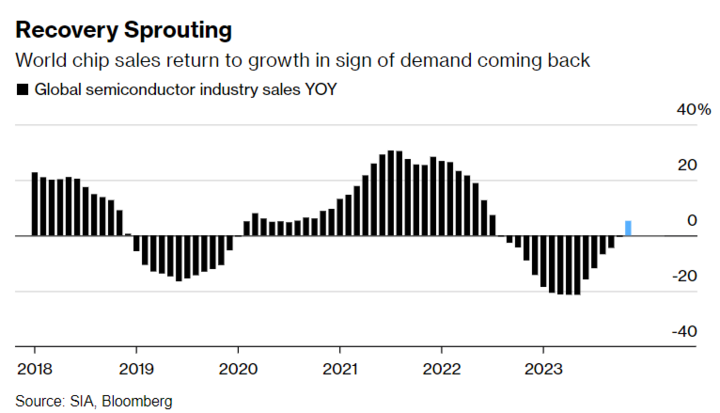

Semiconductors - Recovery trend

Semiconductor sales growth YoY have entered a growth phase again.

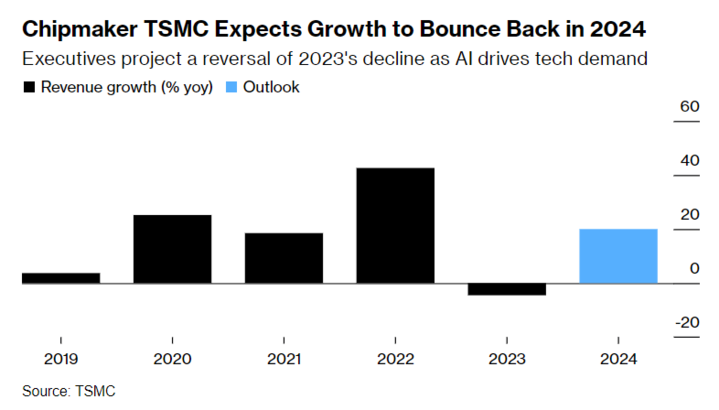

Taiwan Semiconductor expects a return to solid growth this quarter. They see a recovery in smartphone and computing demand.

The stock rallied massively, creating a bid for semiconductors.

TSM is moving ahead with plans for chipmaking plants in Japan, Arizona and Germany — the first of which will begin mass production at the end of 2024 in a big boost to TSMC’s global footprint.

Note: Japan and Europe have their own version of the CHIPS Act. Governments are financing the CapEx of Foundries to diversify China risk. That’s a big deal.

And governments are setting up AI Data centers on their own soil. These are big trends with big customers.

Do you see why we like semiconductors?

You can’t get a better customer than governments and military have a #1 priority to win the AI race.

Front run them.

