- Lumida Ledger

- Posts

- Buildup to Elections: No Recession In Sight

Buildup to Elections: No Recession In Sight

Justin Guilder & Ram Ahluwalia

December 10, 2023

Welcome back to the Lumida Ledger.

Here’s a preview of what we’ll cover this week:

Macro: Surging Productivity - No Recession In Sight

Markets: Election year, Oil, AI & Small Caps

Company Earnings: Legacy Brands In Decline

Distressed Investing: Markdowns, Valuations & Secondaries

Digital Assets: ETH, ETHE & Solana

This week, we spoke with Dr. Tyler Cooper, who is the CEO of the famous Cooper Clinic, which his father Dr. Kenneth Cooper opened in 1970. Dr. Kenneth Cooper coined the term ‘Aerobics’ and wrote the foundational book on it.

Working with NASA during the Apollo lunar missions, Dr Kenneth Cooper, an Air Force Lt. Colonel, was tasked with a critical challenge: counteracting the effects of long-term exposure to zero gravity on astronauts. This journey led to the birth of Aerobics, which revolutionized our understanding of fitness and health.

An essential episode for those keen on diving into the fascinating realm of expanding both health and lifespan.

Click to tune in to your favorite channel.

For our readers seeking insights into the trends influencing markets, macroeconomics, startups, and digital assets, don't miss out on the Non-Consensus Investing Podcast, now available in audio format.

Tune in for a deep dive into contrarian perspectives on investing.

Macro

Our friends at Richard Bernstein lay out the case that there’s no recession in sight.

We agree.

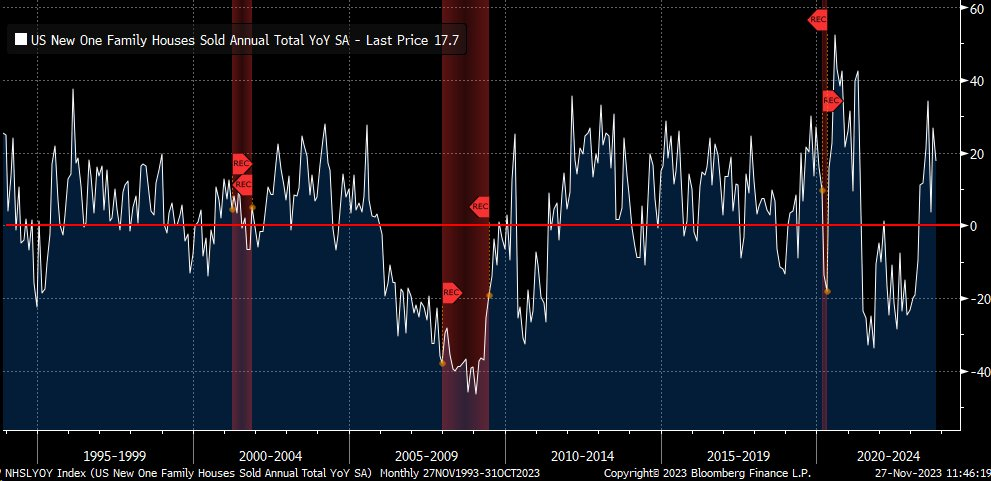

New Home Sales are up +18% YOY.