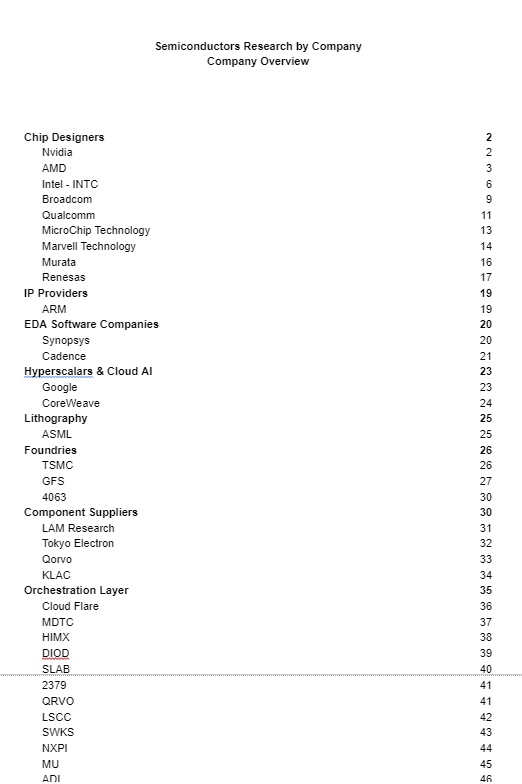

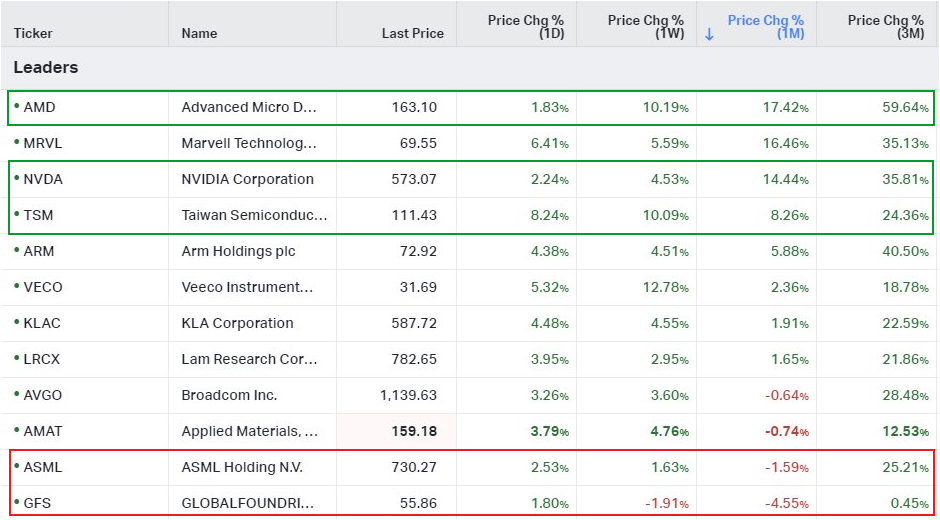

Here's a tracker of names we study closely in semiconductor space.

Also, attached a screenshot of our internal google doc showing our research in this category.

Does your wealth manager have this depth of research on a single category?