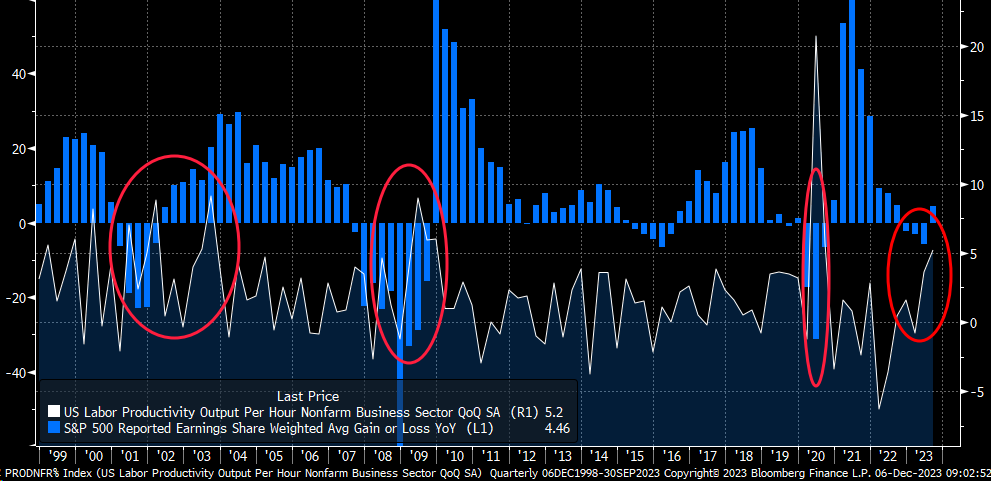

Productivity is surging. Surges in productivity typically are signs of the early stages of a profits expansion. That suggests we have a trough in profits.

Consensus remains the economy is in perilous shape now grown for 5 weeks in a row.

The growth is small, but we haven’t seen 5 consecutive weeks of mortgage growth since 2015. The economy was fine in 2015.

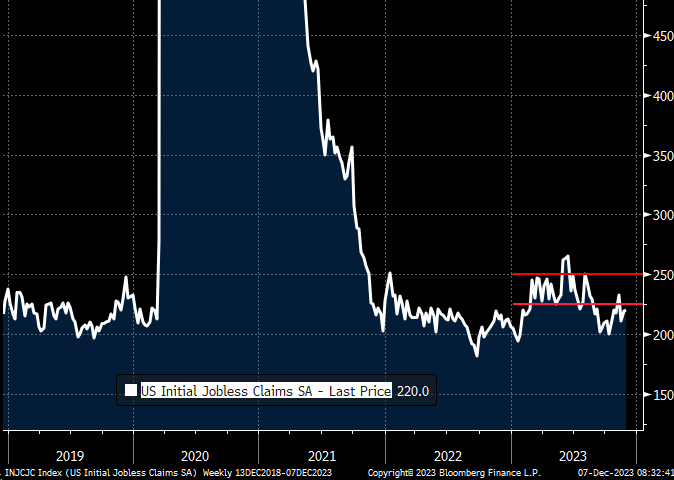

Jobless Claims continue below the 225-250K range reflecting ongoing health in the labor markets.

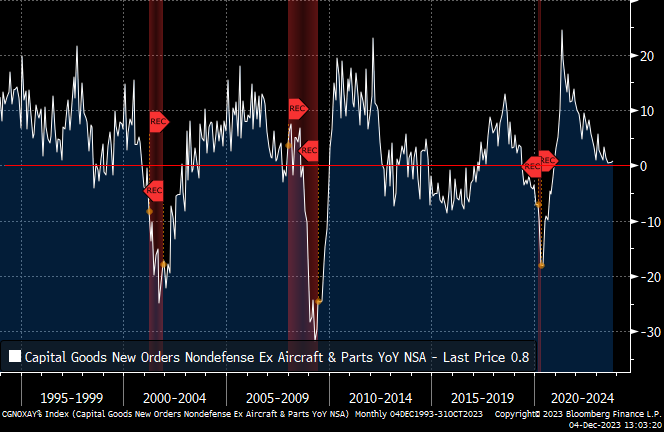

In 2019 consensus was the economy was very strong but Core Capital Goods Orders were negative.

Today, the consensus is recession is imminent… yet orders are stronger than in 2019.

Markets

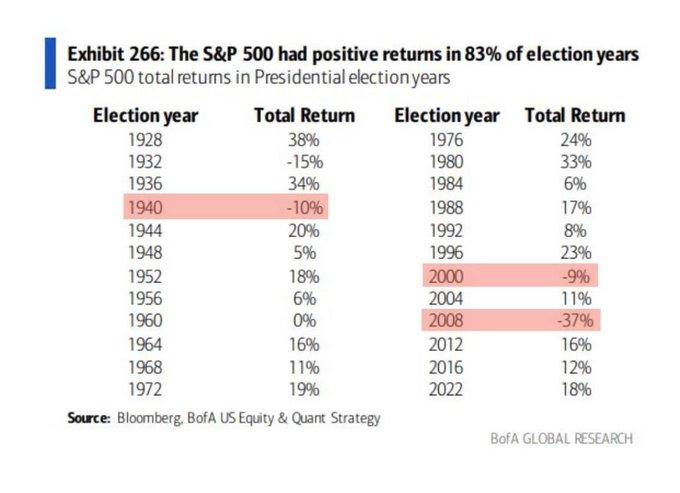

The Presidential Cycle

The stock market has had positive returns in 83% of election years.

1940, 2000, and 2008 were the only three times that the trend was broken.

2024 is an election year.

Will a recession finally hit in the most bullish year of the cycle?

A late-week surge allowed major indexes to close the week with modest gains or flat results. The small-cap Russell 2000 Index outperformed the S&P 500 for the third time in the last four weeks, contributing to a reduction in its substantial year-to-date under-performance.

While growth stocks extended their lead over value shares, energy stocks within the S&P 500 lagged behind due to a drop in domestic oil prices, falling below USD 70 per barrel for the first time since June.

Crude oil is not too far from its recent support levels. Most central banks around the world are cutting rates. We're in a commodity cycle. And energy stocks are now adding the type of diversification (via negative correlation) that bonds once did. Energy firms remain cheap and have clean balance sheets.

As we’ve pointed out before, when tech stocks rally energy declines and vice-versa. But in the long-run both compounds. So it’s good to have energy in the portfolio to complement and diversify technology factor exposure.

Ongoing optimism regarding the potential of generative artificial intelligence (AI) played a role in driving growth indices, particularly boosting the technology-centric Nasdaq Composite.

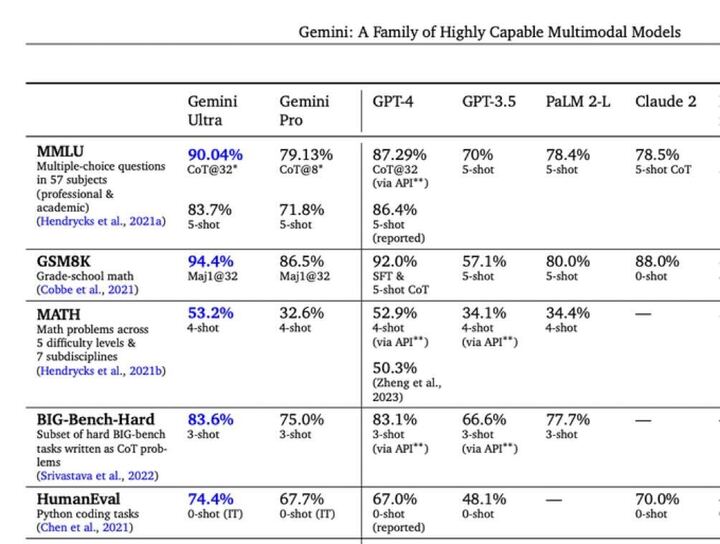

On Thursday, Google parent Alphabet saw a more than 5% increase in its shares following the unveiling of its latest AI model, Gemini.

Gemini demonstrates the capability to process text, code, audio, images, and video, offering integration into mobile applications.

Google’s Gemini Ultra - which rolls out in January - beats OpenAI in a variety of tests.

Gemini Pro, which powers Bard, is still not as strong as OpenAI.

Unlike OpenAI, Google has built multi-modal capabilities at the foundation LLM level.

We believe this drives strategic differentiation.

Google is playing the long-game. We’re all impatient about their results. But between their approach to the AI design and Google accumulating more compute than all its competitors combined - we remain of the view that Google will offer some of the best risk-adjusted returns in 2024.

Simultaneously, Advanced Micro Devices experienced nearly a 10% rise after announcing the launch of a new generation of AI chips.

Earlier in the week, Apple once again surpassed the $3 trillion market capitalization mark, approaching its summer all-time highs.

Recall Apple generated a 0.5% YOY earnings growth this past quarter. With a 29.9 PE ratio we’re no fan… And not surprisingly none of the long/short or fundamental stock picker hedge funds in our 13F analysis own Apple.

If you wanted a moment to sell Apple - or for that matter other highly overvalued names like Palantir, CRM, and Adobe, now is a good time.

Markets Hit all Time Highs

Shorting, while a strategy, comes with its own set of risks. In a trending overbought market, particularly in a bull market, the overbought status can persist, especially considering Q4 seasonality and ongoing inflows.