Lesson: Be Prepared

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Company Earnings

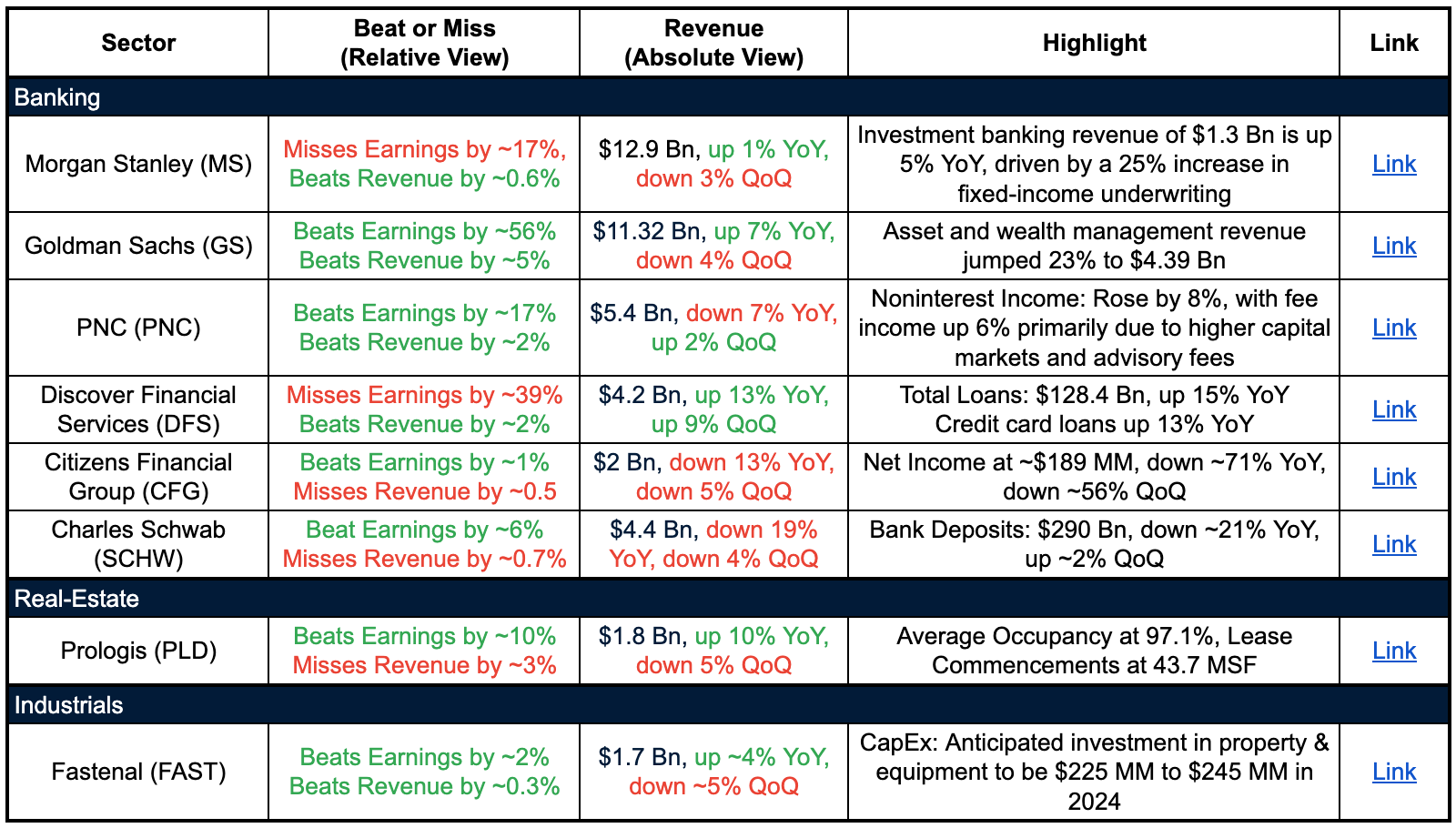

DFS

Discovery Financial Services (DFS) is a name we like to keep an eye on during the earnings season because it offers a very clear snapshot of middle-income consumer balance sheets.

Loans were higher than expected.

Net interest margins were slightly lower than expected while provisions were 17% above estimates fueling a 39% adjusted EPS miss.

The guidance was not much better: with 2024 loan growth expected “relatively flat” and net interest margins sliding to a 10.5%-10.8% range.

The company expects a 4.9% to 5.3% net charge-off rate.

2023 charge-offs hit a 10+ year high at 342 bps, so clearly borrower performance was very weak.