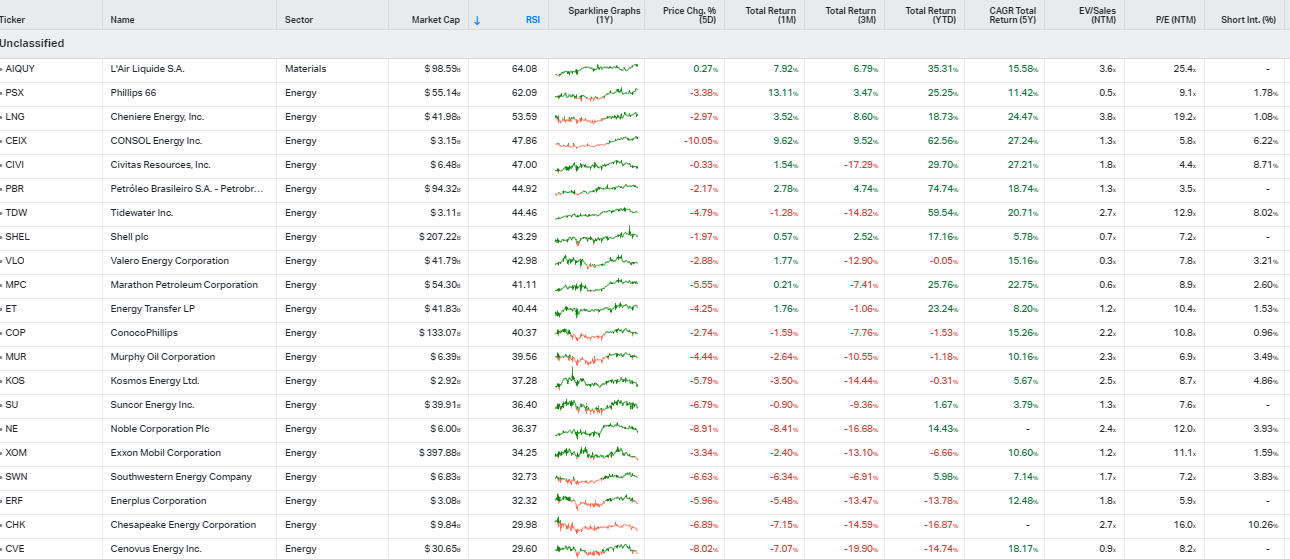

We believe the area to focus on today is Energy.

A noteworthy shift is observed in energy stocks, emerging as the new bonds in terms of correlation and cash flow. Recognizing this trend, the focus shifts towards strategically picking up energy stocks soon.

Here are some energy names we’re following. (This is not a recommendation to buy; you must do your own research.)

Our favorite is Camaco - a uranium miner of which there are only a handful globally. It has yet to pull back.

Names that pop on the list below include Petrobras and Tidewater. We like them both.

Small Caps

November and December are the periods where small caps tend to shine. And that’s happening now as they outperform the S&P.

There are excellent businesses in small caps.

The average P/E ratio for small caps is around ~13 as compared to around ~20 for large caps.

For example, there’s American Public Education (APEI), which provides online post-secondary education. They have a 5 year sales CAGR of 15% and a forward PE of 9.9X. Healthcare training addressing the shortage of nurses in the healthcare system.

There’s another small cap we like which is the leader in hormone replacement therapy.

Biote (BMTE) operates in the medical practice-building business within the hormone optimization space.

The company offers a platform for Biote-certified practitioners to optimize imbalances in their patient’s hormone, vitamin, and mineral levels, as well as prescribe hormone therapies and recommend dietary supplements. The health and wellness trend around hormone therapies and dietary supplements is only increasing.

Also, there are small banks that have ample liquidity and are in a position to grow in the current environment. Small banks are dirt cheap - much cheaper than JP Morgan, which we bought during the March/April ‘banking crisis.

If you filter for the good banks, they should do well.

We have identified a nice list of small caps using our hedge fund 13F tracker.

Over the last 12 months, institutional investors have latched on to the AI theme. They’ve also focused on the ‘Quality’ factor - that means businesses that generate profitable growth.

As recession fears subside, we expect investors will loosen their grip on bidding up the ‘Quality’ factor.

We’re seeing that now with unprofitable tech stocks, cruise lines, and Doge coin (yes, Doge coin) flying off the racks.