That’s not a good story for other consumer lenders

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

AI

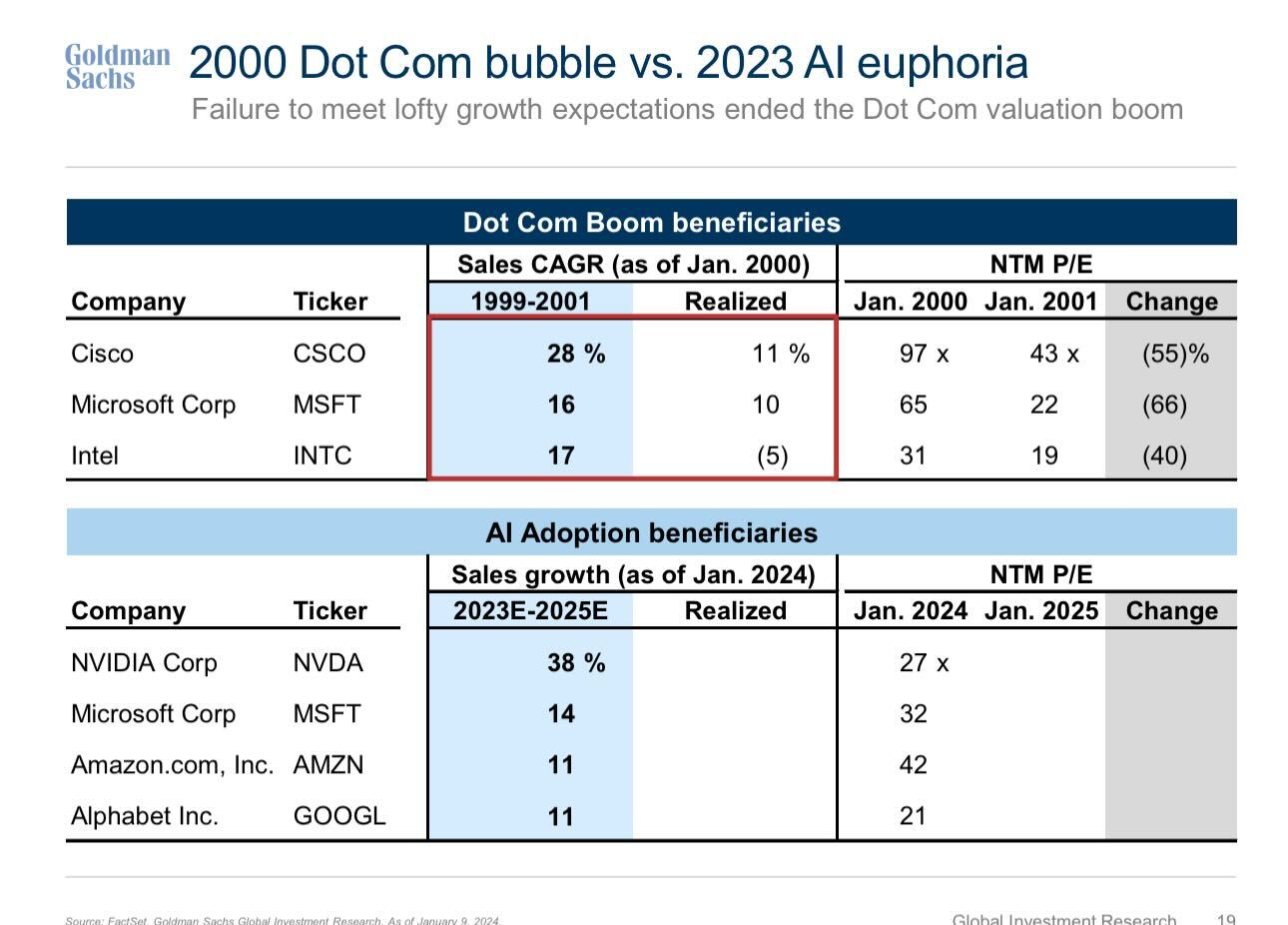

AI Will be the Mother of All Bubbles, But Stay Long, Room to Run

The P/E ratios for the AI period seem lower and more conservative compared to the Dot Com era, reflecting perhaps a more realistic market valuation.

Failure to meet the lofty growth expectations ended the Dot Com valuation boom in the past.

The tell will be when retail investors have sold Apple and Tesla stock and are embracing Nvidia

You’ll also see ‘new economy’ valuations.

Then we’ll want to rotate away from this powerful secular story.

AI is the primary theme driving the outperformance of US equity markets.