Be mindful of valuations. ‘You make your money on the buy.’

A great business with an expensive valuation is not an expensive stock.

There are many great businesses out there with a leadership position, sustainable growth, and attractive valuation. Focus on those names.

Company Earnings

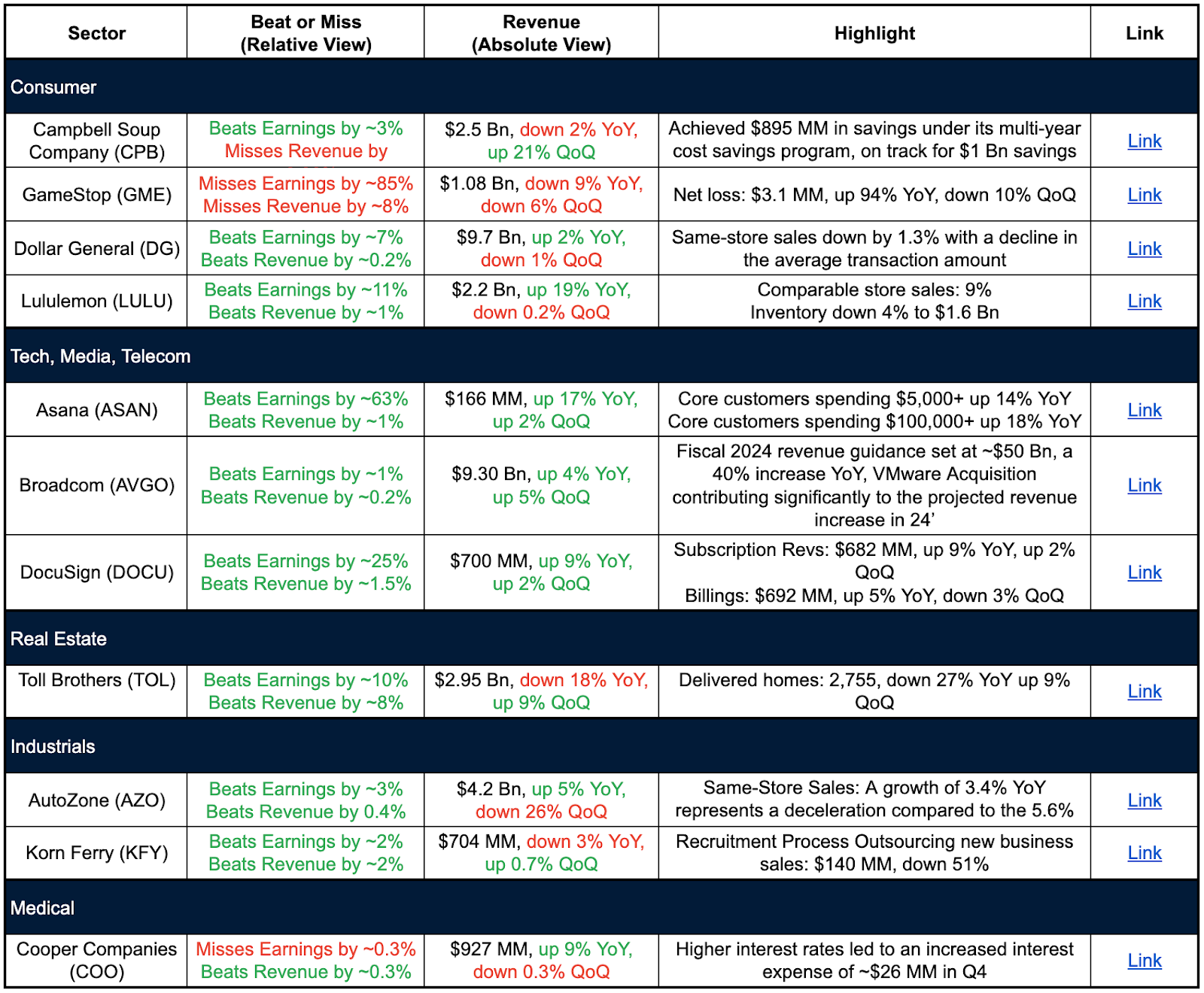

We continue to see this trend of legacy brands in decline, and new brands growing.

Take a look at Lululemon.

Lululemon was trading between $2.50 and $5 in the financial crisis.