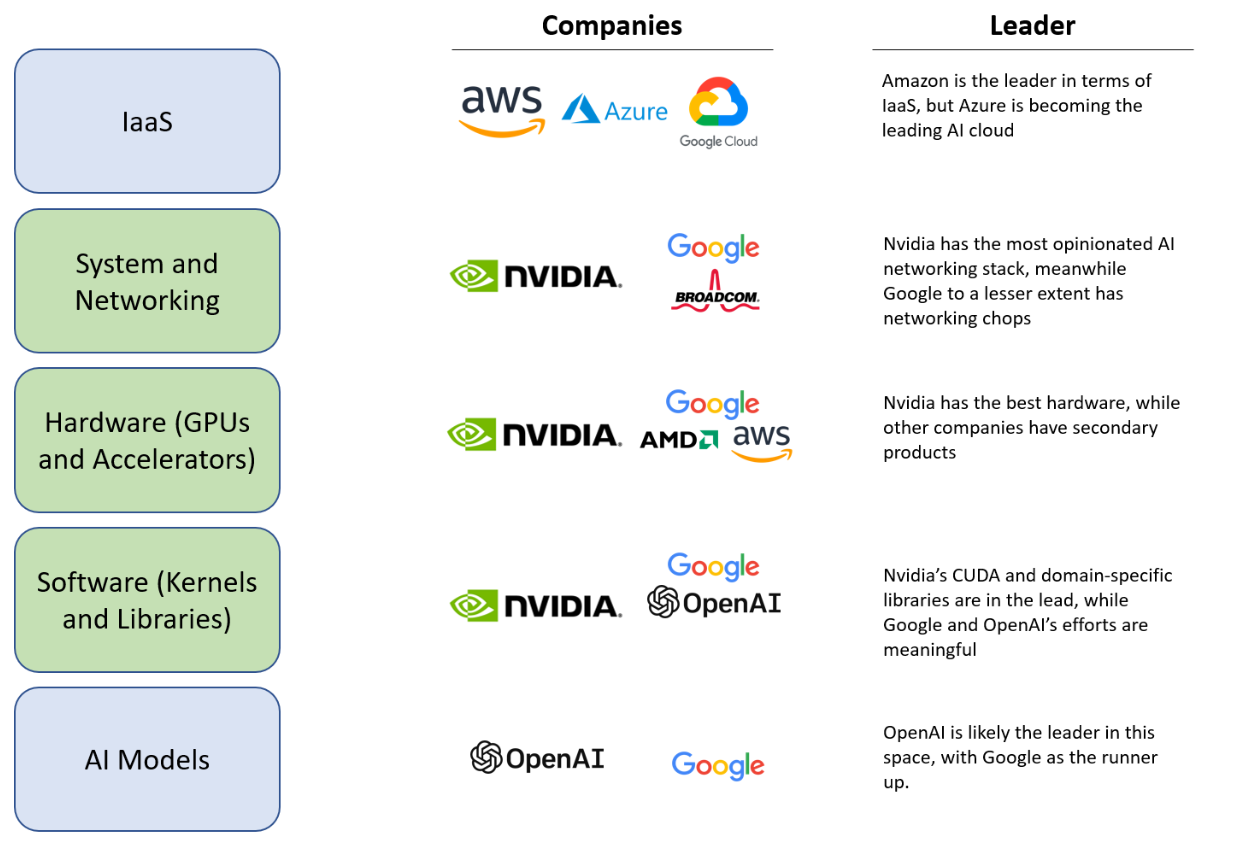

Fabricate Knowledge - Internet adoption vs AI

The internet took 27 years to achieve approximately 70% global penetration, suggesting AI is still in its early stages.

The AI industry is at a crossroads, with its future business model being actively defined by competition between companies like Nvidia and big tech infrastructure providers.

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Digital Assets

This week we had an interesting conversation with Ryan Selkis, CEO Messari.

Tune in to the episode to learn about the trends shaping the world of digital assets in 2024.

Ram also takes a stab at guessing Ryan’s digital asset holdings and comes ‘shockingly close’.

We’re grateful to count on Ryan as a friend and investor in Lumida Wealth.

We appreciate his leadership in holding the SEC accountable as well, and for building a first-rate analytics company for the Digital Asset space.

We discussed:

- Policy & Politics

- ETFs

- Bitcoin, Ethereum, Solana

- AI & Crypto

- Crypto

The move this week?

Buy BITW which had a 50% discount to NAV.

Did you buy?

If you’re interested in learning more about Lumida’s wealth management services, click to join our waitlist

Quote of the Week

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” – Philip Fisher.

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.