Now it's $500. All Time Highs.

That's a 100 to 200x. Beating Amazon, Apple, and Google handily.

Lesson: Don't overlook small cap growth stocks, especially now. Don’t fall in love with Mag 7 names because you’ve owned them forever.

Note: You want to find the next Lululemon. Now it has a $60 Bn+ market cap and a forward PE of 36. Too pricey.

Also - take a look at home builder Toll Brothers. They have a 9% QOQ increase in revenue. That’s a good sign for economic recovery. The comps are improving which means the worst may be behind us.

On Semis - Broadcom did well and is guiding towards a 40% revenue increase YOY. Broadcom is partnering with Google to execute its TPU infra build out.

Asana posted strong numbers. We believe buying Asana is a good idea here.

Amazon vs. Netflix

Take a look at this chart.

The Amazon Prime Membership device is effectively muscling Netflix out of the Top 2 Box. (Hulu is hanging in there.) Netflix has a forward PE of 30. And sales growth of 6%.

I don't see why anyone would want to pay that price to purchase that level of growth (which is also in decline).

Speaking of Amazon, check out 'A Million Miles Away'. It's a great true story film that inspires.

End of the Software Recession? Zoom

The Amazon Membership is a great example of having a “lock” on the customer.

Research from Altimeter’s Jamin Ball suggests the software recession may be over. The chart below shows Net New ARR growth is increasing.

Here’s a stock idea for you along similar lines: Zoom Video.

Yes, the Zoom that many of use for digital meetings.

Zoom achieved a dramatic 50%+ growth during the go-go Covid years.

Then growth slowed to 10% for 2024.

Now, analysts forecast growth of 3 to 5% in the next few years. Analysts have written off Zoom. In our non-consensus lens, that means the worst is priced in.

Meanwhile, Zoom is creating a host of AI tools. They have an ‘AI Companion’ feature. The software captures meeting notes, and also lets latecomers get caught up on the meeting. Zoom has a suite of product features it’s rolling out.

Analysts expect Zoom to grow at nominal GDP.

The bear case is that big enterprises will use Microsoft Teams, and that everyone else will use Google Hangouts. That doesn’t make much sense to us for the same reason no one uses Google Chat.

Zoom is the only specialized player obsessed with getting digital meetings right. There’s room for a third.

The stock is testing its upper resistance now. If it’s rejected, consider accumulating on pullbacks.

The forward PE is 15.8 and marketcap is $22 Bn. The business generates 75% profit margins. Zoom generated about $1.4 Bn in free cashflow.

It’s a profitable tech company.

This is a stock I would consider accumulating on pull backs.

Here’s a longer-term picture of Zoom:

It looks like Zoom is basing. It could take a couple more months for that to complete.

Distressed Investing

Venture Capital & Commercial Real Estate have a lot in common.

Both are seeing markdowns from 2021 peak valuations.

A better way to approach these asset classes is to focus on Secondaries.

Secondaries give you full transparency into the assets, and you’re farther into the J curve.

So you get your money back faster.

And someone else already funded the CapEx too.

You benefit from the mistakes of others

Digital Assets

I suspect we are getting close to a local top in Solana. The enthusiasm is near-peak.

ETH I expect will start to outperform. The drag on our performance is the ETHE discount to NAV. Currently the discount is 13.5% (tightening dramatically from 40 to 50% as recently as June!)

We believe the tighter the discount, then ETH will start to move. The marginal capital is flowing into ETHE and for good reason. After a Bitcoin ETF we should expect to see an Ethereum ETF.

So, you get a nice 13% margin for waiting on that.

Weekly Wisdom

The Paradox of Discipline

People sometimes chafe at the idea of ‘discipline’: commitments, rituals, focus.

It may feel like you are somehow less free.

That’s the wrong frame.

Here's why Discipline matters.

Discipline is the strongest form of self-love.

It means choosing what you want later over what you want now.

Discipline shows how committed you are to your dreams, even on tough days.

Discipline is honoring the covenant you have with yourself. That’s your personal integrity.

Discipline is the path unlocking your best possible future self.

Discipline is honoring & investing in yourself.

Your future self depends on your current self to keep promises made yesterday.

Quote of the Week

“The stock market is a device for transferring money from the impatient to the patient.” – Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/orbe affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.